Africa entered 2026 with stronger growth, easing inflation and renewed investor interest.

The African Development Bank says the continent remains one of the world’s fastest-growing regions.

However, first-quarter realities are already testing that optimism. Higher energy costs, aid cuts, debt-service pressure and disrupted trade are showing how quickly resilience can become vulnerability.

Africa’s Resilience Meets A Harder Reality

Africa’s economic story in 2026 is no longer just about recovery. It is about whether the continent can defend hard-won macroeconomic gains while absorbing a new wave of global shocks.

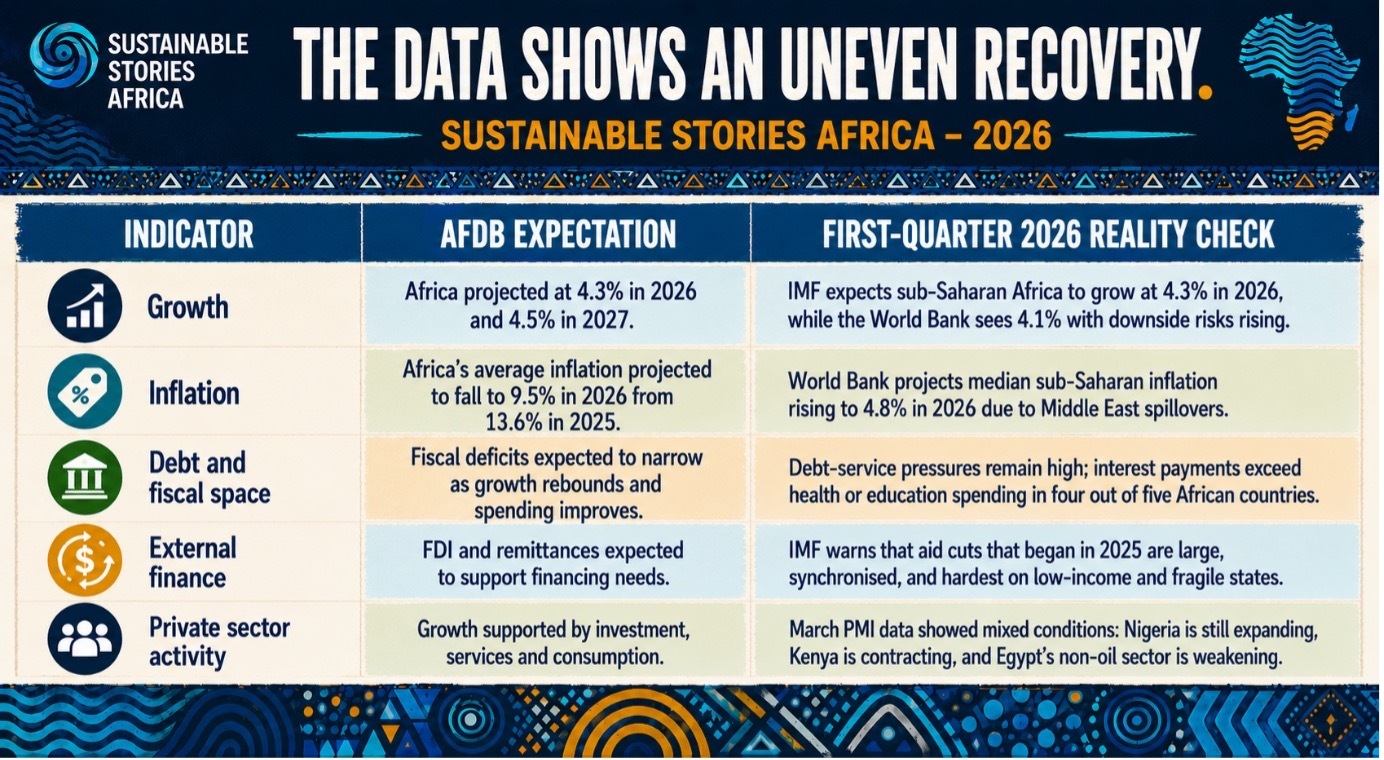

The African Development Bank’s January 2026 Africa’s Macroeconomic Performance and Outlook projects real GDP growth of 4.3% in 2026 and 4.5% in 2027, after an estimated 4.2% expansion in 2025, up from 3.5% in 2024.

The Bank says growth improved in 32 of 54 African economies in 2025, with 22 countries expanding by more than 5%.

However, the first quarter of 2026 has complicated that hopeful baseline. The World Bank now says sub-Saharan Africa’s 2026 growth is holding at 4.1%, unchanged from 2025 but revised down by 0.3 percentage points from its October 2025 forecast, as geopolitical risks, high debt-service burdens and structural constraints weigh on momentum.

Growth Momentum Meets New External Pressure

Africa entered 2026 positioned as a global growth frontier, with the AfDB's outlook anchored in buoyant private consumption, easing monetary conditions, and improving external balances.

However, the first quarter exposed how quickly macroeconomic confidence can erode when households, firms, and governments remain vulnerable to global price shocks.

