Energy transition delays are no longer only a climate problem. They are becoming a balance-of-payments problem for countries that still rely heavily on imported oil and gas.

Atradius’ March 2026 Energy Outlook argues that slower decarbonisation, weak electrification and persistent financing bottlenecks could leave many fuel-importing economies paying more for energy, for longer.

For African and other emerging markets, that means rising pressure on currencies, reserves and growth.

Fuel risk is becoming structural

The warning from the Atradius Energy Outlook Report is blunt: the global energy transition is slowing, fossil-fuel demand is expected to peak later than previously hoped, and oil and gas prices may stay structurally higher for longer.

That matters far beyond climate diplomacy. For fuel-importing economies, especially in emerging markets, it raises a more immediate question: how long can fragile external balances absorb repeated energy-price shocks?

The report’s core argument is that the world’s slower transition away from fossil fuels is creating a deeper economic vulnerability for countries that import large volumes of fuel.

Atradius notes that price spikes linked to the war in the Middle East have already exposed this weakness in the short term, while the medium-term outlook now looks less favourable than it did a year ago.

For Africa, where energy demand is rising quickly, and financing constraints remain severe, the report reads as both diagnosis and warning.

Renewable investment remains too slow, electrification outside the power sector is weak, and the cost of inaction is likely to show up not only in emissions, but in current-account stress, weaker resilience and reduced policy room.

A harsher energy reality emerges

Atradius treats the latest IEA outlook as a pivot point, with the pessimistic Current Policies Scenario back in focus and the Stated Policies Scenario now pointing to a more fossil‑intensive energy mix than previously expected.

