Sub-Saharan Africa entered 2026 with its strongest growth in a decade, lower inflation and improving fiscal positions.

However, the IMF warns those gains are now under pressure from war-driven commodity shocks, tighter financing and falling aid.

The region’s next test is whether governments can protect households, preserve debt credibility and accelerate reforms before another external shock becomes a development setback.

Growth Gains Meet Another External Shock

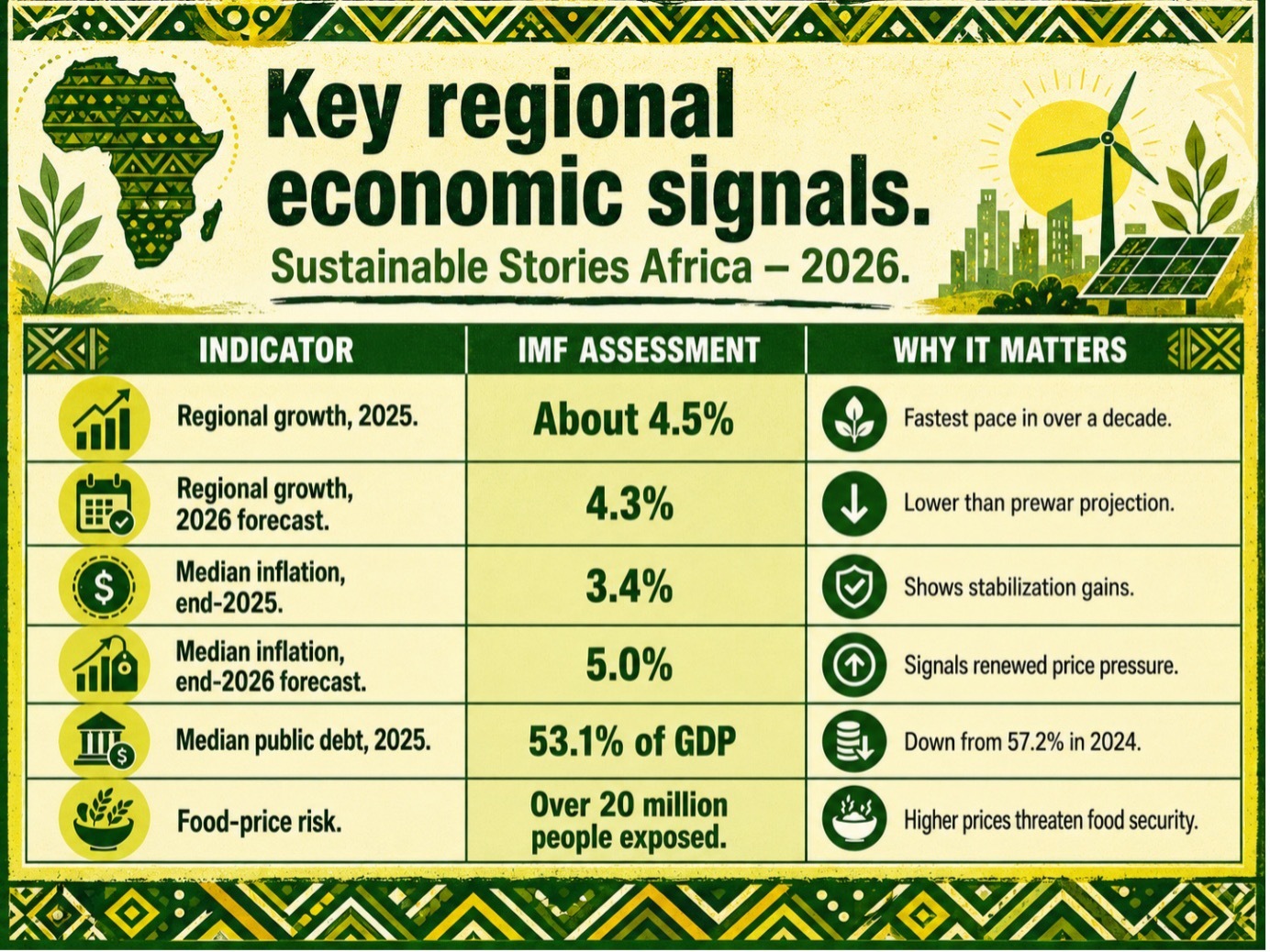

Sub-Saharan Africa’s economic recovery is facing a fresh test after a strong 2025, when regional growth reached about 4.5%, its fastest pace in more than a decade, according to the IMF’s April 2026 Regional Economic Outlook: Sub-Saharan Africa.

