The clean-energy transition needs more minerals, more metals and more processing capacity. It also needs more honesty about the emissions generated in that production.

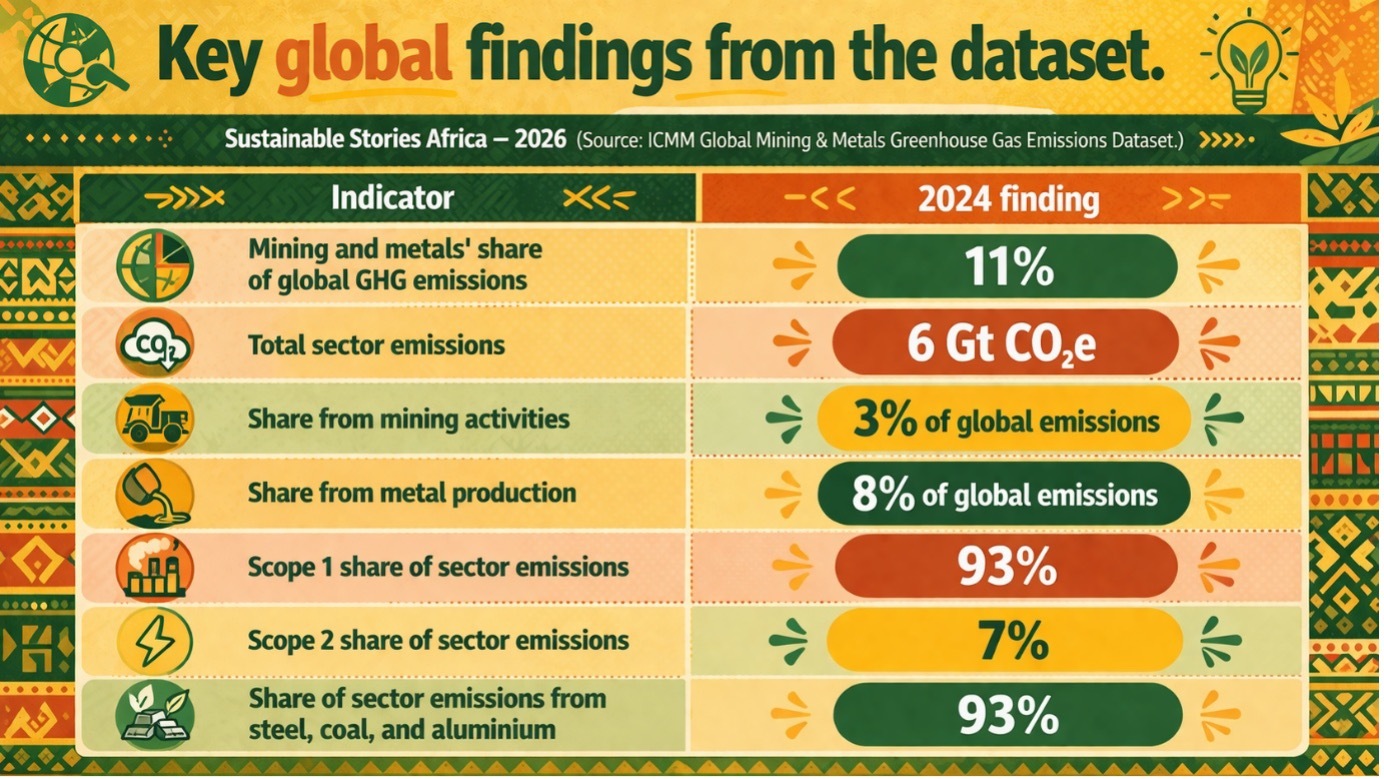

An ICMM dataset puts that trade-off in better perspective, showing mining and metals generated about 11% of global greenhouse gas emissions in 2024.

For African producers, the message is immediate: better data is becoming a competitive tool, not just a reporting exercise.

Transition minerals still carry carbon

The global energy transition rests on a difficult paradox: the mining and metals sector is indispensable to clean-energy systems; however, it remains a major source of greenhouse-gas emissions.

The new Global Mining & Metals Greenhouse Gas Emissions Dataset from the International Council on Mining and Metals puts that contradiction in sharp relief, estimating that the sector accounted for about 11% of global emissions in 2024, or roughly six gigatonnes of CO2e.

Approximately 3% came from primary mining and 8% from metal production, underscoring how deeply the transition still depends on carbon-intensive extraction and processing.

The emissions burden is concentrated on volume-heavy commodities such as steel, coal and aluminium, and reinforced by structural challenges including coal-mine methane, emissions-intensive steelmaking and power-hungry aluminium smelting.

For African and other emerging-market economies, that raises a strategic test. Many are being asked to supply the minerals needed for a low-carbon future while demonstrating that expansion will not entrench a high-carbon industrial pathway.

