Europe’s ESG architecture is no longer one big compliance block. CSRD and CSDDD target different corporate duties, timelines and thresholds; however, together they are reshaping how companies demonstrate sustainability, risk control and supply chain integrity.

For African exporters, subsidiaries, financiers and suppliers, the issue is practical.

Which rule applies, when does it start, and how should businesses prepare when disclosure obligations and due diligence duties begin to overlap in real commercial life?

Two ESG Rules, Different Demands

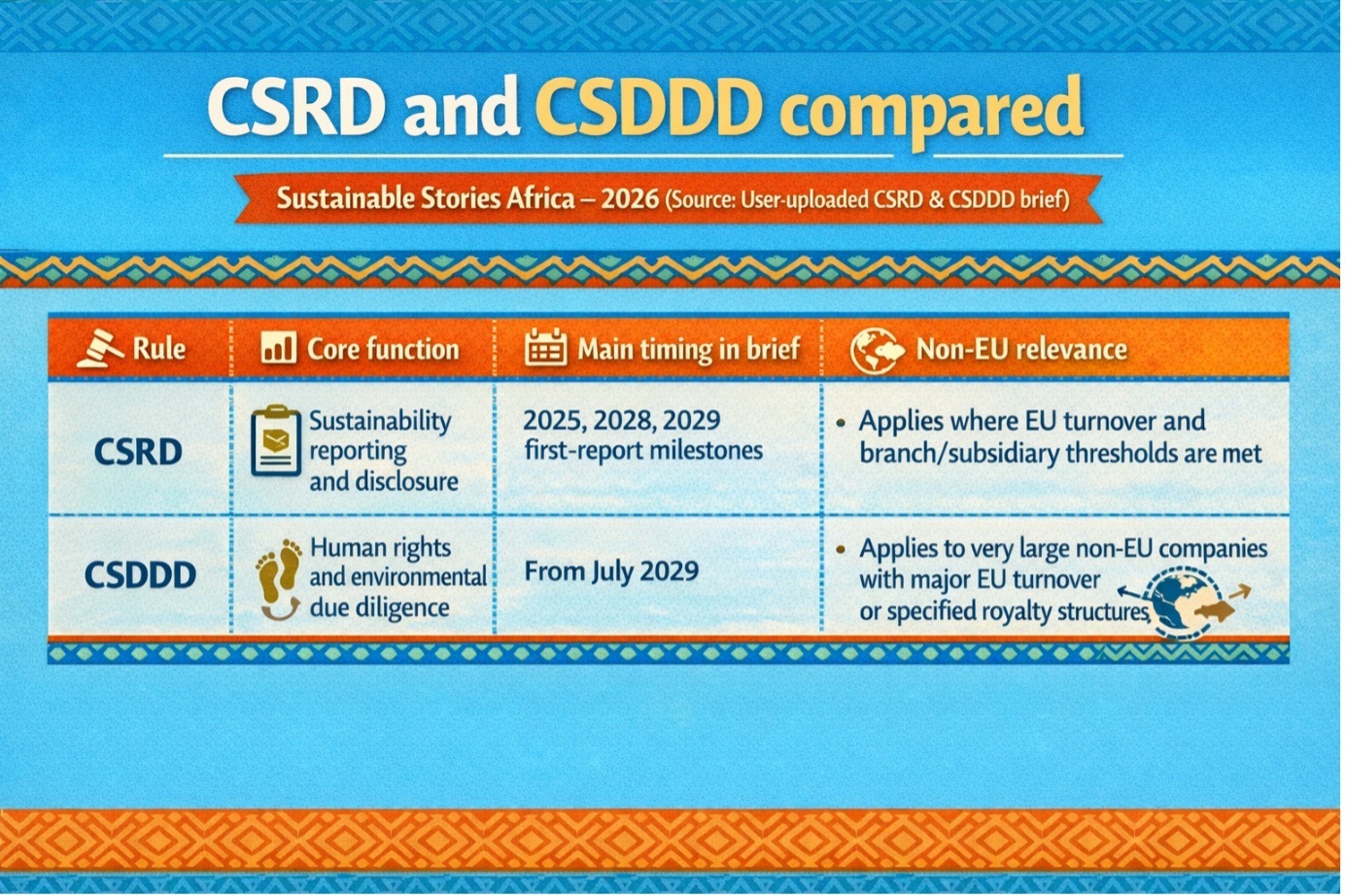

Europe’s sustainability regime is becoming more precise, not simpler. The new compliance picture shows that the Corporate Sustainability Reporting Directive, or CSRD, and the Corporate Sustainability Due Diligence Directive, or CSDDD, do different jobs.

CSRD is about reporting: who must disclose sustainability information, on what timeline, and with what visibility to investors, regulators and markets.

CSDDD is about conduct: who must carry out human-rights and environmental due diligence across operations and value chains.

