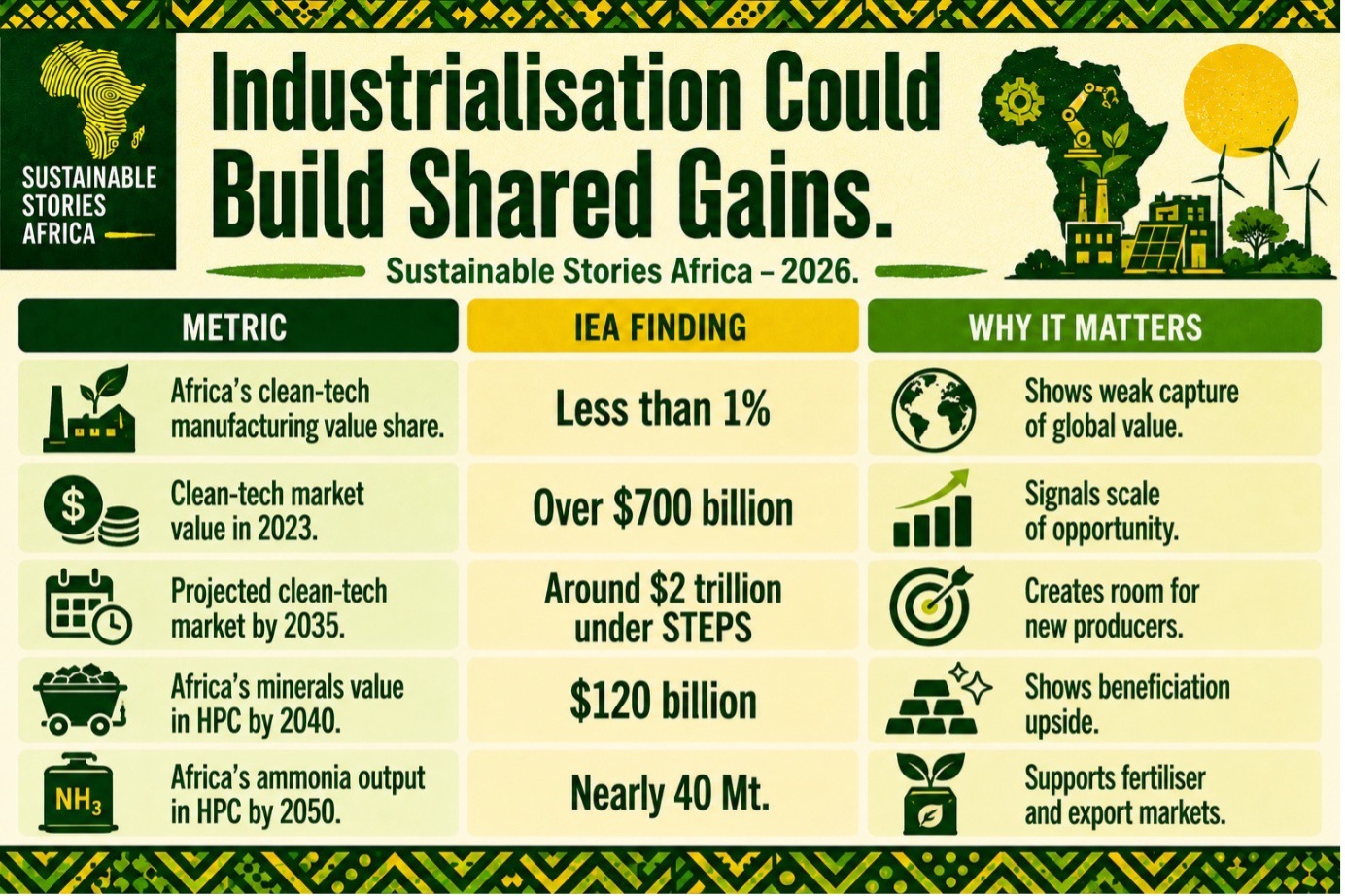

Africa supplies critical minerals to the world. However, captures less than 1% of the clean-energy technology value of manufacturing.

A new IEA report argues that the continent can move from extraction to processing, low-emissions materials and clean-tech manufacturing, if governments, investors and global partners fix energy, infrastructure, finance and skills gaps.

Africa Must Capture More Value

Africa’s clean-energy opportunity is no longer only about what lies beneath its soil. It is increasingly about what the continent can build, refine, manufacture and export from those resources.