The World Bank reported that its total commodity price index rose 8% quarter-on-quarter in Q1 2026, reversing earlier disinflation gains. Brent crude climbed from the low $60s per barrel in January to above $100 by early March, while fertiliser and energy disruptions threatened food prices and future harvests, feeding through directly into transport fares, food costs, and higher working-capital pressures for manufacturers, retailers, and farmers.

The IMF captured the shift plainly in April: sub-Saharan Africa entered 2026 with its strongest momentum in a decade; however, the Middle East conflict put those gains under pressure through rising commodity costs, disrupted trade, squeezed remittances, and tighter financial conditions for fuel-importing nations.

The Data Shows An Uneven Recovery

The AfDB’s January view and first-quarter signals are not contradictory. They tell the same story from different moments. Africa’s recovery is real, but it is uneven, exposed and not yet strong enough to transform livelihoods at scale.

The growth divide is regional.

- East Africa remains the continent’s fastest-growing region, projected by AfDB to remain above 6% in 2026, supported by domestic demand, services and investment.

- West Africa is expected to hold near 4.6%.

- North Africa benefits from tourism, extractives and agricultural recovery.

- Southern Africa remains the weakest growth pole, constrained by electricity shortages, logistics bottlenecks and subdued external demand.

The private-sector data shows the lived version of that divergence.

- Nigeria’s March PMI remained in expansion at 51.9, though growth slowed as higher fuel costs intensified inflationary pressure.

- Kenya’s PMI fell to 47.7 in March, its first deterioration since August 2025, as businesses reported weaker output, softer orders, tighter household budgets and logistics constraints.

- Egypt’s non-oil PMI fell to 48.0 in March, its lowest level in almost two years, as demand weakened and prices rose.

This is the central lesson: Africa’s macro recovery is not yet automatically translating into broad-based business confidence.

Firms are still navigating fuel costs, currency movements, shipping uncertainty, high borrowing costs and cautious consumers.

Stability Can Become Jobs And Investment

The opportunity is that Africa’s 2026 outlook still maintains a pathway of transformation.

The AfDB argues that the continent can convert resilience into sustained prosperity by combining macroeconomic stabilisation with structural reforms, productive infrastructure, domestic resource mobilisation, diaspora capital, improved public investment efficiency and deeper regional integration under AfCFTA.

That agenda matters because Africa does not only need growth. It needs job-rich growth. AfDB notes that current growth remains below what is required to lift millions out of poverty.

The IMF says structural reforms could crowd in private investment and lift output by up to 20% over five to ten years if reforms are well-sequenced, bundled and supported by stronger state capacity.

The financing story is equally important. AfDB reports that FDI to Africa rebounded strongly in 2024, rising by more than 75% to $97 billion, while remittances rose by more than 14% to $104.6 billion, making them Africa’s largest non-debt source of foreign inflows.

However, the realities of the first quarter show why external finance cannot be taken for granted. IMF says the aid contraction that began in 2025 is different in scale, speed and breadth, with low-income and fragile states hit hardest.

It estimates a 16% – 28% cut in bilateral aid in 2025, at a time when domestic fiscal space is already tight after years of shocks.

For citizens, the policy stakes are practical. Better fiscal management can mean more money for roads, clinics and schools. Lower remittance costs can put more money in household hands.

Stronger regional trade can help farmers, logistics firms and manufacturers reach larger markets.

More reliable energy can help businesses produce without passing every cost shock to consumers.

Governments Must Turn Forecasts Into Buffers

The AfDB's prescription is unambiguous: African governments must rebuild macroeconomic buffers while accelerating structural transformation.

That requires coordinated monetary, fiscal, and exchange-rate policies to contain inflation, protect financial stability, and sustain credit flows to productive sectors, alongside tighter scrutiny of recurrent expenditure, subsidies, and state-owned enterprise losses.

Debt management has become central to Africa's development narrative. While the World Bank notes that primary fiscal deficits in sub-Saharan Africa are edging toward balance, overall deficits remain elevated due to high net interest payments.

External public debt service-to-revenue is projected to rise from 15.4% in 2024 to approximately 18.2% in 2025, with annual repayments expected to remain between $47 billion and $50 billion over 2026 – 2028.

Reform, however, cannot stop at stabilisation. African countries need deeper domestic capital markets, stronger tax systems, transparent debt reporting, credible fiscal rules, and improved public investment governance.

Industrial strategies must be selective, accountable, and explicitly linked to job creation rather than broad commitments that dilute scarce resources.

The first quarter of 2026 has made one point unavoidable: the countries best positioned to absorb shocks will be those combining stronger institutions, diversified exports, flexible exchange-rate systems, credible monetary policy, and targeted social protection for vulnerable households.

Path Forward – Protect Gains, Build Buffers

Africa’s 2026 growth story remains positive, but the first quarter has narrowed the margin for policy error.

Governments must protect disinflation gains, manage debt transparently, shield vulnerable households and keep investment flowing into productive sectors.

The priority is not just faster growth. It is stronger, fairer and more resilient growth, powered by infrastructure, regional trade, private investment, domestic finance and reforms that turn macro stability into jobs.