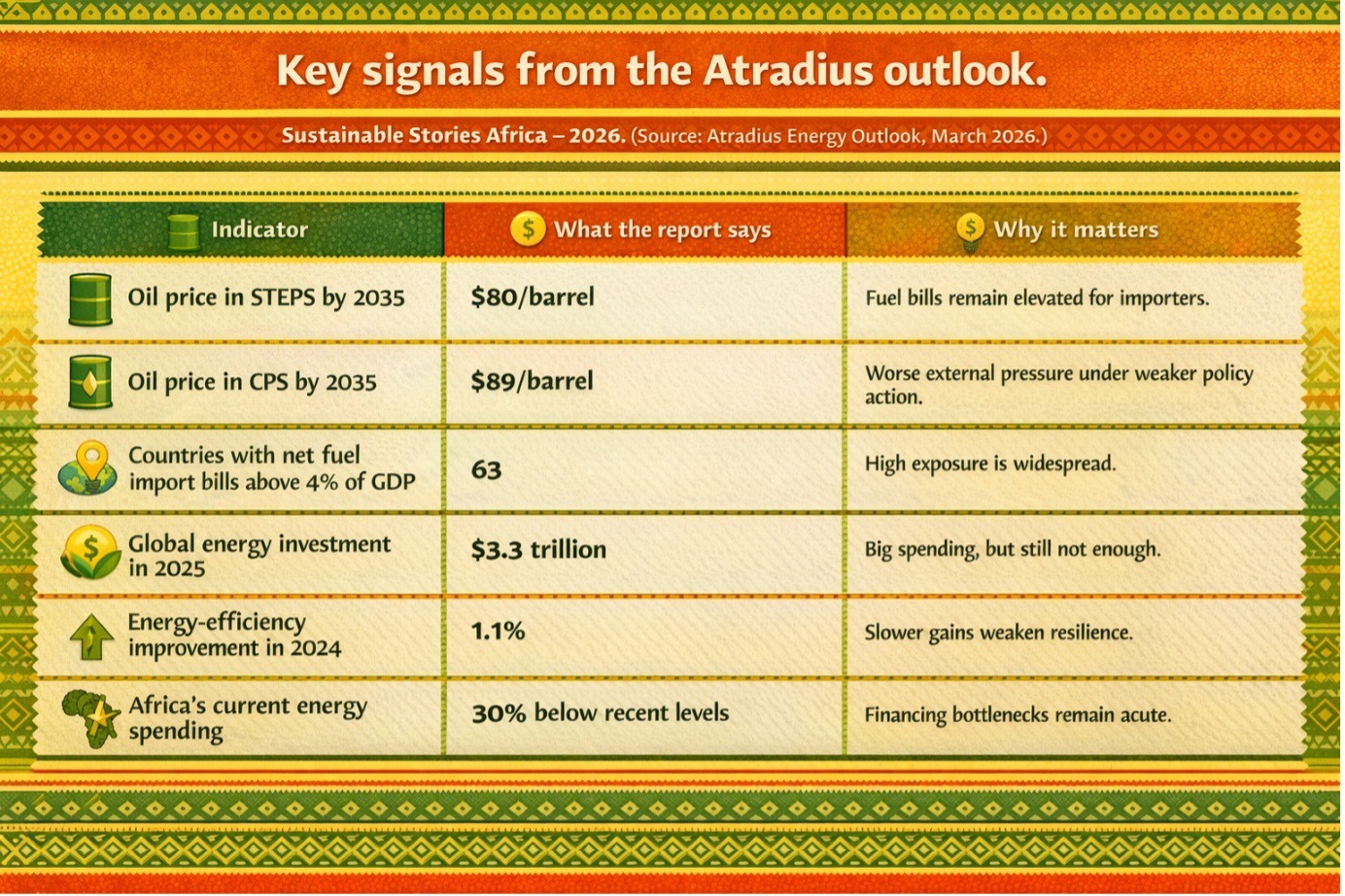

In this framing, the world still tracks toward about 2.5°C of warming under STEPS and roughly 3°C under CPS by 2100, with oil prices revolving between $90 and $130 currently and projected to remain at about $80 per barrel by 2035 in STEPS and toward about $89 per barrel and still climbing in CPS.

Natural gas prices also remain firmer than earlier projections, particularly in the adverse scenario. For fuel‑importing countries, this is a macro warning: using 2024 UNCTAD data, Atradius flags 63 economies where net fuel imports exceed 4% of GDP, nearly 50 of which already run current‑account deficits above 5% of GDP.

Why is the transition stalling

Atradius breaks the energy transition into three channels:

- Efficiency

- Electrification

- Shifting away from fossil fuels

The report argues that all are advancing too slowly. Global energy investment reached about $3.2 trillion in 2024 and is estimated at $3.3 trillion in 2025, but the scale and mix remain inadequate.

Efficiency gains have weakened from an average of 2% per year between 2010 and 2019 to 1.1% in 2024.

Grid investment has fallen from 60% to 40% per dollar of generation, reflecting permitting delays, supply chain strain and electricity security concerns. The gap is sharpest in emerging markets: Africa’s fast-rising energy demand is being met with spending roughly 30% below recent levels, constrained by high capital costs, perceived risk and weak execution.

Technology prices are falling, solar down nearly 45% from 2023, Chinese batteries about 30% in 2024, but a cheaper kit cannot compensate for mixed policy signals and uneven investment.

