Africa’s climate transition is accelerating, but understanding the language of emissions remains a critical gap.

From Scope 1 to carbon footprint, these terms now shape policy, capital flows, and corporate accountability.

As ESG reporting tightens globally, African firms face a simple question: can they compete without fluency in carbon metrics?

The answer increasingly defines access to markets, finance, and long-term resilience.

Carbon Language Now Defines Markets

Across African boardrooms, policy circles, and capital markets, climate language is no longer optional; it is operational.

Terms like “Scope 3 emissions” and “CO₂ equivalent” are shaping investment decisions, regulatory frameworks, and corporate disclosures in real time.

The urgency is driven by tightening global ESG standards, including IFRS sustainability disclosures and value-chain transparency requirements.

For African economies, many of which are both climate-vulnerable and resource-rich, this shift creates a dual reality: risk exposure and opportunity.

At the centre of this transformation lies a foundational issue: understanding the metrics. Without clarity on greenhouse gas (GHG) terminology, businesses risk misreporting emissions, losing investor confidence, and missing out on climate finance.

With clarity, they gain a strategic advantage.

The Language Gap in Africa’s Climate Transition

“More than 60% of emerging market firms struggle with consistent emissions reporting frameworks,”

a senior ESG analyst noted during a recent sustainability roundtable in Lagos.

This gap is not just technical; it is economic. Carbon metrics now influence:

