Climate shocks are no longer distant variables in investment memos. They are already hitting assets, supply chains, communities and business models, forcing climate finance to move from broad intent to disciplined risk management.

A guide from Climate Policy Initiative argues that assessing climate risk, clearly defining resilience, and measuring outcomes credibly are becoming the new baseline for climate finance vehicles seeking investor trust, public funding and real-world impact.

Climate Finance Must Now Prove Resilience

Climate finance is entering a more demanding phase. The January 2026 guide, Assessing Climate Risk, Framing Resilience, and Reporting Impact: A Guide for Climate Finance Practitioners, states that all investment vehicles must now embed climate risk management design and execution to remain viable and effective.

The shift is significant. What was once treated as a specialist concern for adaptation experts is now being framed as a core discipline for fund managers, investors, implementers and technical partners.

That matters for African and emerging markets because climate hazards are not theoretical. Droughts, floods, extreme heat, storms and sea level rise are already damaging livelihoods, infrastructure, supply chains and productive assets.

In markets where exposure is often high and buffers are thin, poor climate-risk discipline can quickly become a problem for financing, development and credibility all at once.

The guide is built around three linked goals:

- First, assess and manage climate risk

- Second, define an adaptation thesis

- Third, design a fit-for-purpose impact measurement and reporting strategy.

That sequence is more than technical housekeeping. It amounts to a new logic for climate finance: understand the hazard, explain how your intervention reduces vulnerability, then prove the result.

The Cost of Ignoring Risk

Climate risk is now a material financial concern. Evidence cited in the report shows 200 of the world's largest companies have an estimated more than $1 trillion in climate-related financial exposure, a figure that signals systemic risk to enterprise performance, investor confidence and asset value.

Climate risk assessment now serves four functions:

- Protecting business performance

- Reducing maladaptation risk, where interventions inadvertently worsen vulnerability

- Supporting alignment with ISSB Standards, the global baseline for climate-related financial disclosure

- Qualifying projects for Paris-aligned public funding, increasingly required by multilateral development banks.

For African markets, the stakes are compounded. Infrastructure deficits, food system fragility, and informal economic dependence mean that climate investments that appear efficient on paper can still fail if they ignore flood exposure, water stress, heat impacts, and the vulnerability of women, smallholders and low-income households.