What faster reform could unlock

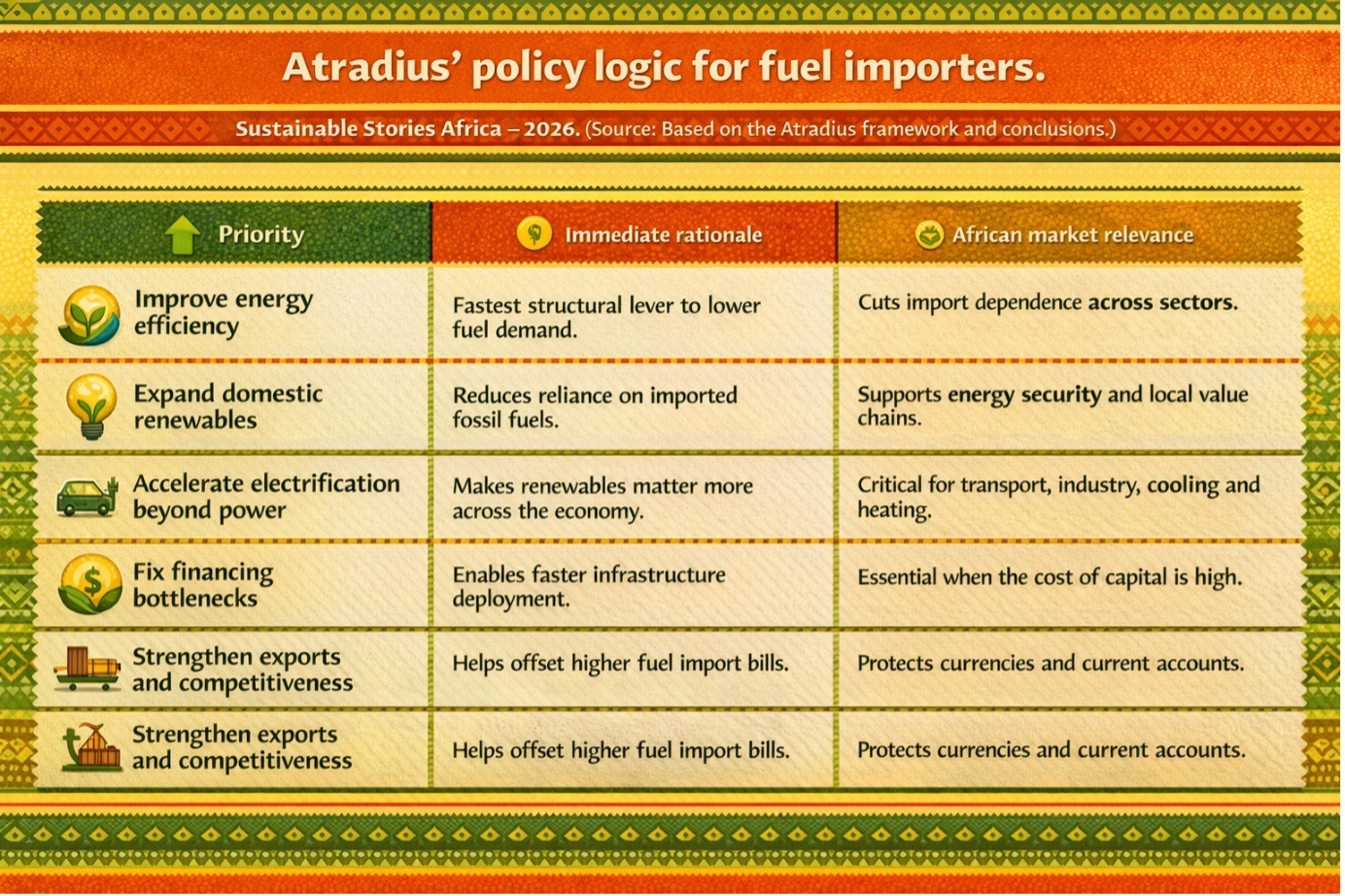

One of the report’s most useful insights is that structural improvement is possible. Atradius finds that while fuel prices drive short-term swings in import bills, energy efficiency has been the strongest structural force reducing net fuel import intensity over time.

That matters because efficiency works across the whole energy system, including sectors such as industry and heavy transport, where electrification remains slow.

By contrast, decarbonisation through renewables has so far had only a modest impact on fuel-import dependence.

Across the broader sample, the renewable share of power rose only from roughly 20% to 30% over the past 15 years.

Atradius argues that renewables alone cannot materially reduce total fossil-fuel demand when electricity still represents a relatively small share of final energy use.

Still, the opportunity is substantial. The report notes that once electrification and renewable generation rise together, their impact becomes mutually reinforcing.

For fuel-importing African economies, that points to a more durable prize: lower exposure to imported fuel shocks, stronger external accounts, better energy security and more room to invest in jobs, industry and social resilience.

What governments and markets must do

Atradius concludes that fuel-importing economies need a broader resilience strategy. That starts with accelerating domestic renewable investment, but it does not end there.

Countries also need faster electrification in

- Industry

- Heating

- Cooling

- Heavy transport

where policy attention remains weaker than in the power sector.

The report is equally clear that macroeconomic resilience cannot be built by the energy system alone. Governments must strengthen export capacity, improve competitiveness and reduce dependence on non-energy imports.

That matters because even where current-account deterioration is not universal, countries already running deficits remain highly exposed.

In Atradius’ model, Tunisia’s current-account deficit widens from 2.1% of GDP in 2025 to 5.1% in 2035, while Morocco’s deteriorates from 1.9% to 5.6%.

Path Forward – Build resilience before prices bite

The report’s message is not that the transition has failed. It is that delay has become expensive.

Fuel-importing economies now need to treat clean energy, efficiency and electrification as macroeconomic protection, not only climate policy.

For African markets, the priority is clear: mobilise cheaper capital, scale domestic renewables, electrify more end uses, and strengthen trade competitiveness before the next fuel shock turns structural weakness into crisis.