- Access to international capital

- Export competitiveness under carbon border adjustments

- ESG ratings and investor confidence

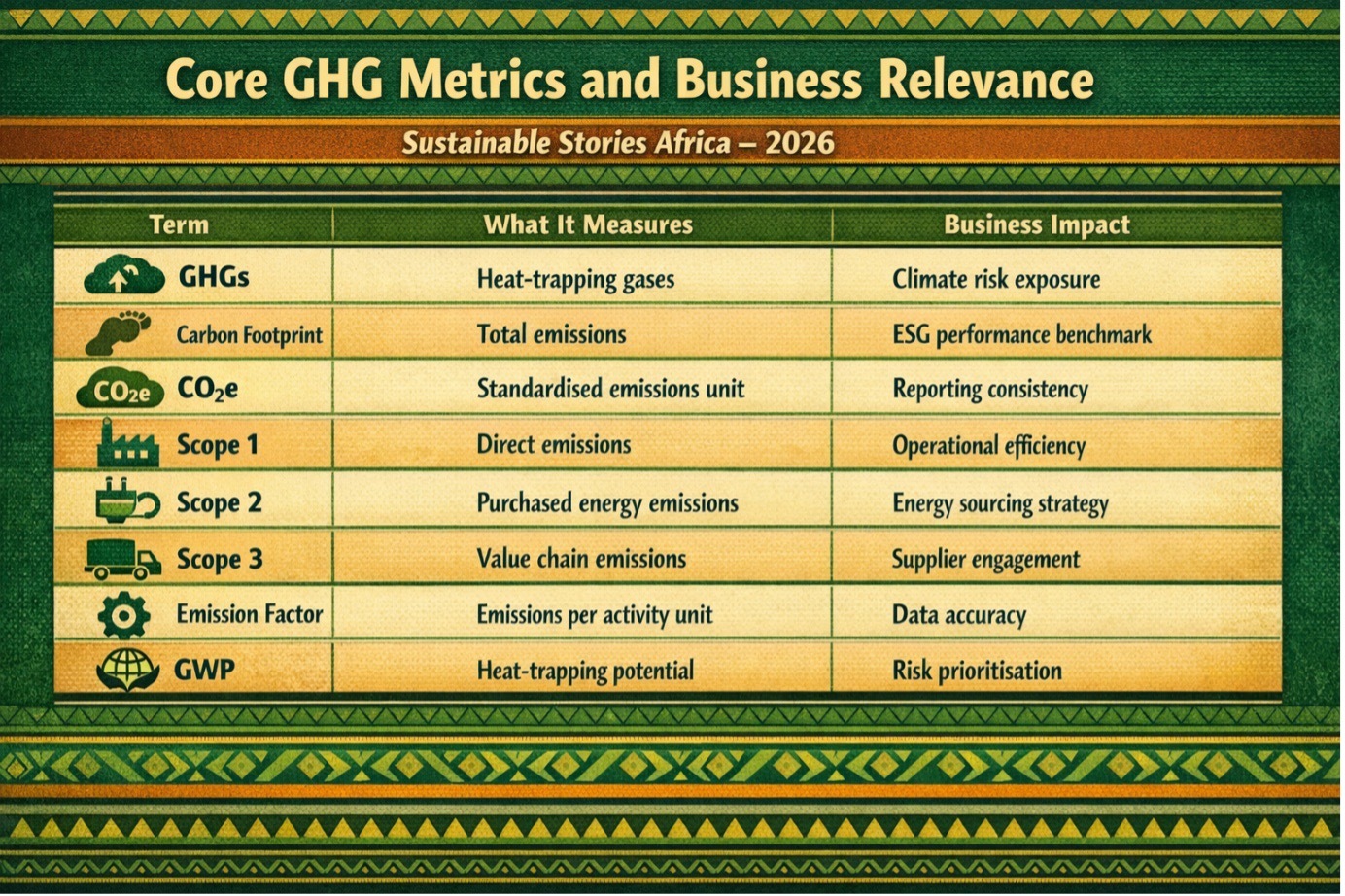

At the heart of this shift are eight core greenhouse gas terms. These are not abstract concepts; they are the building blocks of climate accountability.

Breaking Down the Eight GHG Terms

- Greenhouse Gases (GHGs) – These include carbon dioxide (CO₂), methane (CH₄), and nitrous oxide (N₂O), gases that trap heat in the atmosphere. CO₂ dominates global emissions, but methane is over 25 times more potent over 100 years.

- Carbon Footprint – A measure of total emissions caused directly and indirectly by an entity. For example, a Nigerian manufacturing firm’s footprint includes factory emissions, electricity use, and supply chain logistics.

- CO₂ Equivalent (CO₂e) – A standardised unit converting all greenhouse gases into the equivalent warming impact of CO₂. This allows comparability across sectors and geographies.

- Scope 1 Emissions – Direct emissions from owned or controlled sources—such as fuel combustion in company vehicles or industrial processes.

- Scope 2 Emissions – Indirect emissions from purchased electricity, heating, or cooling. In Africa, where grids are often fossil-fuel-dependent, Scope 2 can be significant.

- Scope 3 Emissions – All other indirect emissions across the value chain—transportation, procurement, waste, and even product use. Often the largest and hardest to measure.

- Emission Factor – A coefficient used to estimate emissions per unit of activity (e.g., kg CO₂ per litre of diesel). These factors are essential for accurate reporting.

- Global Warming Potential (GWP) – A metric comparing how much heat a gas traps relative to CO₂ over time. For instance, methane has a GWP of about 25 over 100 years.

Core GHG Metrics and Business Relevance

Term | What It Measures | Business Impact |

|---|---|---|

GHGs | Heat-trapping gases | Climate risk exposure |

Carbon Footprint | Total emissions | ESG performance benchmark |

CO₂e | Standardised emissions unit | Reporting consistency |

Scope 1 | Direct emissions | Operational efficiency |

Scope 2 | Purchased energy emissions | Energy sourcing strategy |

Scope 3 | Value chain emissions | Supplier engagement |

Emission Factor | Emissions per activity unit | Data accuracy |

GWP | Heat-trapping potential | Risk prioritisation |

Why Mastery of GHG Terms Unlocks Opportunity

Understanding these concepts is not just about compliance—it is about competitiveness.

African companies that accurately measure emissions can:

- Access climate finance – Green bonds and sustainability-linked loans depend on credible data

- Improve operational efficiency – Identifying emission hotspots reduces energy costs

- Strengthen export viability – Particularly under mechanisms like the EU Carbon Border Adjustment Mechanism (CBAM)

- Enhance investor confidence – ESG transparency is increasingly tied to valuation

For governments, standardised emissions data supports:

- Nationally Determined Contributions (NDCs)

- Carbon market development

- Evidence-based policy

The upside is clear: clarity drives capital.

What Needs to Happen Now

To bridge the climate literacy gap, coordinated action is required across stakeholders:

- For Businesses

- Integrate GHG accounting into financial reporting systems

- Invest in data collection and emissions tracking tools

- Engage suppliers to measure Scope 3 emissions

- For Regulators

- Align national frameworks with global standards (IFRS S1/S2, GHG Protocol)

- Mandate phased ESG disclosures for listed companies

- Provide sector-specific emission factors

- For Financial Institutions

- Embed emissions metrics into credit risk assessments

- Support clients with transition financing and advisory

- For Capacity Builders

- Train professionals in carbon accounting and ESG reporting

- Develop Africa-specific data benchmarks and tools

You cannot manage what you cannot measure, and you cannot measure what you do not understand.”

Path Forward – From Metrics to Market Transformation

Africa’s climate future depends on translating complex emissions data into an actionable strategy. Standardising GHG understanding is the first step toward credible ESG reporting and sustainable growth.

The next phase requires alignment between policy, capital, and corporate action to ensure that emissions literacy becomes a competitive advantage, not a constraint.