Nigeria’s fiscal story has taken a sharp turn: subsidy cuts, tax reforms and higher revenues are now colliding with rising debt service, expensive borrowing and household pressure.

The central question is whether fiscal reform can move beyond accounting gains to visible development, better power, jobs, infrastructure, social protection and climate resilience.

Nigeria Faces A Fiscal Credibility Test

Nigeria is entering a harder phase of reform. The country has removed fuel subsidies, adjusted the exchange-rate system, pursued tax reforms and tried to rebuild investor confidence; however, the fiscal space created by those reforms is being squeezed by a larger debt stock and heavy debt-service obligations.

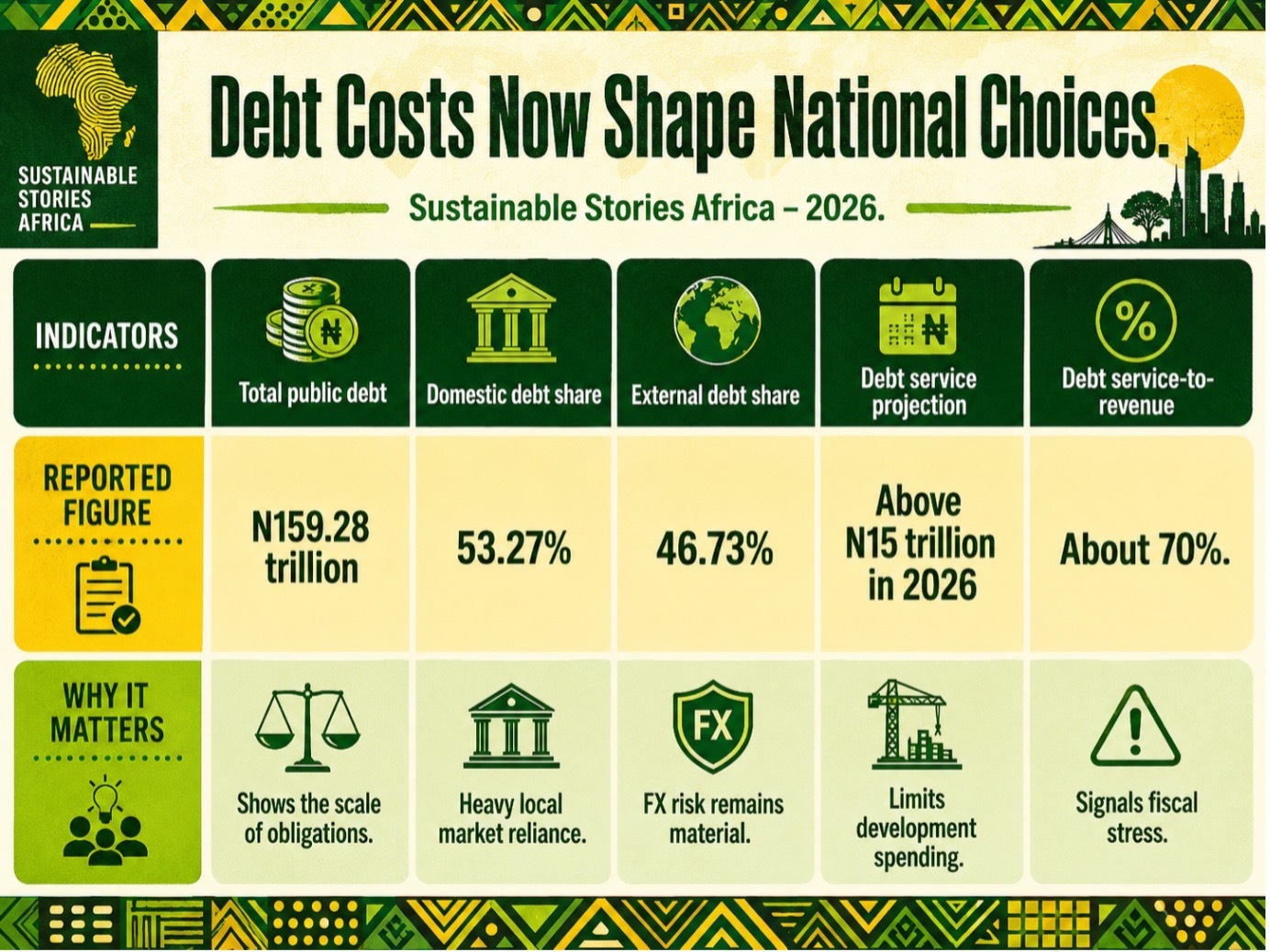

The Debt Management Office’s latest figures put Nigeria’s total public debt at N159.28 trillion as of December 2025, up from N153.29 trillion in September 2025 and N144.67 trillion in December 2024. Domestic debt accounted for 53.27% of the total, while external debt made up 46.73%.

