Africa entered 2026 with stronger growth, but the Middle East conflict is threatening to turn global disruption into local hardship.

A joint AfDB-led policy paper warns that oil, fertiliser, shipping, currency and financing shocks could hit African households, farms, governments and businesses, especially if the conflict lasts beyond three months.

Africa Faces Another Imported Economic Shock

Africa’s latest economic test is not starting on its farms, factories or finance ministries. It is moving through oil routes, shipping lanes, fertiliser markets and foreign-exchange desks.

A joint policy paper by the African Development Bank, African Union Commission, UN Economic Commission for Africa and UNDP warns that the Middle East conflict, which began on 28 February 2026, has already increased volatility in commodity, financial and stock markets.

The paper says the shock comes as African economies are still managing climate pressures, trade tensions, debt risks and geopolitical fragmentation.

The central question is urgent: can Africa protect its recovery when a conflict outside the continent increases fuel prices, food production, trade logistics, and financial capital?

A Distant War Hits African Markets

The Middle East holds more than 55% of the world’s oil reserves and accounts for nearly 30% of global oil production in 2025.

That makes the region more than a geopolitical theatre; it is a price-setting engine for the global economy.

The joint policy paper says disruptions around the Strait of Hormuz are especially serious because the corridor facilitates about a quarter of global shipments of oil, gas and fertiliser-related commodities.

For Africa, the shock is arriving through five channels: energy prices, fertiliser costs, shipping disruption, capital-flow volatility and geopolitical-security risks.

The continent has shown resilience before. AfDB’s 2026 macroeconomic outlook found that Africa hosted 12 of the world’s 20 fastest-growing economies in 2025, with 22 countries expanding by more than 5%.

However, the new conflict could reverse recent gains for economies dependent on imported fuel, food, fertilisers, as well as external financing.

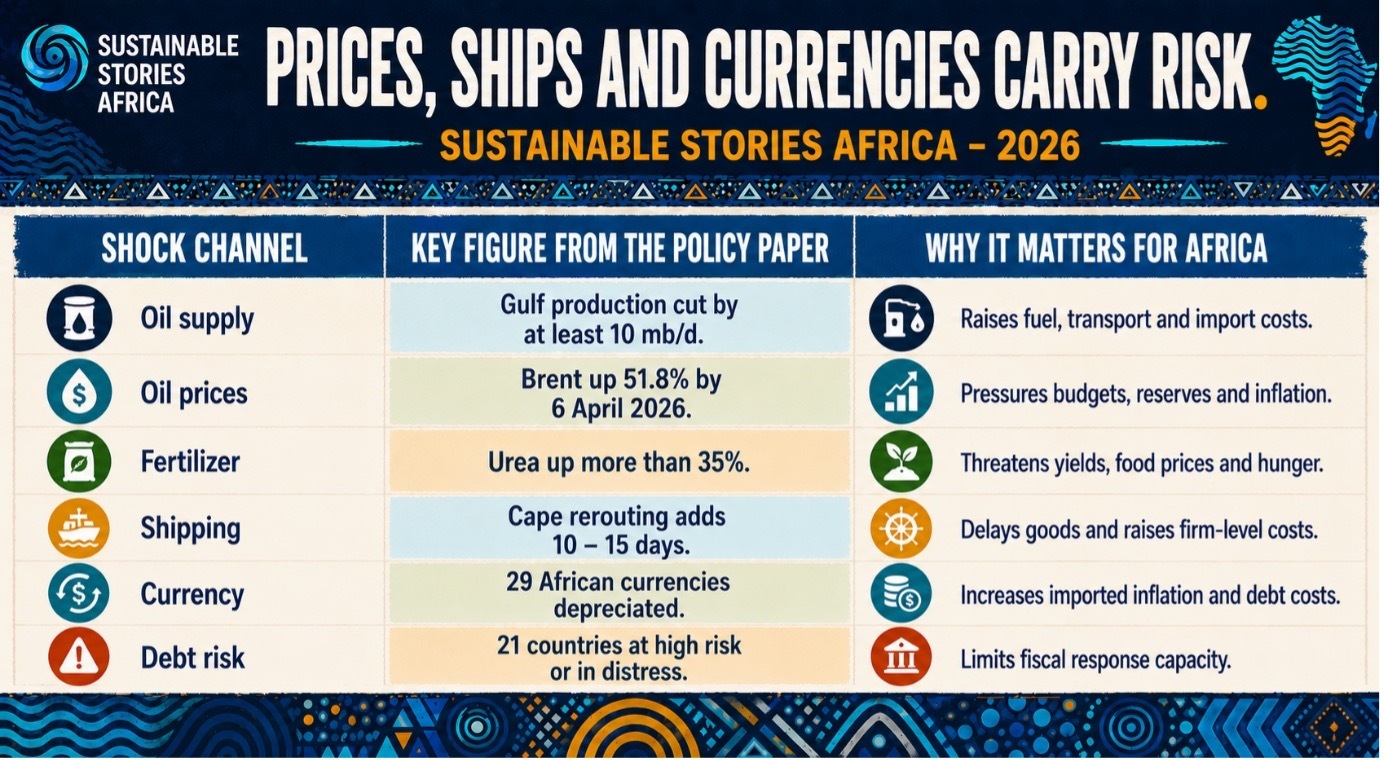

Prices, Ships, and Currencies Carry Risk

The Middle East conflict has created three compounding pressure points for Africa.

- First, oil: shipping traffic through the Strait of Hormuz fell sharply from approximately 109 vessels daily to a near standstill by 22 March 2026. The Gulf producers cut output by at least 10 million barrels per day.