A new International Energy Agency report, Stepping Up the Value Chain in Africa: Minerals, materials and manufacturing, says Africa supplies major shares of the world’s unprocessed critical minerals, including about 75% of global manganese, 70% of cobalt and nearly 20% of copper; however, it captures less than 1% of the value generated from clean energy technology manufacturing and components.

The report, prepared as input for South Africa’s 2025 G20 Presidency, frames the issue as an industrialisation test: whether Africa remains a raw-material supplier or becomes a larger player in batteries, electric vehicles, refined minerals, low-emissions ammonia, steel and clean-energy manufacturing.

Africa’s Minerals Tell Bigger Story

The numbers are stark. The global market for six clean-energy technologies, including solar PV, wind, batteries, electric vehicles, heat pumps and electrolysers, was worth more than $700 billion in 2023 and could reach about $2 trillion by 2035 under stated policies. However, Africa accounted for less than 1% of that market.

This matters because clean-energy supply chains are becoming a central pillar of global industrial policy.

Countries are racing to secure minerals, diversify supply chains and localise manufacturing.

However, the current system still rewards those who refine, process and manufacture far more than those who only extract.

For African economies, the risk is familiar: exporting raw materials, importing finished products, and watching value, jobs and technological capability accumulate elsewhere. The IEA says this can change, but only if mineral wealth is converted into an industrial strategy.

