As ESG reporting accelerates globally, the demand for sustainability assurance is rising sharply. Investors, regulators, and stakeholders are no longer satisfied with disclosures alone; they want verified, credible data.

For African markets, the question is urgent: can sustainability assurance close the trust gap and unlock capital, or will weak systems undermine ESG credibility?

Trust Becomes ESG’s Missing Currency

Sustainability reporting is evolving rapidly across global markets, and Africa is no exception.

From climate disclosures to governance metrics, companies are increasingly publishing ESG data to meet investor expectations and regulatory demands.

However, a deeper challenge is emerging. While reporting volumes are rising, trust in that information remains uneven. Without credible verification, ESG disclosures risk becoming narratives rather than evidence-based accountability tools.

This is where sustainability assurance, independent verification of ESG information, is gaining prominence.

As highlighted in the ACCA report “Sustainability Assurance – Rising to the Challenge”, assurance is becoming essential to enhance credibility, reduce greenwashing risks, and align sustainability reporting with the rigour of financial audits.

For African markets navigating global ESG expectations, sustainability assurance is no longer optional. It is becoming the backbone of credible, investable sustainability performance.

ESG Without Assurance Risks Losing Credibility

“Sustainability reporting is one of the hottest topics globally,” the ACCA report notes, but trust remains the defining issue.

Investors increasingly rely on ESG disclosures to guide capital allocation, yet many remain sceptical about the reliability of reported data. This has triggered a global shift: from disclosure to verification.

Key drivers include:

- Expansion of ISSB standards (IFRS S1 and S2)

- Regulatory mandates such as the EU’s CSRD

- Rising scrutiny of greenwashing

The implication is clear: ESG without assurance is rapidly becoming insufficient.

In African markets, where data systems are still developing, this trust gap is even more pronounced. Without assurance, companies risk exclusion from global capital flows and sustainability-linked financing.

Understanding the Sustainability Assurance Landscape

What is Sustainability Assurance? – Sustainability assurance involves independent verification of ESG disclosures, typically conducted under frameworks such as ISAE 3000 (Revised), used by approximately 94% of assurance providers globally.

It evaluates:

- Accuracy of ESG data

- Reliability of measurement systems

- Completeness of disclosures

- Alignment with reporting standards

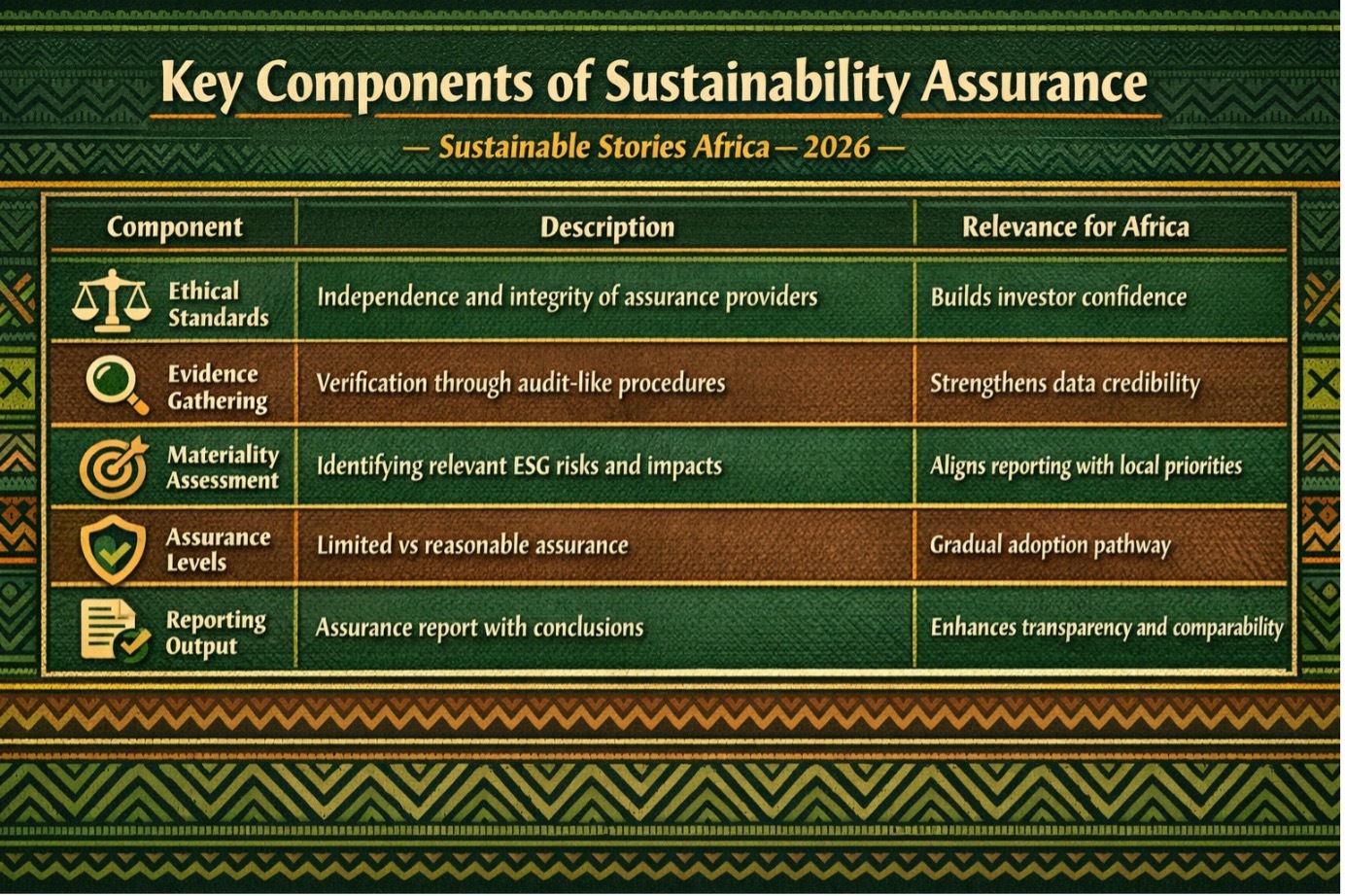

Key Components of Sustainability Assurance

Component | Description | Relevance for Africa |

|---|---|---|

Ethical Standards | Independence and integrity of assurance providers | Builds investor confidence |

Evidence Gathering | Verification through audit-like procedures | Strengthens data credibility |

Materiality Assessment | Identifying relevant ESG risks and impacts | Aligns reporting with local priorities |

Assurance Levels | Limited vs reasonable assurance | Gradual adoption pathway |

Reporting Output | Assurance report with conclusions | Enhances transparency and comparability |

Limited vs Reasonable Assurance — A Critical Distinction

A major insight from the ACCA report is the distinction between:

- Limited assurance: Lower level of confidence, less extensive testing

- Reasonable assurance: Higher confidence, closer to financial audit standards

Misunderstanding this difference can create an “expectation gap” among stakeholders.

Key Challenges in Practice

The ACCA research, informed by global practitioner roundtables, identifies several systemic challenges:

- Data Complexity and Uncertainty – Unlike financial data, ESG metrics often involve forward-looking estimates and scenario modelling.

- Dependence on Experts – Sustainability assurance requires multidisciplinary expertise, including climate scientists, engineers, and social impact specialists.

- Fragmented Reporting Standards – Despite progress, ESG frameworks remain diverse, complicating assurance processes.

- Risk of Greenwashing – Without robust assurance, companies may present misleading sustainability narratives.

The Value Proposition of Sustainability Assurance

If effectively implemented, sustainability assurance can unlock transformative benefits across African markets:

- Investor Confidence and Capital Access – Verified ESG data enhances credibility, enabling access to:

- Green bonds

- Sustainability-linked loans

- Impact investment funds

- Stronger Corporate Governance – Assurance embeds accountability, improving:

- Board oversight

- Risk management systems

- Ethical compliance

- Market Competitiveness – Companies with assured ESG disclosures are better positioned in:

- Export markets

- Global supply chains

- ESG ratings and indices

- Reduced Greenwashing Risk – Independent verification ensures that sustainability claims are evidence-based.