The report, titled Hard-Won Gains Under Pressure, says the region entered 2026 with visible stabilisation gains: inflation had moderated, fiscal balances improved, and several countries were beginning to benefit from exchange-rate, fuel-subsidy, fiscal and monetary reforms.

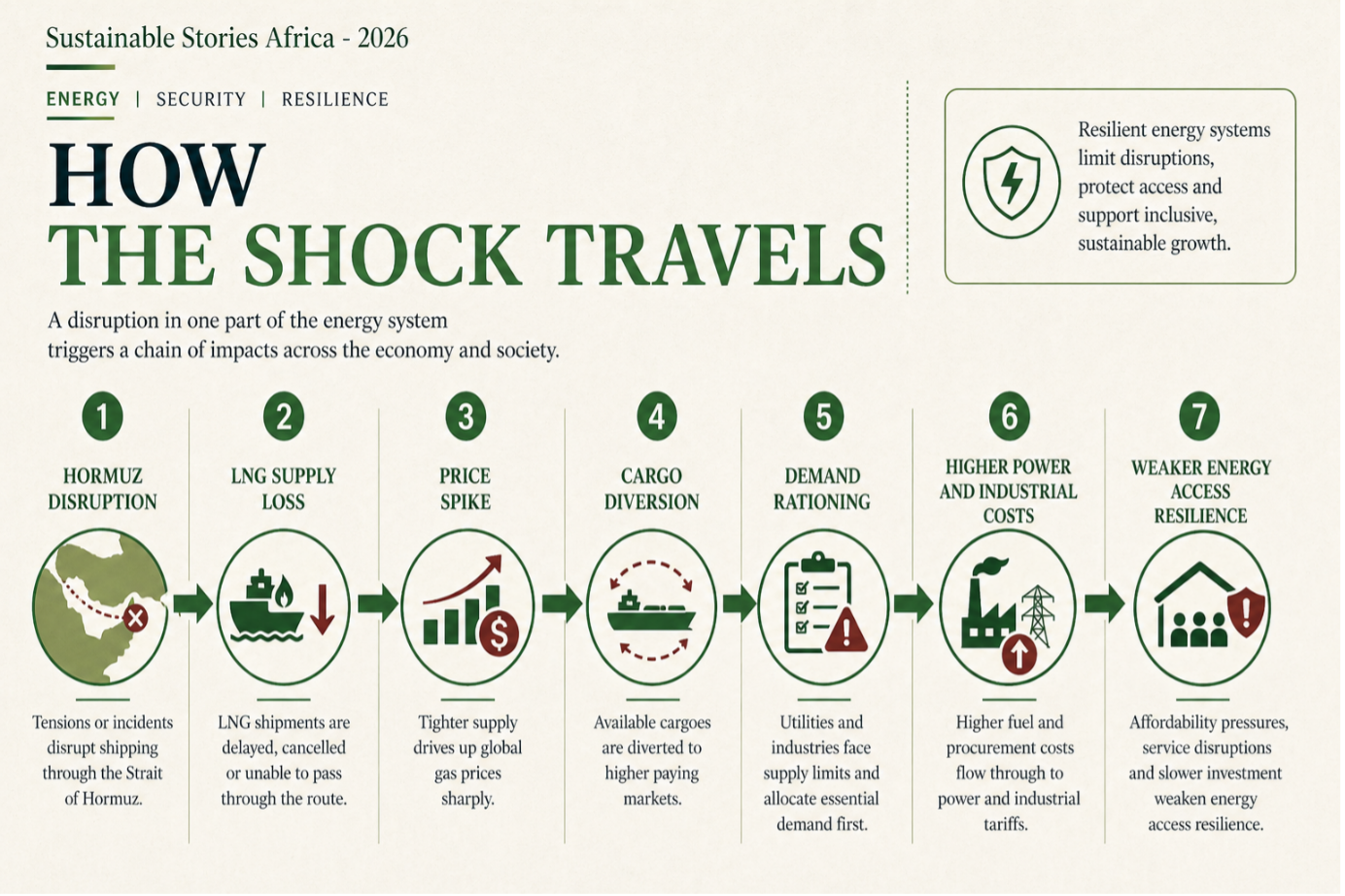

However, the war in the Middle East has changed the outlook.

Oil, gas, fertiliser, and shipping costs have increased, trade with Gulf partners has been disrupted, tourism is weaker in some economies, and remittances may fall.

