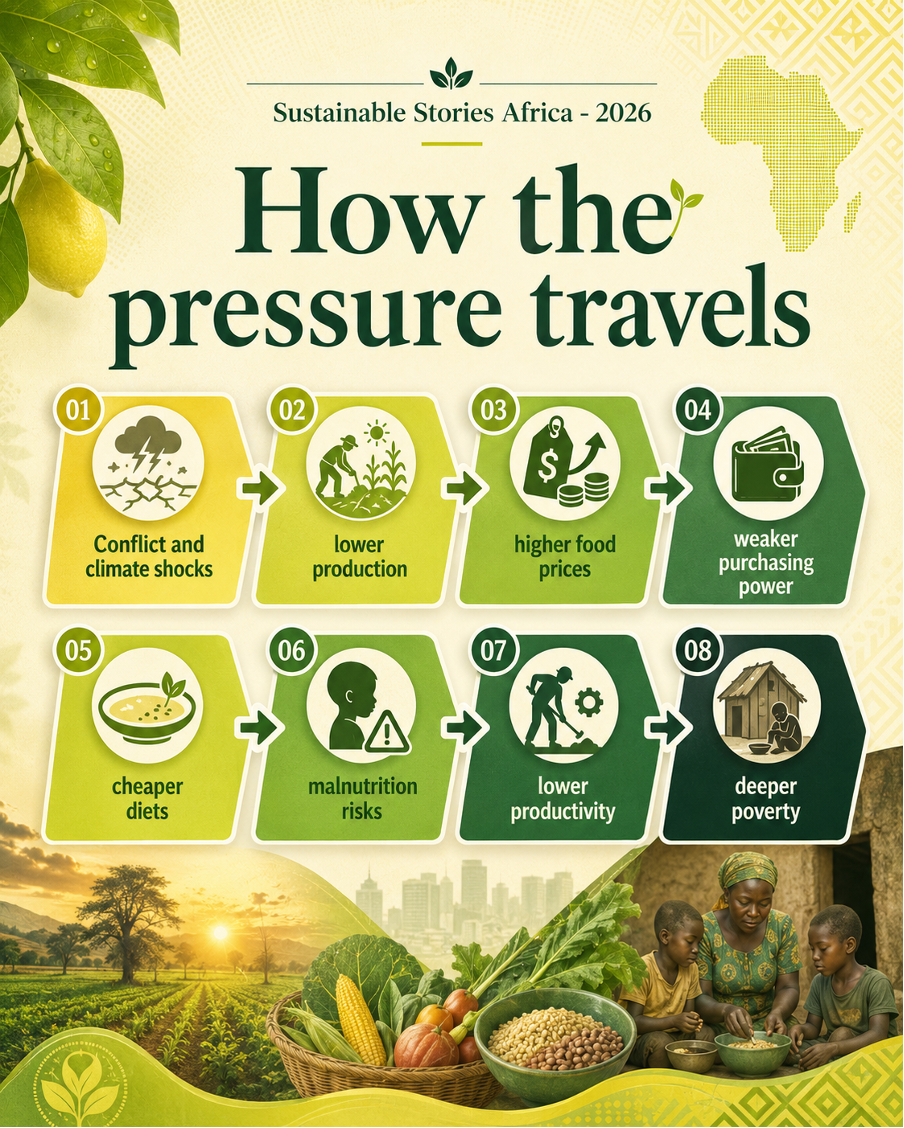

Africa’s food-security crisis is no longer only about harvests, imports or rainfall. It is now a financing story, with hunger rising as public budgets tighten, climate shocks intensify, and food prices outpace household incomes.

The 2025 Africa regional food-security overview warns that without better-targeted finance, the continent risks turning today’s nutrition emergency into a long-term development drag.