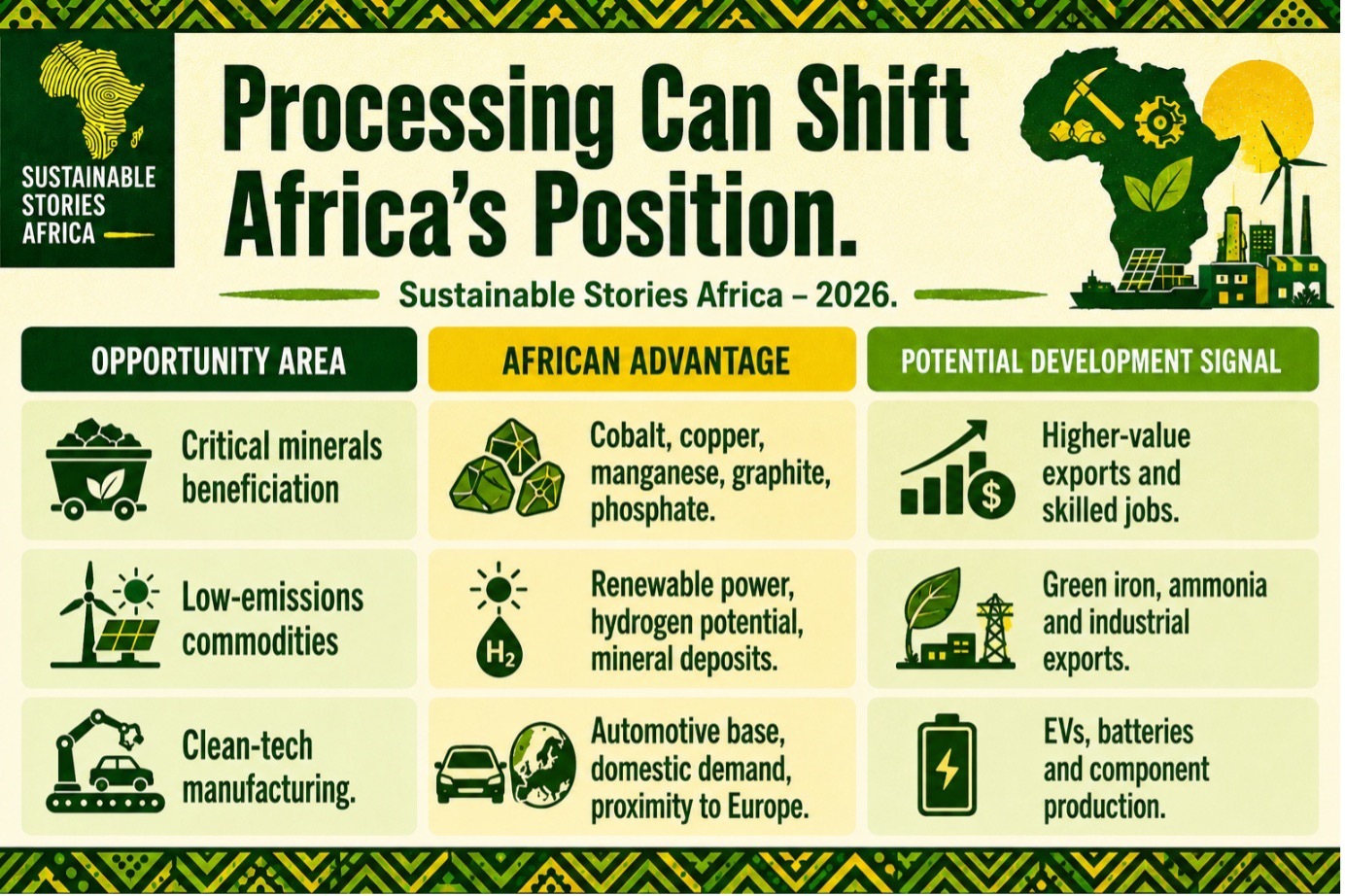

Processing Can Shift Africa’s Position

The IEA identifies three major opportunity areas: critical minerals beneficiation, production of low-emissions energy-intensive commodities, and clean energy technology manufacturing. These are not abstract pathways.

They include copper refining in the DRC and Zambia, spherical graphite production in East Africa, high-purity manganese sulphate in South Africa and Gabon, and purified phosphoric acid in Morocco.

The value upside is significant. In the IEA’s High Potential Case, Africa’s market value from selected minerals could rise by nearly three-quarters to $120 billion by 2040, compared with around $70 billion today.

However, beneficiation is not automatic. The report notes that mining investment has grown faster than refining investment, leaving many countries stuck at the lower-value end of the chain.

In 2024, Africa’s key energy minerals production was worth about $50 billion from mining and $16 billion from refining, showing the gap between resource extraction and value addition.

Industrialisation Could Build Shared Gains

The opportunity goes beyond export revenue. Processing minerals locally can anchor new industrial ecosystems, create demand for engineers and technicians, support logistics and maintenance firms, and justify investment in power, roads, ports and water systems.

Low-emissions commodities could be another route. The IEA says African countries with renewable energy potential and mineral deposits could produce low-emissions iron, steel and ammonia for markets seeking to decarbonise.

In its High Potential Case, low-emissions iron exports to Europe and Asia could be worth more than four times the value of the same tonnage of iron ore exports at today’s prices.

Ammonia is especially strategic because it links energy, agriculture and trade. The report projects that African ammonia production could rise from about 11 million tonnes today to 25 million tonnes in 2035 and nearly 40 million tonnes by 2050 under the High Potential Case, helping eliminate ammonia imports for fertiliser production by mid-century.

Clean-energy technology manufacturing offers a third frontier. North African countries, especially those with existing automotive industries, could strengthen its position in EVs and batteries.

The IEA projects that Africa’s EV production could rise from virtually nothing today to nearly 4 million units by 2035 and 5 million by 2050 in the High Potential Case.

Policy Must Move Beyond Announcements

The report is clear that mineral endowment alone is not enough. Africa’s industrial transition will depend on bankable projects, reliable electricity, efficient transport corridors, skilled labour, predictable regulation and patient capital.

Export bans and local-content rules may help signal ambition; however, they cannot substitute for infrastructure and investor confidence.

The IEA notes that several African countries have introduced beneficiation strategies, fiscal incentives, local content requirements and export controls, but implementation remains uneven.

- Governments need mineral-specific strategies, not generic slogans. Copper refining, graphite processing, manganese sulphate, phosphoric acid, ammonia and EV manufacturing require separate economics, technologies and markets.

- Regulators must also build traceability systems that distinguish raw exports from semi-processed and fully beneficiated products.

- Financiers have a role too. Development banks, export credit agencies and private investors can reduce risk through blended finance, offtake agreements and infrastructure co-investment.

- For global partners, the message is practical: supply-chain diversification should not only secure minerals for advanced economies; it should help build industrial capacity where the minerals are found.

Path Forward – Build African Industrial Value

Africa’s clean-tech opportunity depends on moving from extraction to value creation. Governments should prioritise reliable energy, transport corridors, technical skills, transparent regulation and targeted incentives that make refining and manufacturing commercially viable.

The next step is disciplined implementation. Africa can supply the minerals of the transition; however, the bigger prize is building the factories, materials, jobs and institutions that allow the continent to own more of the clean-energy economy.