This is the great fiscal reversal: Nigeria is moving from a period of delaying political costs to one in which old fiscal choices now compete with urgent development needs. For citizens, the reversal shows up in food prices, transport costs, electricity bills, school fees, health spending and the uncertain promise of growth.

Debt Costs Now Shape National Choices

The pressure is no longer abstract. Financial Nigeria’s article, “The great fiscal reversal,” argues that the Tinubu administration has added N87.38 trillion to total public debt in less than three years, with debt service costs now taking about 70% of government revenue.

That figure matters because debt service is money that cannot easily support hospitals, schools, roads, clean energy, flood control or small-business support.

It also narrows the government’s ability to respond when inflation rises, oil prices shift, insecurity disrupts farming, or climate shocks damage communities.

BudgIT has also warned that debt servicing rose from N942 billion in 2014 to N12.6 trillion in 2024 and is projected to exceed N15 trillion in 2026, keeping Nigeria in a high debt-service-to-revenue band.

Reform Gains Meet Household Pain

Nigeria’s reforms have improved parts of the macroeconomic story. The IMF said recent policy changes, including the removal of subsidies, the ending of monetary financing of the deficit and reforms to the foreign-exchange market, helped strengthen investor confidence and reopen access to Eurobond markets.

However, reform credibility is not measured only by bond-market access.

It is measured by whether households feel less exposed, whether companies can plan, whether states deliver services, and whether public spending becomes more transparent.

The World Bank expects Nigeria’s economy to grow in 2026. However, it has warned that conflict-driven energy shocks could lift inflation, even after inflation eased from late-2024 highs.

Nigeria’s reforms helped improve reserves, reduce the fiscal deficit to 3.1% of GDP in 2025 and reduce debt-to-GDP for the first time in a decade.

For a market trader in Lagos, a farmer in Benue or a manufacturer in Aba, the fiscal reversal is practical.

- Higher fuel costs affect transport.

- Exchange-rate adjustment affects imported inputs.

- Interest rates affect credit.

- Weak public investment affects roads, power and logistics

The promise of reform must therefore become visible in daily economic life.