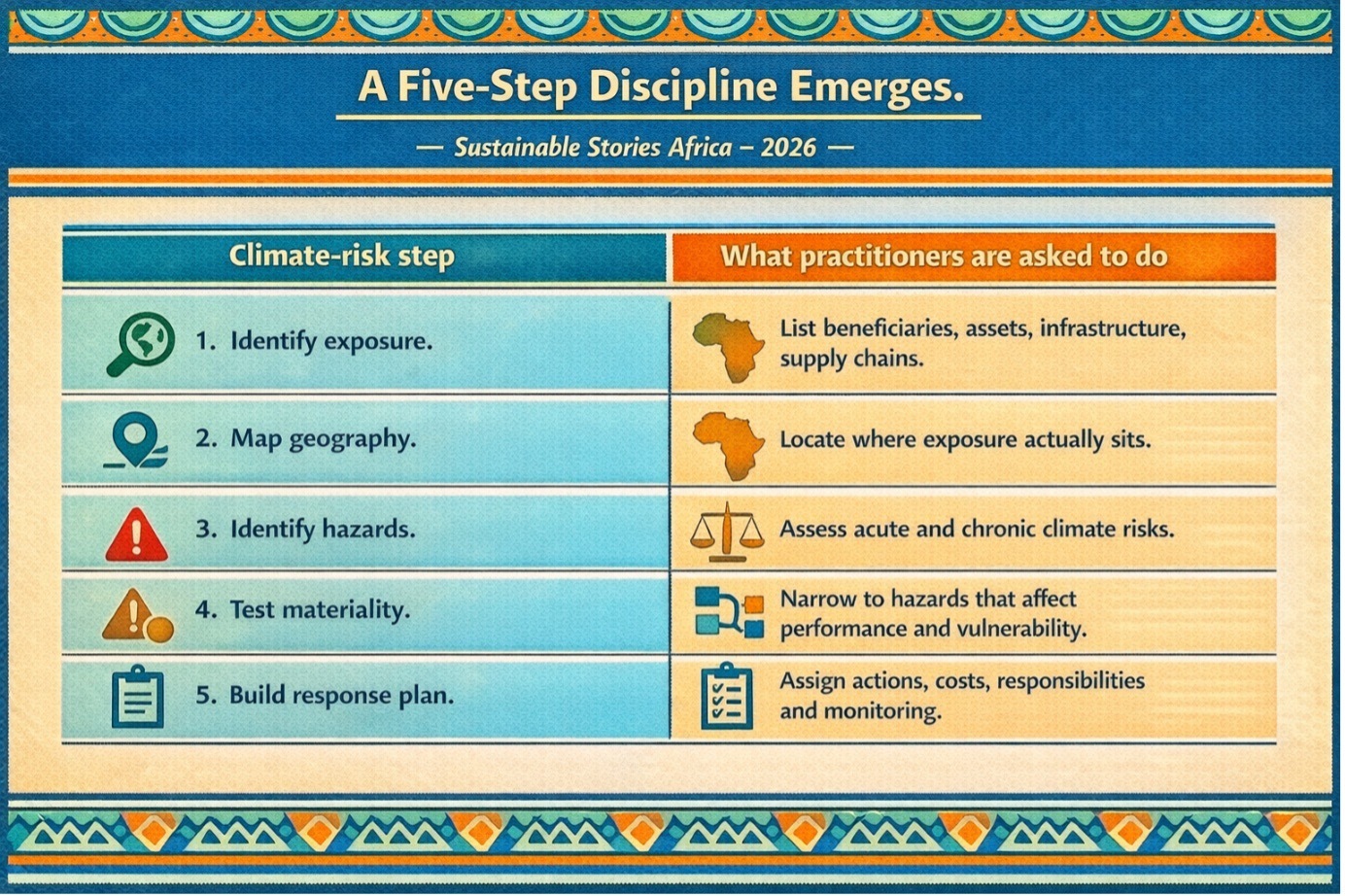

A Five-Step Discipline Emerges

The guide’s most practical contribution is its five-step structure for assessing and beginning to manage climate risk.

- First, list all end users, beneficiaries, assets, infrastructure and supply chain nodes.

- Second, map their geographic boundaries.

- Third, identify relevant acute and chronic climate hazards.

- Fourth, narrow those hazards to the materially relevant ones.

- Fifth, build a management plan.

Climate hazards fall into two categories that practitioners must track separately.

- Acute hazards, including heatwaves, wildfires, cyclones, flooding and heavy precipitation, strike suddenly.

- Chronic hazards, such as shifting temperatures, drought, sea-level rise and coastal erosion, erode resilience over time.

The guide urges scenario planning across multiple climate pathways, cautioning against single-view risk assessments that routinely underestimate exposure

An East African agriculture case makes the stakes concrete.

A climate-smart irrigation company operating across Kenya, Tanzania and Uganda faces compounding risks: rising drought, erratic rainfall, heat stress and intensifying floods.

Droughts that once struck every five to six years before 1999 now occur every two to three years, with drought exposure in East Africa projected to rise by up to 54% by the end of the century.

Sub-Saharan Africa has recorded a tenfold increase in flood events since the 1970s.

Kenya's 2018 floods alone displaced over 230,000 people, destroyed 8,500 hectares of crops and killed more than 20,000 livestock.

Page 19 lists six hazard-mapping tools. These include the World Bank Climate Change Knowledge Portal, ThinkHazard!, WRI Aqueduct Water Risk Atlas, UCT Climate Information Platform, the European Commission’s INFORM Climate Change Tool, and South Africa’s CSIR Green Book. It also flags limitations, including low spatial resolution and sectoral gaps, reminding practitioners that due diligence remains essential.