Food Finance Now Defines Africa’s Resilience

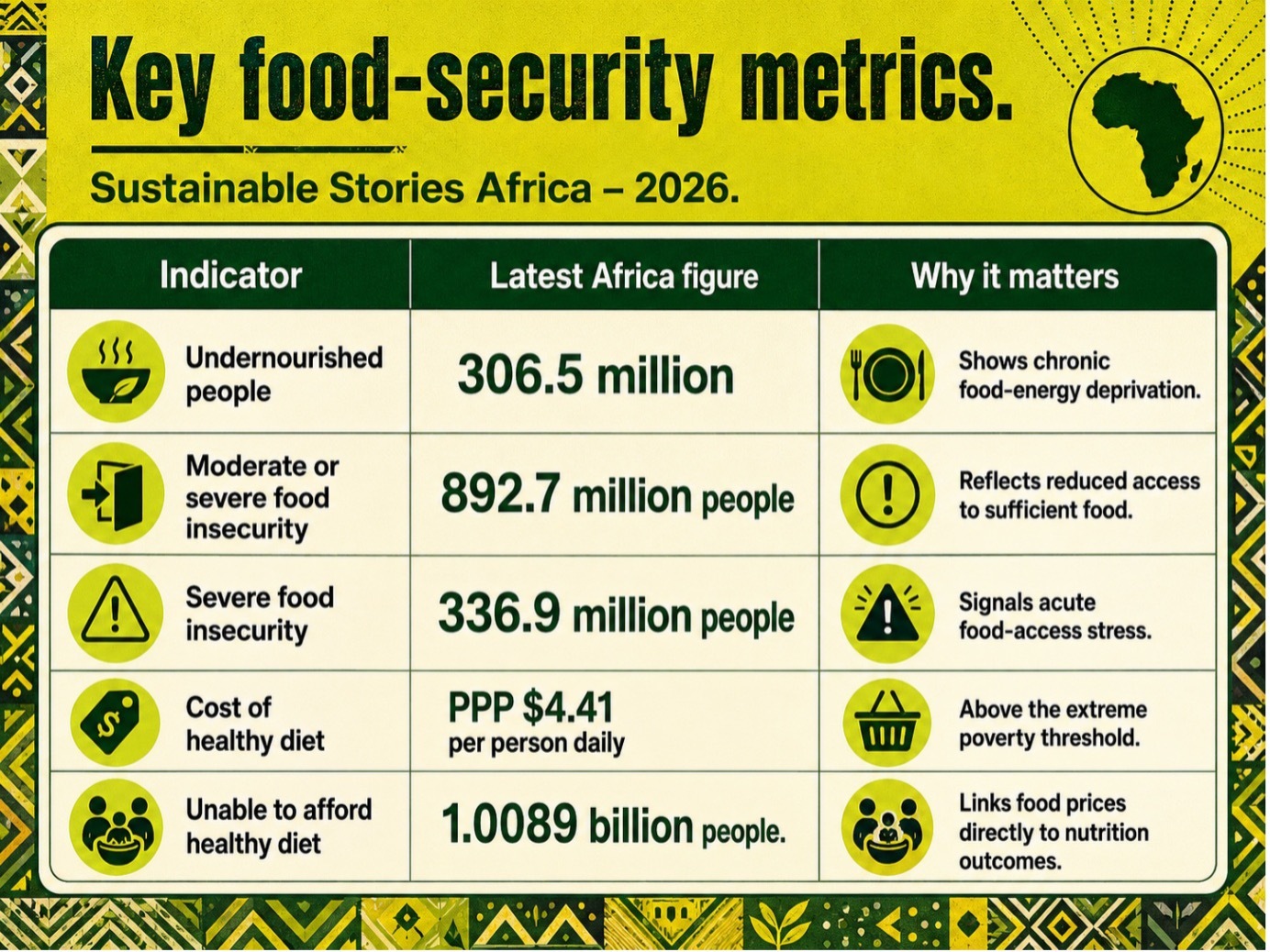

Africa entered 2024 with a sobering food-security balance sheet: 306.5 million people were undernourished, equivalent to 20.2% of the continent’s population, more than twice the global average of 8.2%.

Almost 893 million people faced moderate or severe food insecurity, while nearly 337 million experienced severe food insecurity.

The figures, contained in the Africa Regional Overview of Food Security and Nutrition 2025, jointly prepared by FAO, ECA, WFP and the African Union Commission, show a continent where food systems are being squeezed from several directions: conflict, climate variability, economic downturns, high borrowing costs and persistent inequality.

The report’s central message is direct: Africa cannot eat its way out of hunger without financing its way into more resilient agrifood systems.