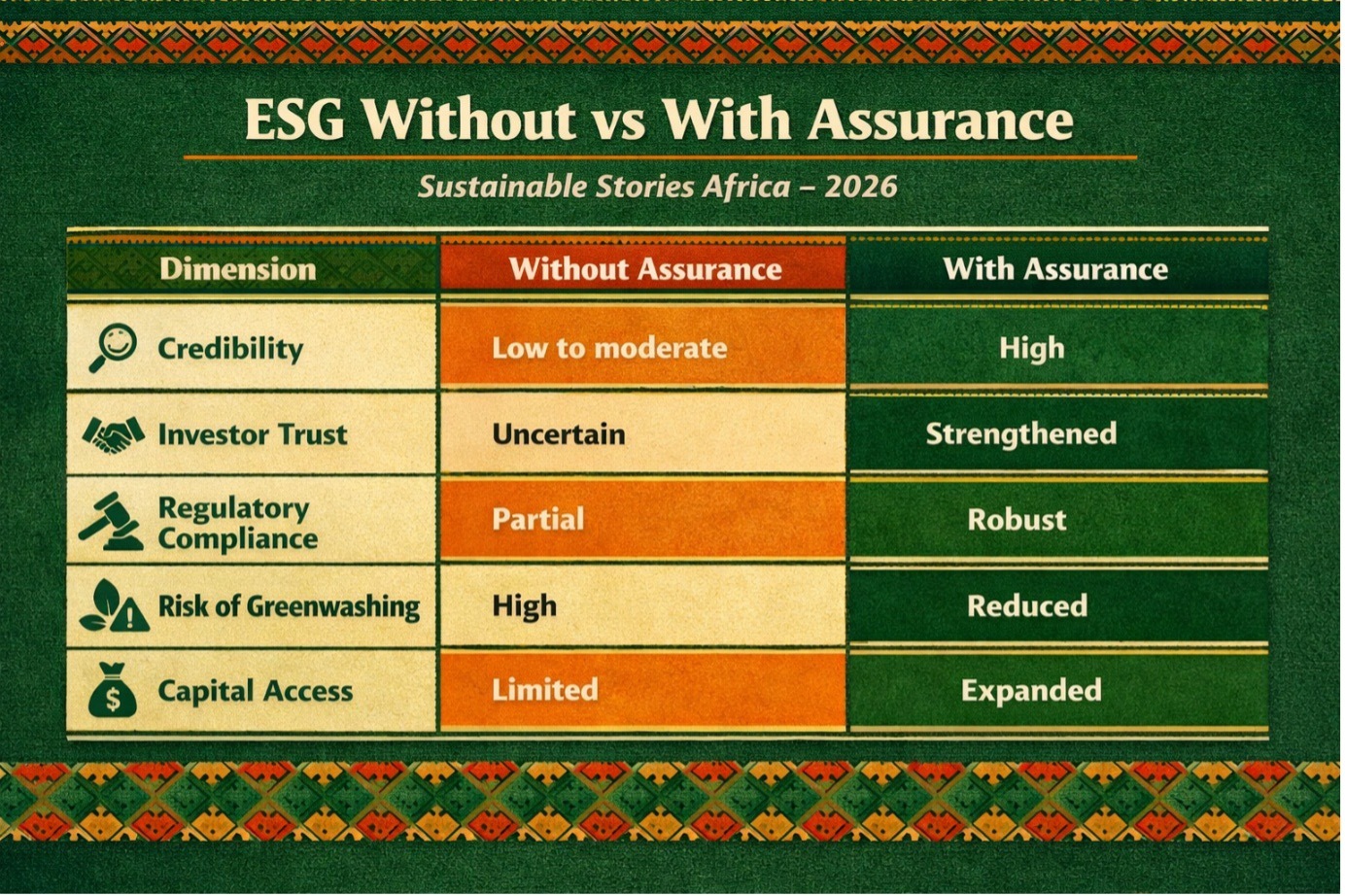

ESG Without vs With Assurance

Dimension | Without Assurance | With Assurance |

|---|---|---|

Credibility | Low to moderate | High |

Investor Trust | Uncertain | Strengthened |

Regulatory Compliance | Partial | Robust |

Risk of Greenwashing | High | Reduced |

Capital Access | Limited | Expanded |

Building Africa’s Sustainability Assurance Ecosystem

To scale sustainability assurance across African markets, coordinated action is required:

- Regulatory Alignment – Governments must integrate assurance requirements into ESG reporting frameworks, aligning with global standards while adapting to local realities.

- Capacity Building – There is an urgent need to develop:

- Skilled assurance professionals

- ESG data systems

- Technical expertise across sectors

- Standard Harmonisation – Reducing fragmentation across ESG frameworks will improve comparability and ease assurance processes.

- Investment in Data Infrastructure – Reliable ESG assurance depends on:

- Digital reporting systems

- Real-time monitoring tools

- Standardised data collection

- Professionalisation of Assurance – The accountancy profession is uniquely positioned to lead, leveraging:

- Audit expertise

- Ethical frameworks

- Established assurance methodologies

As the ACCA report emphasises, audit skills remain fundamental to sustainability assurance engagements.

Path Forward – From Disclosure to Verified Impact

Sustainability assurance is rapidly becoming the bridge between ESG ambition and credibility. For Africa, scaling assurance systems will determine whether ESG reporting translates into real investment, accountability, and impact.

The next phase requires collaboration among regulators, corporations, and assurance professionals to build systems that are credible, scalable, and locally relevant, ensuring that Africa’s sustainability story is not only told but trusted.