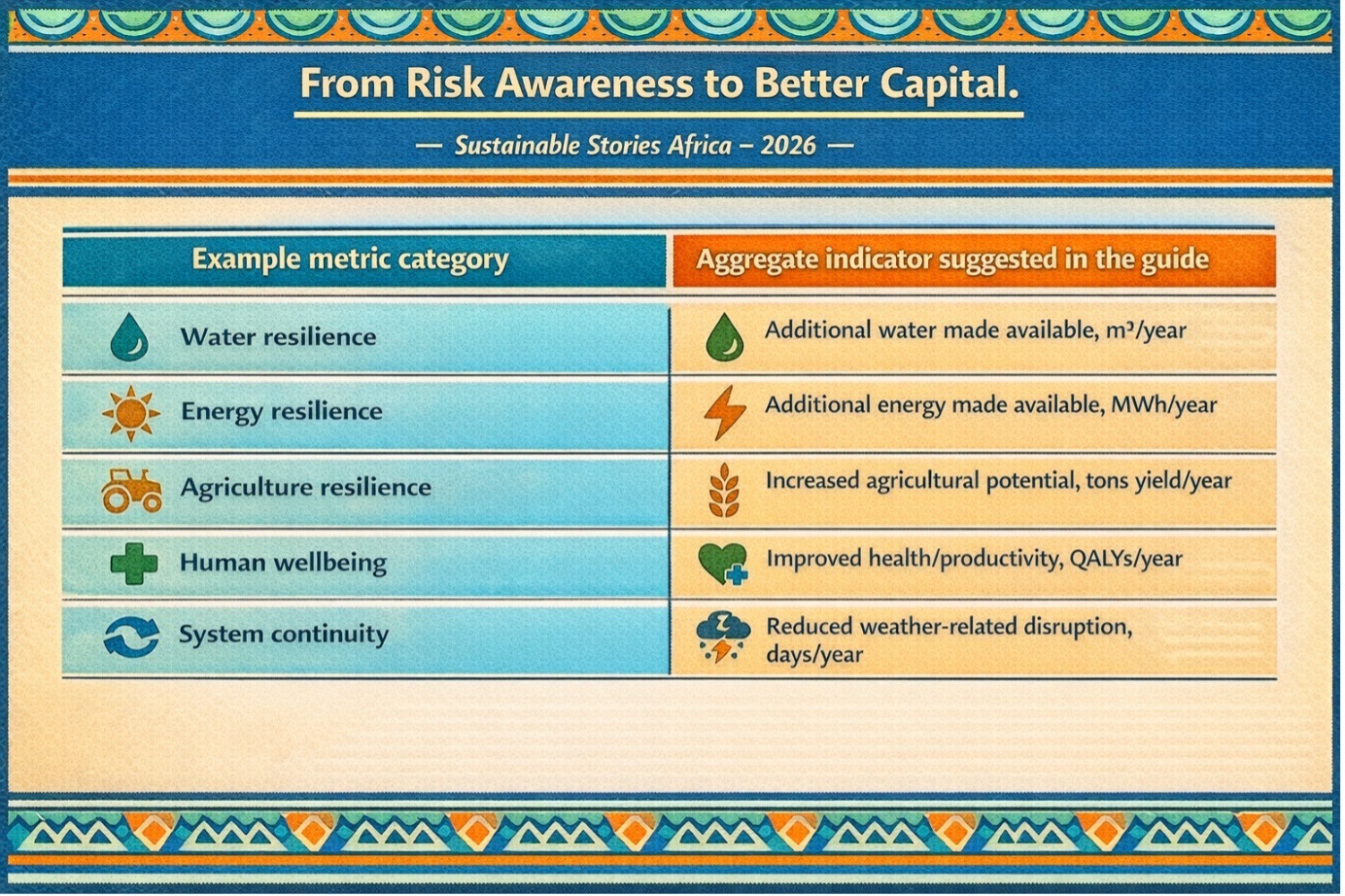

From Risk Awareness to Better Capital

Better climate risk assessment is not only about avoiding losses; it can improve bankability and unlock new capital.

Two cases illustrate this.

- Cooling as a Service entered CPI's support process, focused on emissions reduction, rather than a climate-risk assessment, which revealed adaptation co-benefits, reduced food waste, improved labour productivity and protected cold-chain medicines, which helped attract a new set of funders.

- CRAFT, the Climate Resilience and Adaptation Finance and Technology Transfer Facility, used CPI's support to sharpen its adaptation thesis and align with Green Climate Fund criteria, securing a $100 million GCF commitment across six new countries.

For African markets, the development case is equally compelling. Strong impact measurement helps prioritise investments, guard against maladaptation and satisfy donor demands for quantitative metrics.

The guide wisely recommends contextual approaches over universal templates, recognising that data collection across African geographies and gender lines remains costly and uneven.

What African Markets Should Do

For African financiers, DFIs, regulators and project developers, the practical lesson is direct: resilience must move from broad aspiration to operational discipline.

That begins with governance. Boards need clearer oversight of physical climate risk; investment committees must assess hazards across beneficiaries, assets and value chains, rather than just company headquarters.

The sample criteria on page 18 are instructive: credible climate finance now means asking whether a site is flood-exposed, whether workers can safely function in extreme heat and whether company reporting aligns with investor standards.

Adaptation framing also needs sharpening.

A credible adaptation thesis must define the context of climate vulnerability, state an explicit intention to reduce that vulnerability and draw a direct line between project activities and resilience outcomes.

This is a growing requirement for MDB and public investment vehicles. In African markets, where adaptation finance remains chronically underprovided, stronger adaptation theses could move more projects from concept to credible pipeline.

Finally, measurement must become more honest and practical. The guide recommends stakeholder-relevant metrics, pre-intervention baselines, gender-disaggregated tracking where feasible and data plans that organisations can realistically deliver, a timely corrective for a field that sometimes confuses ambition with measurement capacity.

Path Forward Starts With Discipline

What is being advocated is not just more climate finance, but better-prepared climate finance: risk-tested, clearly framed, and measured against resilience outcomes that matter to beneficiaries and investors alike.

For African markets, the opportunity is significant. The vehicles that map hazards properly, avoid maladaptation, build strong adaptation theses, and report results credibly will be better placed to attract capital and deliver resilience where it is needed most.