Global electricity demand is rising faster than legacy systems can absorb. The IEA says cooling, data centres, EVs and industrial electrification are pushing the world into a new electricity age.

For Africa, that shift brings opportunity and pressure together: access gaps, weak grids, high costs and reliability risks now matter as much as generation targets.

Electricity’s surge is redrawing development maps

The International Energy Agency’s Electricity 2026 report arrives with a message that is hard to miss: electricity is no longer simply following economic growth.

It is beginning to outpace it. Global electricity demand is forecast to grow by 3.6% a year from 2026 to 2030, taking consumption to 33 600 TWh by the end of the decade.

That is not just an energy statistic. It is a development signal. The report describes a world where industry, electric vehicles, space cooling, data centres and digital infrastructure are all pulling harder on power systems at once, forcing grids, storage, pricing and reliability to move from the margins to the centre of policy.

For African markets, the stakes are even sharper. Demand on the continent rose 5.2% in 2025 and is forecast to grow by about 3.9% annually through 2030, yet around 600 million people in sub-Saharan Africa still lack reliable electricity.

In this new electricity economy, generation alone will not be enough. Access, resilience and affordability will matter just as much.

Power demand now outruns legacy systems

Global electricity demand grew faster than the economy in 2024, the first normal increase of its kind in 30 years, signalling a structural shift in energy use.

The IEA now projects annual demand growth through 2030 to be 50% above the previous decade’s average. Nearly half (49%) of additional demand between 2025 and 2030 will come from buildings, driven by cooling, heat pumps and data centres.

Transport’s share will exceed 10%, boosted by electric vehicles, while electricity’s share of total final consumption will rise from 21% in 2025 to 24% in 2030.

For Africa and other emerging markets, this surge underscores the need for power systems that can handle faster, weather-sensitive and digitally intensive demand.

