Ghana has restructured $1.1 billion in IPP debt, renegotiating power contracts and introducing tariff reforms to restore liquidity and stabilise its electricity sector.

However, beneath the headline progress lies a deeper question: can structural inefficiencies, losses, pricing distortions, and governance gaps be resolved fast enough to turn short-term relief into long-term market sustainability?

Debt Reset Meets Structural Energy Reality

In January 2026, Ghana took one of its most decisive steps yet to stabilise its energy sector, renegotiating power purchase agreements (PPAs) with nine independent power producers (IPPs) and restructuring $1.1 billion in legacy debt.

The move, announced by President John Dramani Mahama, is expected to deliver immediate fiscal relief and restore confidence across the sector.

The intervention builds on earlier efforts, including approximately $1.47 billion in payments made in 2025 to clear arrears and restore critical guarantees.

Together, these measures represent a coordinated attempt to halt a decade-long cycle of debt accumulation, tariff distortion, and operational inefficiency.

However, the deeper challenge remains whether Ghana can translate financial restructuring into systemic reform to address the underlying drivers of sector instability while maintaining affordability and investor confidence.

A $1.1 Billion Turning Point

At the centre of Ghana’s energy reset is a stark reality: by early 2025, the country’s power sector debt had reached approximately $3.1 billion, with an additional $1.2 billion required annually for fuel procurement.

The restructuring seeks to address this through:

- Renegotiated PPAs with nine IPPs

- Structured repayment of $1.1 billion between 2026–2028

- Immediate savings of $250 million from reduced capacity charges

But the significance goes beyond numbers.

The crisis itself, outlined in detail on page 3, was driven by “take-or-pay” contracts, tariff under-pricing, and increasing system losses, all compounded by currency depreciation and governance failures.

In simple terms, Ghana was paying for power it did not need, at prices it could not sustain, with revenues it could not fully collect.

How the Crisis Built and What Changed

The roots of the crisis lie in structural mismatches.

Ghana Power Sector Stress Indicators

Indicator | Pre-Reform Reality |

|---|---|

Total Sector Debt (2025) | $3.1 billion |

Annual Fuel Requirement | $1.2 billion |

Transmission & Distribution Losses | 27% |

Capacity Payment Structure | Take-or-pay obligations |

Tariff Levels | Below cost-recovery |

As described on page 4, Ghana’s local power bills denominated in cedis were increasingly unable to meet dollar-indexed IPP obligations, particularly as currency depreciation accelerated. This created a self-reinforcing debt spiral.

- What the Restructuring Changed – The renegotiation process introduced several critical reforms (page 5):

- Revision of capacity charges

- Modification of take-or-pay provisions

- Suspension of new PPAs (since May 2025)

- Termination of 202 dormant contracts worth $227.6 million

- Legislative ratification of revised agreements

This effectively halted the pipeline of new liabilities while restructuring existing ones, a rare dual-track intervention in African power markets.

- Tariff Reform: The MYTO Shift – Crucially, debt restructuring is being reinforced by tariff reform.

The Multi-Year Tariff Order (MYTO) 2025–2030 introduces a five-year pricing framework to replace politically driven quarterly adjustments (page 7).

Key features include:

- Weighted Average Cost of Gas: $7.87/MMBtu

- Exchange rate benchmark: GHS 12.0067/USD

- Inflation benchmark: 8%

- Thermal generation share rising to 78.79% by 2030

This creates predictability but also exposes consumers and the economy to cost pressures.

- Operational Reform: Fixing the Cash Flow System – At the operational level, Ghana has revived the Cash Waterfall Mechanism (CWM), a structured payment system that allocates revenues across the sector (page 9).

Early results are promising:

- ECG disbursed GHC1.07 billion in May 2025

- Monthly collections rose to GHC1.678 billion by June 2025 (up 47.3% year-on-year)

However, persistent inefficiencies remain:

- 27% system losses

- Electricity theft and billing gaps

- Weak metering infrastructure

These represent the “last mile” problem of reform.

A Path to Bankability and Investment

If fully implemented, Ghana’s reforms could reposition its power sector as one of Africa’s most investable energy markets.