Hunger Is Rising Faster Than Budgets

The most urgent finding is that Africa’s hunger crisis has widened since the COVID-19 pandemic.

The report says 73 million more people in Africa have faced hunger since the pandemic, while the continent now accounts for more than 45% of the world’s hungry people.

This is not only a humanitarian warning. It is an ESG, governance and investment signal.

Food insecurity weakens labour productivity, increases social pressure, raises public health risks and exposes gaps in climate adaptation, agricultural policy and fiscal planning.

The data also show that the crisis is uneven. Central Africa recorded the highest prevalence of moderate or severe food insecurity at 77.3% in 2024, followed by Eastern Africa at 64.9% and Western Africa at 63.2%.

Women were slightly more affected than men, with 58.2% of women facing moderate or severe food insecurity compared with 57.1% of men.

Food Prices Reveal The Nutrition Gap

For households, the crisis often begins at the market stall. The average cost of a healthy diet in Africa rose to PPP $4.41 per person per day in 2024, up 5.5% from 2023.

That figure is more than double the extreme poverty threshold of PPP $2.15, meaning that even some people not classified as extremely poor may still be priced out of nutritious diets.

By 2024, more than one billion Africans could not afford a healthy diet, an increase of more than 29 million from 2023 and about 145 million more than before the pandemic. Eastern Africa alone accounted for 365.5 million people unable to afford healthy food, while Western Africa accounted for 319.6 million.

The nutrition indicators underline the human cost. Stunting among children under five remained above 30% in 2024, anaemia among women aged 15 to 49 reached 35.9% in 2023, and adult obesity rose to 16.2% in 2022, showing that Africa faces the double burden of hunger and poor-quality diets.

Better Finance Can Rebuild Food Systems

The opportunity is that Africa’s food-security crisis has identifiable financing levers. The report frames agrifood finance around public spending, international development funding, domestic bank credit, foreign direct investment and remittances.

Public spending is rising in some areas, but not fast enough. Domestic public expenditure in agriculture, forestry and fishing reached about $16 billion in 2022, up from $12.6 billion in 2020 and $14.6 billion in 2021.

However, fiscal pressure, debt stress and reduced donor space are limiting how much governments can invest in SDG 2 priorities.

Private finance remains a weak link. Credit to agriculture, forestry and fishing averaged less than 4% of total credit between 2001 and 2022, while foreign direct investment into Africa has historically accounted for approximately 3% of global FDI.

Food and beverage investment flows have also remained low and uneven.

Still, the report points to underused channels. Remittances reached an estimated $100.1 billion in 2022 and benefited at least 200 million people.

Blended finance for African agrifood systems reached $3 billion across 99 deals between 2020 and 2023, although many transactions remain too large and downstream to support smallholders.

Governments And Markets Need Coordinated Delivery

The action agenda is clear. Governments need to treat food security as infrastructure, not relief.

That means stronger national agricultural investment plans, predictable public spending, better food data systems, climate-smart agriculture, rural roads, irrigation, storage, extension services and social protection.

Regulators and financial institutions must reduce the perceived risk of lending to agriculture. That requires credit guarantees, crop insurance, warehouse receipt systems, concessional capital, advisory support for agri-SMEs and blended-finance structures that lower ticket sizes to reach cooperatives, processors and farmer groups.

Climate finance also needs to move closer to food systems. Africa’s climate finance flows rose 48% to $44 billion in 2021/2022, but that was still only 18% of the estimated $250 billion required annually to meet the continent’s 2030 climate goals.

The report argues that climate capital must be designed around farmers, agribusinesses and value-chain actors, not only large mitigation projects.

For investors, the message is equally practical: food security is no longer a soft-development category.

It is a market-stability issue, a climate-resilience issue and a governance test for African economies.

Path Forward – Financing Must Reach Farms First Now

Africa’s food-security response must shift from emergency spending to transformation finance: targeted public investment, lower-risk private credit, climate-smart capital and support for agri-SMEs that connect farmers to markets.

The priority is delivery. Finance must reach farms, women, processors, traders and households before the next shock.

That is how food security becomes resilience, and resilience becomes sustainable development.