The IMF now expects regional growth to slow to 4.3% in 2026, while median inflation is projected to rise to 5.0% by year-end from 3.4% at the end of 2025.

Recovery Is Strong But Vulnerable Now

The headline is clear: Sub-Saharan Africa is growing, but its recovery remains exposed.

In 2025, growth accelerated from 4.2% in 2024 to 4.5%. Ten economies grew by more than 6%, with Benin, Côte d’Ivoire, Ethiopia, Rwanda and Uganda among the fastest-growing economies globally. Median inflation fell to 3.4% from 4.8% a year earlier, helped by lower global food and oil prices, easing currency pressures and tight monetary policy in several countries.

The fiscal picture also improved. The median fiscal deficit narrowed to 3.0% of GDP in 2025, 3.4% in 2024, while the median public debt fell to 53.1% of GDP from 57.2%. Ethiopia, Ghana and Zambia also made significant progress on sovereign debt restructuring.

For households, these numbers translate into a familiar story. When fuel prices rise, transport costs rise.

When fertiliser prices rise, food production becomes more expensive. When currencies weaken, imported essentials cost more. And when governments face higher borrowing costs, schools, clinics, roads and social programmes often compete for shrinking fiscal space.

Food Prices Put Social Stability At Risk

The IMF’s warning is not only about GDP. It is about the human consequences of a new inflation shock.

The report estimates that a 20% increase in international food prices could push more than 20 million people in the region into moderate or severe food insecurity.

It also warns that such a price increase could raise child malnutrition prevalence sharply in the most affected countries and leave two million more children under five acutely malnourished.

This is where macroeconomics becomes a lived reality. In an oil-importing African economy, a global conflict can show up as higher bus fares, more expensive cooking fuel, lower household savings, costlier school meals and delayed business expansion.

- For farmers, fertiliser shortages can reduce yields.

- For manufacturers, higher energy costs can cut margins.

- For governments, fuel-price controls may calm consumers today but raise subsidy bills tomorrow.

