Libya’s private sector is carrying more than commerce. In an economy fractured by conflict, weak institutions and uneven development, informal traders and MSMEs have kept livelihoods, supply chains and regional exchange alive.

A new AfDB policy note argues that peace-positive investment in agribusiness, fisheries, renewable energy, finance and infrastructure could help turn private enterprise into a stabilising force.

Libya’s Private Sector Becomes Peace Test

Libya’s next phase of recovery may depend less on oil wealth alone and more on small firms, informal traders, municipal actors, and entrepreneurs still moving goods across divided regions after more than a decade of conflict.

That is the core message of the African Development Bank’s April 2026 policy note, Investment for Peace and Prosperity: Leveraging Libya’s Private Sector for Resilience and Inclusive Growth, which frames private-sector development as a pathway to jobs, social cohesion and institutional recovery.

The report comes as Libya faces a familiar paradox: a resource-rich economy with fragile public systems, limited private credit, uneven regional development and high youth exclusion. Yet beneath that instability, the AfDB sees a practical opening — invest in markets that already connect communities, then use them to support peace.

Conflict’s Hidden Cost Meets Enterprise Resilience

The African Development Bank notes that despite currency volatility, restricted financing, and weak financial integrity systems, the private sector, particularly informal actors and MSMEs, has continued to sustain supply chains and livelihoods across Libya.

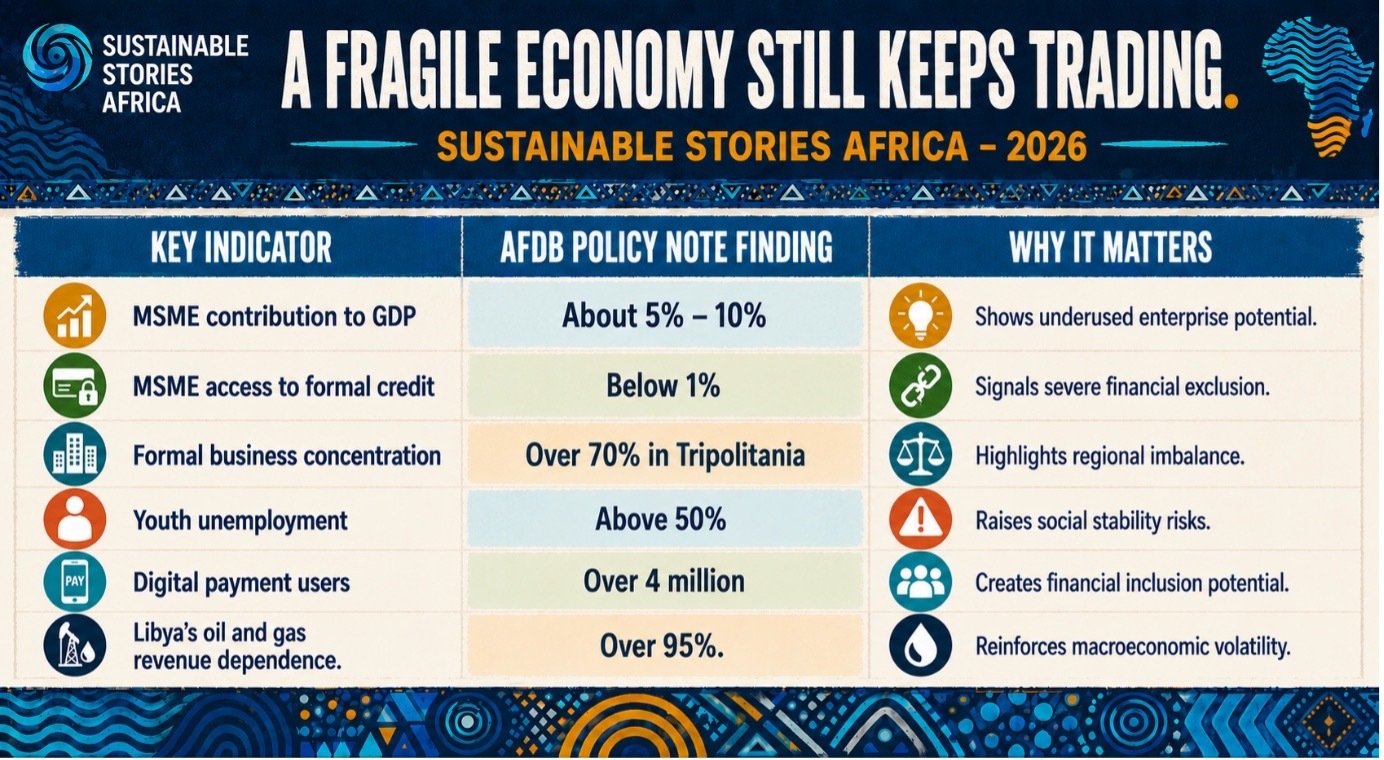

The data reveals both the scale of vulnerability and the breadth of opportunity. Libya's informal sector employs more people than the public sector; however, MSMEs contribute only 5% – 10% of national output.