Between 27 February and 6 April, WTI crude rose 68.1%, and Brent climbed 51.8%, from $72.87 to $109.77 per barrel. With 80% of African countries being net oil importers, the exposure is broad and immediate.

- The second pressure point is fertiliser. Urea prices surged more than 35%, from $462.1 per tonne in late February to $621.0 per tonne by 23 March, a shock that hit five major African importers: Sudan, Tanzania, Somalia, Kenya, and Mozambique, precisely during planting seasons, compounding food-security risks.

- Third, logistics disruptions from Suez Canal rerouting to the Cape of Good Hope added 10 – 15 days to transit times and raised freight costs by 20% – 40%, with 13% of Africa's total imports transiting the Strait of Hormuz.

Households Will Feel The First Burden

The most immediate effects of the Middle East conflict will not appear first in GDP figures; they appeared in bus fares, food markets, diesel bills, and shop prices.

Transport accounts for 30% – 50% of final costs in domestic food markets across many African countries, meaning fuel price increases move rapidly through supply chains, hitting poorer households hardest, given that they spend 50% – 60% of their income on food.

Inflation risks are already unevenly distributed. Double-digit inflation is projected for 2026 for Ethiopia, Egypt, Nigeria, Angola, South Sudan, Malawi, Burundi, and Sudan.

This would translate into smaller food portions, delayed planting, higher transport costs, and harder fiscal choices between subsidies, debt service, and social protection.

Currency pressure compounds the strain. Since the conflict began, 29 African currencies have depreciated against the dollar.

A 10% currency depreciation in foreign-exchange-stressed markets can directly translate into a 10% increase in the local-currency cost of imported fuel, fertiliser, and food.

Vulnerability Differs Across African Regions

The impact of rising commodity prices and supply disruptions will not be uniform across Africa's regions.

- East Africa is highly vulnerable; 12 of its 13 countries are net oil importers, with Tanzania, Kenya, and Uganda holding oil import shares of 21%, 15%, and 14% of total imports, respectively, directly exposing households and businesses to higher transport and production costs.

- Central Africa presents a mixed profile, with oil exporters such as Congo, Gabon, and Cameroon gaining short-term fiscal relief. The net importers, including the DRC and the Central African Republic, face heightened inflation.

- North Africa, geographically closer to the conflict, sees Algeria, Egypt, and Libya positioned to benefit from higher oil prices, though subsidies and internal pressures may limit gains.

- Southern Africa remains largely exposed as a net oil-importing region.

- West Africa faces a split outlook. Nigeria benefits from crude prices; however, it faces refined petroleum pressures, and Ghana gains from gold, and tighter global financing conditions could amplify broader vulnerabilities.

Resilience Requires More Than Emergency Relief

The policy paper's central argument is that the current shock should accelerate Africa's economic resilience, not merely trigger another crisis-management response.

Some ports stand to gain from rerouted shipping, with Lamu, Durban, Walvis Bay, and Mauritius potentially benefiting from increased port activity and maritime services.

However, these gains remain uneven and cannot offset broader inflation, fiscal, and food-security pressures.

The deeper opportunity is structural: deepening regional trade under AfCFTA, investing in domestic refining and fertiliser capacity, accelerating renewable energy projects, expanding strategic reserves, and reducing dependence on external financing.

Remittances represent a critical vulnerability. More than 3.6 million Africans work across Gulf states, with GCC remittances reaching $28.3 billion, far exceeding the region's $1.1 billion in official development assistance.

Saudi Arabia alone contributed $12.5 billion, the UAE $8.2 billion, and Qatar $3.7 billion, supporting household incomes across Egypt, Ethiopia, Kenya, Nigeria, and Rwanda, among others.

FDI exposure is equally significant. Africa attracted over $100 billion in global FDI in 2024, with Gulf states playing a growing role, including Qatar's $103 billion investment pledge in 2025 and the UAE's $4.5 billion Green Investment Initiative.

Any Gulf inward turn could leave Africa's infrastructure, energy, and agriculture project pipeline facing a substantial financing gap.

Governments Must Act Before Shock Deepens

The immediate policy response must be targeted, coordinated, and fiscally realistic. Broad fuel subsidies risk draining budgets while disproportionately benefiting higher-income households.

Instead, the paper recommends strategic inflation management, fiscal discipline, targeted social protection, supply diversification, stronger regional trade in oil and fertiliser markets, and tighter coordination between fiscal and monetary authorities, supported by emergency instruments from multilateral development banks and African DFIs.

Medium- and long-term action must go deeper, encompassing faster AfCFTA implementation, domestic capital mobilisation, renewable energy expansion, domestic refining capacity, and initiatives including Mission 300, Desert to Power, and Africa's New Financial Architecture.

Regional financial mechanisms, including the African Financial Stability Mechanism, Africa Shock Swap Mechanism, and the African Credit Rating Agency, are highlighted as essential tools for building continental financial agency.

The scenario analysis is sobering. A one to three-month conflict could reduce Africa's real GDP growth by approximately 0.2 percentage points.

A prolonged disruption of three to six months or more risks deeper growth losses, heightened food-security pressures, and worsening humanitarian conditions across fragile regions.

Path Forward – Build Shock-Ready Economies

Africa’s response should protect households first while building long-term resilience: targeted support, stable prices, food security, credible debt management and coordinated regional action.

The deeper task is structural sovereignty. Africa must trade more with itself, finance more from within, expand clean, reliable energy, secure supply chains, and build institutions capable of absorbing shocks before they become social crises.