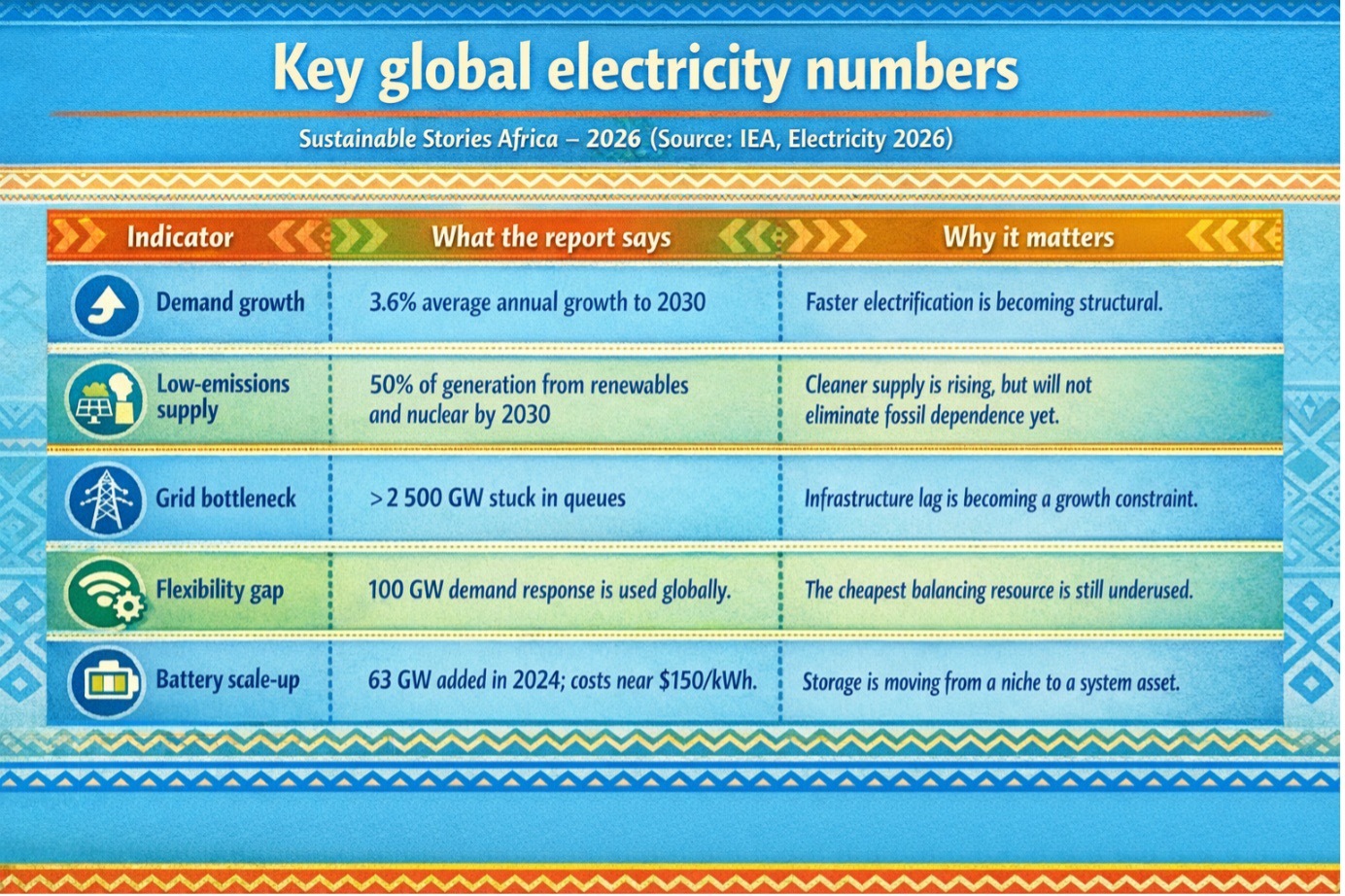

Eight metrics defining the next power era

- 3.6%: That is the IEA’s expected average annual growth rate for global electricity demand from 2026 to 2030, equivalent to roughly 1 100 TWh of extra demand each year.

- 80%: Emerging markets and developing economies are expected to account for nearly 80% of additional electricity consumption through 2030. China alone is forecast to deliver close to half of the increase, while India is expected to grow at 6.4% annually and Southeast Asia at 5.3%.

- 50%: Renewables and nuclear together are expected to provide around half of global electricity generation by 2030, up from 42% in 2025. Renewable generation is forecast to rise by roughly 1 050 TWh each year, with solar PV alone contributing more than 600 TWh annually.

- 27%: Coal is set to lose share, falling from 34% of the electricity mix in 2025 to 27% by 2030, but it will still remain the single largest individual source of generation globally. That is a reminder that transition does not mean immediate replacement.

- 2 500 GW: More than 2 500 GW of projects, spanning renewables, storage and large loads such as data centres, are stalled in grid connection queues worldwide. The IEA says annual grid investment must rise about 50% by 2030 from today’s USD 400 billion.

- 1 200 - 1 600 GW: That much advanced-stage capacity could be unlocked through regulatory reform and grid-enhancing technologies. The report estimates 750-900 GW could come from more flexible non-firm connection agreements, with another 450-700 GW enabled by technologies such as dynamic line rating, power-flow control, reconductoring and voltage uprating.

- 100 GW and 63 GW: Only around 100 GW of demand response is currently used globally, despite far larger potential from industry and buildings. At the same time, utility-scale batteries added 63 GW in 2024, taking global installed capacity to 124 GW, while project costs fell about 40% to around USD 150/kWh.

- 13 900 Mt CO2, 6% negative-price hours, and major blackouts: Power-sector emissions are forecast to plateau through 2030 at around 13 900 Mt CO2 annually even as global CO2 intensity falls. But affordability and reliability remain unsettled: some European markets recorded negative prices for around 6% of hours in 2025, while blackouts in Chile, the Iberian Peninsula and Mexico exposed how fragile stressed systems can still be.

Africa can still shape better outcomes

Africa’s latest electricity outlook reads as both caution and blueprint. Power demand grew 5.2% in 2025 and is projected to rise around 3.9% annually through 2030, supported by improved supply in South Africa.

Kenya and Senegal are moving steadily toward universal access, while Nigeria is scaling off-grid and distributed solar to close its access gap.

Natural gas still provides over 40% of Africa’s generation, but about 28% of additional supply to 2030 is expected from solar PV, roughly 55 TWh, alongside more hydro, wind and nuclear.

A hybrid, infrastructure-heavy approach that expands access while reinforcing transmission, distribution, storage, metering and demand management could unlock more reliable power, lower diesel use, and a stronger industrial base, but grid bottlenecks remain a critical risk.

Build whole systems, not just megawatts

The IEA's core policy lesson is clear: electricity strategy can no longer end at generation targets.

- Regulators must streamline connection processes

- Utilities need better monitoring

- Voltage management and reserves

- Governments must treat storage

- Demand response and grid-enhancing technologies as core infrastructure.

Price reform is equally urgent; household electricity costs in many countries have risen faster than incomes since 2019, and taxes on electricity outweigh those on natural gas, undermining the case for electrification.

For African markets, five priorities stand out: modernise and expand grids; reduce connection bottlenecks; create investable frameworks for storage and flexible demand; protect affordability without distorting long-term efficiency; and treat reliability as a strategic economic asset.

The new electricity age rewards countries that connect, balance, price, and protect power rather than produce more of it.

Path Forward – Build grids before shortages become permanent

Africa’s electricity opportunity is real, but it will be captured only if access, grid capacity, flexibility and affordability advance together.

The report argues for a shift from generation-first planning to system-first planning.

That means faster networks, smarter regulation, wider use of storage and demand response, and stronger protection against outages and weather shocks. In the electricity decade ahead, resilience will be just as valuable as capacity.