That distinction matters now because the timelines are beginning to harden. The infographic in the uploaded brief sets out a staggered CSRD timetable, starting with former “Wave 1” companies already covered by the NFRD for 2024 data reported in 2025, then other large companies for 2027 data reported in 2028, and non-EU groups for 2028 data reported in 2029 if they meet the EU turnover and branch or subsidiary thresholds.

The same brief shows CSDDD beginning from July 2029 for defined EU and non-EU companies above much larger size or turnover thresholds.

For African and wider Global South markets, that means two pressures are arriving from Europe at once.

One asks companies to disclose more clearly. The other asks them to manage risks more credibly.

CSRD Reports What You Do. CSDDD Demands You Change What You Do.

The costliest mistake companies make is treating CSRD and CSDDD as interchangeable.

They are structurally different obligations.

- CSRD is a reporting regime; it asks what material sustainability impacts, risks, and governance arrangements exist, and whether they can be disclosed credibly.

- CSDDD is a due diligence regime; it demands active identification, prevention, mitigation, and remedy of harm across operations and value chains. That distinction changes budgets, teams, and risk exposure.

A company may enter CSRD's reporting perimeter before CSDDD applies directly; however, companies residing outside both legal thresholds can still feel the effects through supplier codes, customer questionnaires, procurement screens, and group-level compliance demands.

The thresholds clarify the separation.

- CSRD's "other large companies" threshold is over 1,000 employees and turnover of €450 million, with first reports due in 2028 on 2027 data; non-EU groups enter scope for 2028 data reported in 2029, where EU net turnover exceeds €450 million and subsidiary or branch turnover exceeds €200 million.

- CSDDD applies from July 2029 to EU companies exceeding 5,000 employees and €1.5 billion turnover, and to non-EU companies with over €1.5 billion in EU turnover, a higher bar, but a harder obligation.

What Does The Difference Mean In Practice

The reporting side is already more immediate. The table on page 2 of the brief shows that former NFRD reporters are already within the CSRD timeline, while other large companies and qualifying non-EU groups come in later.

That means the market is already generating disclosure expectations, templates and assurance habits that will spread beyond the legal minimum.

The due diligence side is narrower on paper but potentially deeper in business effect.

The page 3 table shows CSDDD applying only from July 2029 and only to very large companies or those with substantial royalties from franchising or licensing arrangements.

However, those firms sit at the top of many global value chains. When they move, suppliers move too.

For African producers, this is where local realities come in.

A cocoa exporter in West Africa may never directly cross a European legal threshold, but a European buyer subject to CSRD may request emissions, labour and traceability data.

A buyer exposed to CSDDD may ask tougher questions about remediation systems, sourcing risks, community impacts and business-partner oversight.

The formal law may sit in Brussels, but the operational pressure lands in farms, factories, logistics hubs and boardrooms across emerging markets.

Why Clarity Could Still Be Good Business

There is a positive side to this regulatory split. It gives companies a cleaner map. Businesses can separate the work of disclosure from the work of operational due diligence, even if the two increasingly reinforce each other.

That makes governance more disciplined. Finance teams, sustainability teams, legal advisers, procurement leads, and boards can assign responsibilities more clearly.

For African markets, this can become a competitive advantage.

- Firms that build credible reporting systems early will be better placed to respond to investor scrutiny, retain export relationships and negotiate with multinational customers.

- Firms that also strengthen supplier oversight, grievance channels, traceability and risk-management systems will be more resilient when due diligence expectations intensify.

This is where language simplification matters. Companies do not need to become legal theorists.

They need to understand that Europe is dividing ESG into two practical tests: can you report responsibly, and can you operate responsibly?

What African Businesses Should Do Next

- The first step is classification. Companies need to determine whether they are directly in scope for CSRD, directly in scope for CSDDD, indirectly exposed through customers or financiers, or likely to be affected by supply chain requirements. That sounds basic, but it prevents wasted effort and weak prioritisation.

- The second step is system design. Businesses with European exposure should build a minimum ESG architecture now: board visibility, documented sustainability risks, auditable data trails, supplier information channels, and escalation routes for labour, environmental and integrity concerns. Even where CSDDD is years away or legally indirect, commercial expectations will arrive earlier.

- The third step is relationship strategy. African regulators, trade bodies, business associations and financiers should help local firms understand that these are not just European legal texts; they are market filters. Companies that wait for formal notices may discover that customers have already moved.

Path Forward – Reporting First, Conduct Next

Europe’s ESG rulebook is separating disclosure from due diligence, but markets will join them back together in practice. Companies that understand the distinction early will prepare faster and spend smarter.

For African markets, the priority is clear: map exposure, strengthen data, improve supplier visibility and build credible integrity systems now. The firms that do so will not just stay compliant. They will stay commercially relevant.