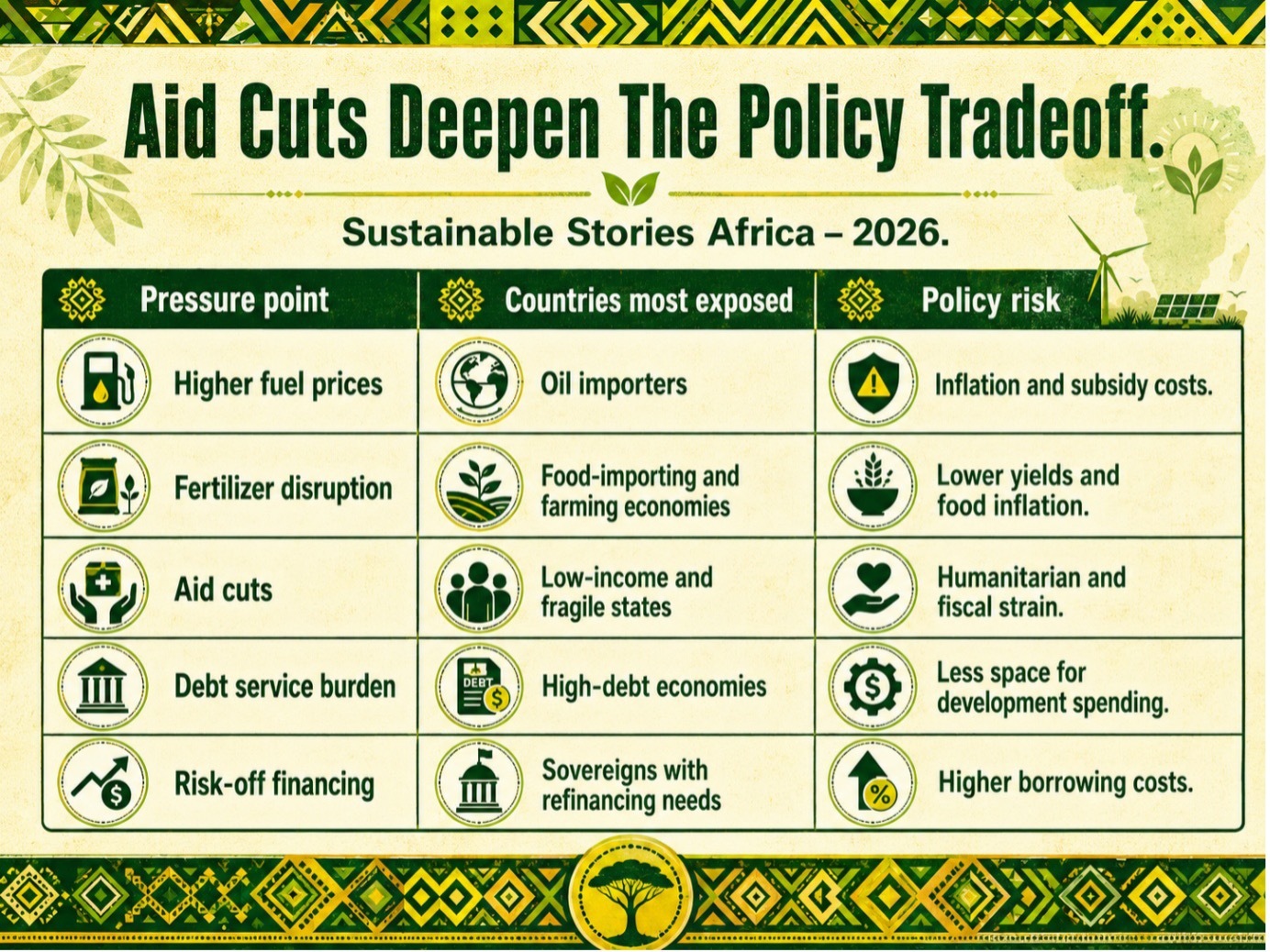

The shock will also hit countries unevenly. Oil exporters may benefit from stronger export revenues, but the IMF warns they remain exposed to volatility and procyclical spending risks.

Oil-importing, non-resource-rich countries face worsening trade balances and higher

Aid Cuts Deepen The Policy Tradeoff

A second pressure point is foreign aid. The IMF says the current aid shock differs in scale, speed, simultaneity and uncertainty.

Many traditional development partners are cutting or reprioritising funding, often with limited warning. Alternative sources, such as UN agencies and NGOs, are not large enough to replace lost bilateral or multilateral budgets.

This matters because aid is not just money. In many low-income and fragile economies, aid also finances delivery systems, capacity and institutional structures for health, education, humanitarian assistance and infrastructure.

More than half of aid to the region goes to health, education and basic humanitarian assistance, while much of the rest supports infrastructure and productive investment.

The IMF says the most vulnerable countries will feel the biggest impact. Among the 15 countries most reliant on official development assistance in the region, 73% are already at high risk of debt distress or in debt distress.

That creates a difficult governance dilemma: if governments replace lost aid, fiscal balances deteriorate; if they do not, essential programmes and services can lapse.

This is why the region’s economic outlook is also an ESG story. Social protection, food security, debt management, public finance transparency and climate resilience are now central to macroeconomic stability.

Reforms Can Turn Pressure Into Resilience

The positive side of the IMF’s message is that policy still matters.

In the near term, central banks need to keep inflation expectations anchored. That may require pausing rate cuts or tightening policy when inflation accelerates, while using clear communication to maintain credibility.

Fiscal authorities need to avoid broad subsidies where possible, protect the most vulnerable with targeted and time-bound support, and preserve priority spending on health, education, water, sanitation and energy access.

Oil exporters are advised to treat any windfall as temporary, rebuild buffers, clear arrears, strengthen safety nets and avoid spending surges that become difficult to reverse.

Oil importers, especially those with limited fiscal space, need to mobilise domestic revenue, reprioritise spending and strengthen public financial management.

Over the medium term, the growth answer is private-sector-led diversification. The IMF highlights reforms that lower the cost of doing business, improve governance in state-owned enterprises, strengthen energy, transport and telecoms networks, deepen local-currency financial markets and advance regional integration through the African Continental Free Trade Area.

Technology also appears in the reform agenda. The IMF says artificial intelligence could improve agriculture, tax administration, healthcare, education and financial inclusion, but only if countries invest in reliable electricity, digital infrastructure, skills, cybersecurity and data governance.

For investors, the signal is mixed but actionable: the region’s growth momentum is real, but resilience will depend on policy credibility, debt discipline, reform sequencing and the ability to convert public spending into measurable outcomes.

Path Forward – Stability Must Protect People First

Sub-Saharan Africa’s task is to defend stabilisation gains without sacrificing citizens. That means credible monetary policy, targeted social support, stronger revenue systems, efficient public spending and faster reforms that unlock private investment.

The priority is resilience. Governments, financiers and development partners must protect food security, preserve essential services, deepen local capital markets and support reforms that make African economies less vulnerable to the next shock.