In that setting, emissions data is no longer peripheral. It is becoming central to market access, investor confidence, policy credibility and industrial competitiveness.

It also shapes capital allocation decisions and strengthens the case for transparent, lower-emission mineral development across resource-rich economies in the South.

The transition’s material paradox

The report highlights a contradiction in the energy transition: the world needs more mined materials for low-carbon infrastructure; however, producing them remains emissions-intensive.

ICMM’s analysis of 1,700 facilities across 14 commodities shows that mining and metals generated approximately 5.9 Gt CO₂e in Scope 1 and 2 emissions, with 93% coming from direct, on-site sources and just 7% from purchased electricity.

The core challenge lies within mines, furnaces and smelters, not only on the grid.

One statistic stands out. Fugitive emissions from coal mining account for 82% of mining Scope 1 and 2 emissions.

Excluding them, mining-only emissions fall sharply as a share of global totals, showing that methane control in coal is one of the fastest targeted decarbonisation levers available.

Interest: Where the emissions really sit

The dataset shows mining and metals emissions are highly concentrated. In 2024, steel accounted for 55% of Scope 1 and 2 emissions, coal mining 23%, and aluminium 15%; together, the three activities generated 93% of the total. The implication is that decarbonisation doesn’t have to begin at once to deliver gains.

Steel remained the largest emitter at 3.3 Gt CO2e because blast-furnace production depends on metallurgical coal. Aluminium contributed 0.9 Gt CO2e, driven by heavy electricity use and carbon anodes in smelting, while coal mining’s profile is dominated by fugitive methane.

The report separates scale from intensity. Steel, thermal coal and aluminium dominate because production volumes are vast, but precious metals are more emissions-intensive per tonne.

Gold emitted 9,948.48 t CO2e per tonne of product, versus 1.78 for steel, 0.18 for thermal coal and 12.46 for aluminium, largely because low ore grades often require more material to be moved and processed.

Mining and metals emissions continued to increase between 2020 and 2024, increasing 3% from 5.76 Gt CO2e to 5.95 Gt CO2e.

The increase was driven largely by higher production and emissions intensity in thermal coal and nickel, even as aluminium output expanded alongside a 3% decline in emissions intensity, supported by greater use of hydropower and renewable electricity.

The regional picture is uneven. Asia accounts for 80% of mining and metals emissions, reflecting its role in mining and processing.

In Europe, steel contributes approximately 93% of emissions, while in Africa and the Middle East, aluminium contributes 40% despite 6% of global production.

Why better data changes decisions

The most useful part of the dataset is not only the headline number. It is the way it can sharpen decision-making. Once emissions are disaggregated by commodity, process and region, the path to abatement becomes more practical.

The report points to medium-term options: shifting steel toward DRI-EAF routes, using CCUS for hard-to-replace blast furnaces, decarbonising electricity for aluminium, testing alternatives to carbon anodes, and cutting coal methane through capture and pre-drainage.

For African producers, this creates a strategic opening. Better emissions visibility can help countries and companies position themselves not simply as mineral suppliers, but as lower-carbon suppliers.

That can matter for future trade relationships, investor scrutiny, industrial policy and value-add ambitions. It can also help governments identify where grid decarbonisation, transport electrification and methane mitigation would create the greatest emissions gains per dollar spent.

This is an inference, but it is strongly supported by the report’s emphasis on transparency, regional asymmetry and enabling ecosystems.

What needs to happen next

The report makes clear that the dataset is a starting point, not a finished picture. Major gaps remain: emissions data are missing for several metals, including gold, silver, molybdenum, cobalt, platinum group metals and lead, for which reliable data are scarce.

Coverage is uneven. Facility-level data captures 92% of coal production, but only 22% of gold, 35% of cobalt and 60% of steel output, with opacity in parts of Asia limiting visibility in a sector that produces more than 70% of the world’s steel.

That means the next phase is about disclosure quality, as it is about decarbonisation technology.

- Governments, mining firms, processors, investors and exchanges need stronger facility-level reporting, more consistent methods and better treatment of informal output, especially in gold.

The report stresses that technology alone will not deliver transition readiness without clean power, finance, infrastructure and long-term coordination, particularly in African markets facing mineral demand and uneven grid reliability.

Path Forward – Measure, then decarbonise

The report advocates a more transparent, facility-level view of emissions, a tighter focus on steel, aluminium and coal methane, and stronger collaboration to expand clean power, electrification and lower-carbon processing routes.

For African markets, the practical priority is to turn emissions data into an industrial advantage: improve disclosure, decarbonise power and logistics, and build credible low-carbon mineral pathways before buyers and financiers begin treating emissions opacity as a market risk.