Access to formal credit remains below 1%. Over 70% of formal business activity is concentrated in Tripolitania, leaving Fezzan chronically underinvested.

Youth unemployment exceeds 50%, and women's labour-market participation remains below 25%.

For the AfDB, these are not merely economic indicators; they are peacebuilding imperatives. Where young people cannot work, and firms cannot access credit, fragility deepens.

Conversely, functional trade corridors, thriving local enterprises, and clean-energy systems can generate shared economic interest, ultimately reducing the structural incentives for conflict.

A Fragile Economy Still Keeps Trading

Libya's formal economy remains state-dominated, with only 11% of formal jobs in the private sector.

The informal economy represented approximately 36.2% of GDP in 2020, while wholesale and retail trade accounted for nearly 90% of private-sector value.

Agriculture employs roughly 9% of the labour force yet contributes marginally to GDP, exposing a persistent gap between livelihoods and productivity.

Institutional weaknesses compound financial constraints. More than 85% of financial assets are held by state-owned banks, with the Central Bank of Libya controlling around 70% of banking assets, leaving private enterprises without adequate financing mechanisms or guarantees to expand despite existing capacity.

Stakeholders have called for clearer institutional frameworks and an accelerated public-private partnership law.

The economic cost of conflict is staggering, estimated at 783.4 billion Libyan dinars (approximately $580 billion).

Between 2016 and 2025, private consumption fell by 37.76%, total investment declined by 68.15%, and private investment dropped by 45.84%. In 2018, 97% of firms reported conflict-related impacts.

Nevertheless, digital adaptation is gaining ground. With 88.4% internet penetration and 80.7% smartphone usage, instant-payment platforms including LY Pay and One Pay now serve 4 million users and 47,000 merchants, while digital transactions exceeded 20 billion dinars in early 2025.

Where Investment Could Turn Into Stability

The AfDB's central argument is that Libya's private sector is already functioning as a social connector, not merely a growth engine awaiting activation. Traders, MSMEs, tribal networks, and municipal actors sustain supply chains where national institutions often fall short.

The policy note consequently prioritises three peace-positive sectors: agribusiness, fisheries, and renewable energy.

- Agribusiness can link southern Fezzan producers with northern urban markets through dates, tomatoes, cold chains, and rural logistics.

- Fisheries can connect coastal communities from Zuwara to Tobruk.

- Renewable energy can address grievances rooted in unequal service delivery and chronic power shortages.

Infrastructure investment is equally central. Libya's planned 1,750-kilometre Highway of Peace, stretching from Emsaad on the Egyptian border to Ras Jedir near Tunisia, is framed as a national reconstruction corridor.

In November 2025, Italy awarded a €700 million contract for the western segment, with remaining negotiations expected in 2026.

Renewable energy holds the greatest transformative potential. Libya depends on oil and gas for over 95% of national revenues; however, it faces a 25% gap in power supply due to maintenance backlogs and damage resulting from conflict.

With more than 3,500 annual sunshine hours, decentralised solar systems could reduce outages by up to 70%, while a single 10 MW solar plant can generate approximately 100 construction jobs and 10 – 20 permanent positions.

The Reforms Needed To Unlock Growth

The AfDB's recommendations follow a deliberate sequence: establish readiness, build trust, then scale.

- First priority is a phased engagement model, moving from analytical groundwork to pilots and then broader operations, supported by a proposed Technical Support Unit to help Libyan firms develop concept notes, business plans, and transaction documents that meet development finance standards.

- Second, stronger institutional and data systems are essential. This includes mapping MSMEs, incubators, and enterprise support centres; establishing a National MSME and Innovation Network; and streamlining business licensing and commercial dispute resolution at the municipal level, reforms that directly determine whether small firms can register, borrow, hire, or join a value chain.

- Third, a credible PPP framework is needed for peace-positive infrastructure, with conflict-sensitive models, legal advisory support, and transparent procedures across solar energy, logistics, agribusiness, and municipal services. Without clear contract structures and defined risk allocation, private capital will not mobilise at scale.

- Fourth, expanding MSME finance and digital inclusion, through credit guarantees, interoperable payment systems, alternative credit scoring, and Sharia-compliant financing, could move thousands of enterprises from survival into formal growth.

- Finally, Libya's diaspora, estimated at around 3% of the population residing largely in high-income countries, represents an underutilised investment bridge.

Transparent diaspora bonds, co-investment windows, and SME financing platforms could convert external skills and capital into peace-positive economic activity.

Path Forward – Build Markets That Hold

Libya’s recovery agenda should prioritise practical reforms that turn enterprise into stability: MSME finance, municipal capacity, PPP laws, diaspora investment and clean-energy deployment.

The AfDB’s message is clear: peace-positive investment must be sequenced, local and measurable. For Libya, the next test is whether institutions can back the traders, entrepreneurs and communities already keeping the economy connected.