Fiscal Repair Can Unlock Development Value

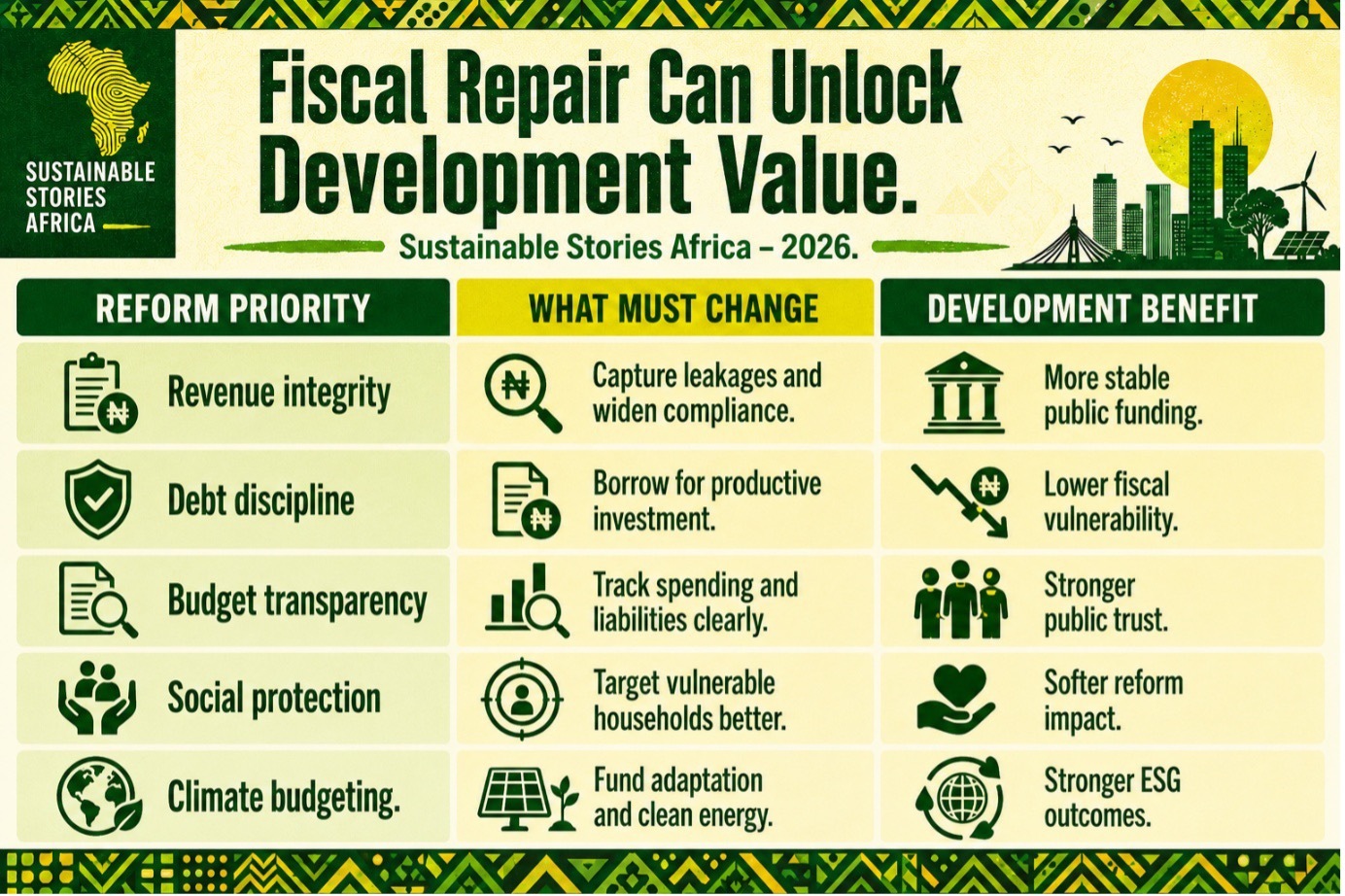

The upside is that Nigeria still has a route out of the squeeze. A stronger revenue base, better tax administration, disciplined borrowing and transparent spending can create a fiscal system that supports development rather than merely servicing liabilities.

Government’s own fiscal-positioning argument is that Nigeria’s structural constraint is not simply the absence of revenue, but weak revenue capture, recognition and routing within a coherent fiscal system.

That is why tax reform is central. If revenues rise through better compliance, digital systems and fairer collection — rather than arbitrary pressure on already-strained households — Nigeria can finance infrastructure, social protection and climate resilience more credibly.

Nigeria Must Convert Reform Into Delivery

The next phase should focus on execution. Nigeria needs to show that fiscal consolidation is not only about reducing deficits, but also about improving the quality of public spending.

Government should prioritise projects with clear economic and social returns: power-sector reliability, transport corridors, primary healthcare, basic education, food-system resilience and flood-control infrastructure.

These are not soft priorities. They are productivity investments.

- Regulators and lawmakers must strengthen oversight of debt, contingent liabilities, public-private partnerships and state-owned enterprises

- Investors need clearer fiscal rules.

- Citizens need open contracting, credible budget dashboards and stronger accountability for capital projects.

Businesses also have a role.

- In a tighter fiscal environment, companies need stronger governance, energy efficiency, local sourcing, ESG disclosure and risk planning.

Fiscal credibility and corporate integrity now reinforce each other.

Path Forward – Make Fiscal Reform Count

Nigeria’s great fiscal reversal should become a development reset, not only a debt-management exercise.

The priority is to turn higher revenue, tax reform and investor confidence into visible public value.

That means disciplined borrowing, transparent budgets, stronger social protection and climate-smart investment.

If reform is matched with delivery, Nigeria can convert fiscal pain into a more credible, inclusive and sustainable growth path.

Culled From: The great fiscal reversal