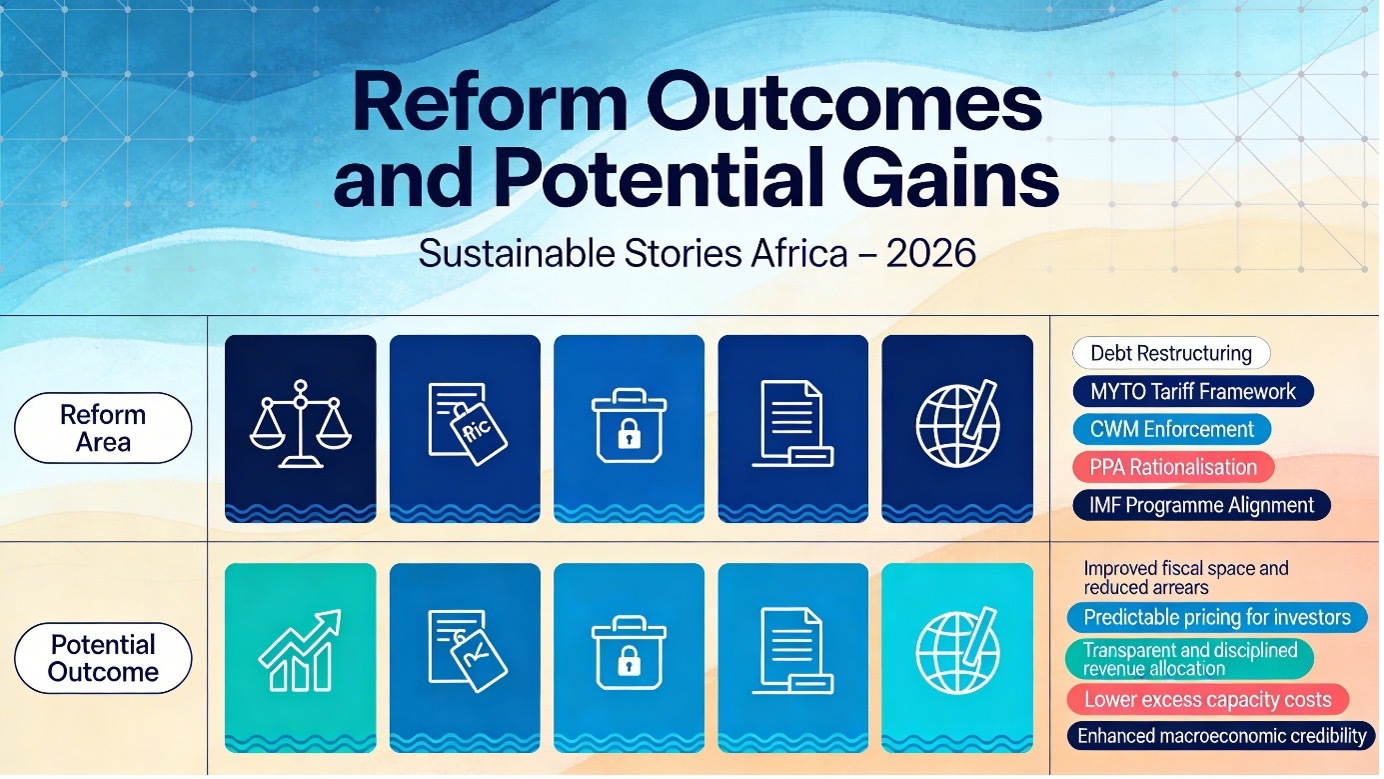

Reform Outcomes and Potential Gains

Reform Area | Potential Outcome |

|---|---|

Debt Restructuring | Improved fiscal space and reduced arrears |

MYTO Tariff Framework | Predictable pricing for investors |

CWM Enforcement | Transparent and disciplined revenue allocation |

PPA Rationalisation | Lower excess capacity costs |

IMF Programme Alignment | Enhanced macroeconomic credibility |

Already, investor sentiment is improving.

Under the IMF programme, Ghana secured approximately $2.8 billion in disbursements and strong signals of support for private-sector participation in the electricity distribution segment (page 11).

The National Energy Compact projects $4.4 billion in required investment by 2030, with $2.6 billion expected from private sources.

For investors, the message is clear: reform is underway, but conditional.

What Must Happen Next

Despite progress, the report is unequivocal: restructuring alone is not sufficient.

Priority Actions

- Reduce System Losses

- Address the 27% distribution loss rate

- Invest in smart metering and grid efficiency

- Enforce Cost-Reflective Tariffs

- Maintain regulatory independence

- Balance affordability with sector viability

- Strengthen Governance Frameworks

- Ensure compliance with the Cash Waterfall Mechanism

- Improve accountability across institutions

- De-risk Private Participation

- Learn from the failed 2019 ECG concession

- Establish clear risk allocation frameworks

- Manage Energy Mix Risk

- Reduce over-reliance on thermal generation

- Mitigate exposure to gas price and FX volatility

As the report warns, Ghana’s challenge is not knowledge or planning; it is the discipline of implementation (page 14).

Path Forward – Reform Must Deliver System Change

Ghana’s IPP restructuring marks a critical inflexion point, shifting the sector from crisis management toward structured reform. But durability will depend on execution: reducing losses, sustaining tariff credibility, and strengthening institutional discipline.

The $1.1 billion reset is not an endpoint. It is a platform. Whether Ghana builds a resilient, investment-ready power sector will determine if this moment becomes a turning point or a reprieve.