Nigeria's infrastructure deficit is not a funding gap; it is a structural crisis hiding in plain sight.

With government revenues overwhelmed by debt service and personnel costs, the capital market must now become the primary engine of national development finance.

At Proshare HardFacts Episode 9, held on March 30, 2026, Bolaji Balogun, CEO of Chapel Hill Denham, laid out a frank and data-driven case for why institutional capital, not public spending, must drive Nigeria's infrastructure future, and what it will take to get there.

Nigeria's Infrastructure Deficit Confronts Hard Fiscal Truth

Nigeria is staring at an infrastructure financing gap that no government budget can close. The country's infrastructure base sits at approximately 35% of GDP, barely half the 70% threshold typical of economies with comparable development ambitions, while the annual financing requirement to bridge that gap exceeds $100 billion.

Against a national fiscal architecture where recurrent expenditure and debt service routinely consume the lion's share of public revenues, meaningful government-led capital spending has become structurally impossible.

This is not a new revelation. It is, however, a reality that Nigeria's policy and investment community has yet to convert into action.

The ninth edition of Proshare HardFacts, held on March 30, 2026, offered one of the most candid and rigorous examinations of that challenge. Bolaji Balogun, Chief Executive Officer of Chapel Hill Denham and one of Nigeria's most accomplished deal-makers over the past three decades, sat down with Olufemi Awoyemi, Founder and Chairman of Proshare, for a session titled "Infrastructure, Fiscal Space, and Capital Market Funding."

The conversation was structured around four pillars:

- Nigeria's fiscal reality and infrastructure gap

- Infrastructure debt and capital market solutions

- Subnational infrastructure and regional capital allocation

- The concept of a Capital Market National Deal Room.

Together, they painted a picture of an economy at a decisive inflexion point, and a capital market with the tools; however, it is yet to achieve the scale or coordination to meet the moment.

The 76-Cent Problem No One Wants to Solve

"If you put a hundred dollars through the government, 76 of it will get spent on salaries and debt service."

With that single, clinical observation, Bolaji Balogun reframed Nigeria's infrastructure debate at its most fundamental level. Of the remaining 24 cents available for capital projects, a further fraction is absorbed by land acquisition and administrative costs, leaving a residual so thin as to render government-led infrastructure delivery largely symbolic at the national scale.

The numbers are unambiguous. Nigeria's 2024 budget projected N26 trillion in capital expenditure, a figure that seems substantial until measured against the structural weight of recurrent obligations and the realities of revenue shortfalls.

In practice, the infrastructure investment that reaches the ground is a fraction of what is appropriated, and a fraction of a fraction of what is needed.

This is not a budgeting problem. It is a systemic one. Balogun's argument, anchored in over 35 years of investment banking, deal structuring, and market development, is that solving it requires not more public spending, but a fundamental shift toward infrastructure financing, led by the capital market.

A Market Finding Its Footing

The capital market's infrastructure financing story in Nigeria is still being written — but some chapters are already compelling.

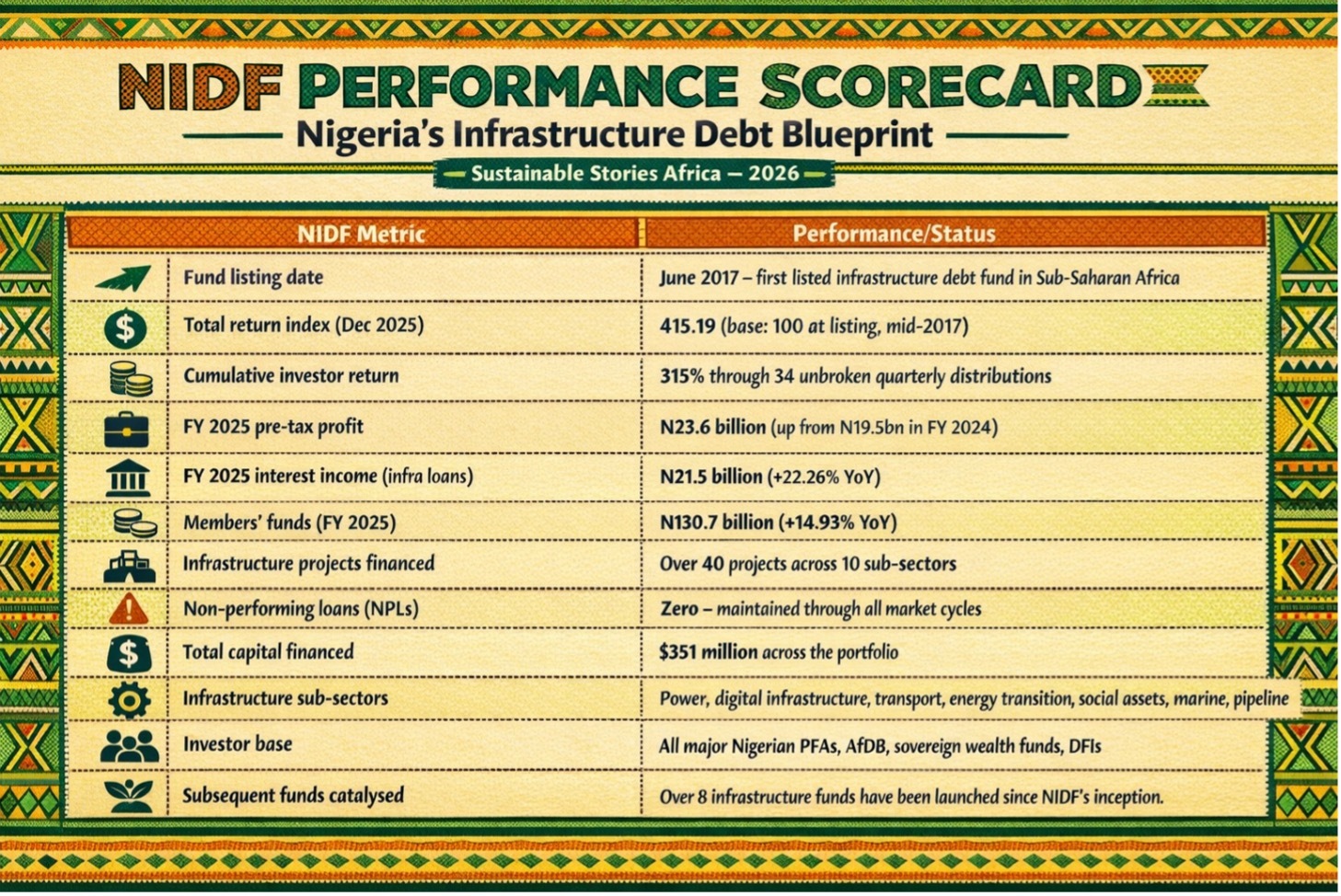

The Nigeria Infrastructure Debt Fund (NIDF), managed by Chapel Hill Denham, has pioneered institutional financing for greenfield infrastructure projects in the country, introducing a model that prior funds had avoided, focusing instead on operational refinancing.

NIDF has attracted participation from all major pension fund administrators, development finance institutions, and sovereign investors, demonstrating that infrastructure debt can function as a core, not marginal, asset class for Nigerian institutional capital.

The fund has financed projects across power, digital infrastructure, transport, energy transition, and social assets.

The Returns Are Already Speaking for Themselves

Nigeria’s most compelling case for capital market-led infrastructure finance is already listed on the Nigerian Exchange.

NIDF’s total return index rose to 415.19 by December 2025, from 343.2 in 2024 and a 2017 base of 100, delivering 315% cumulative returns through 34 unbroken quarterly distributions.

In 2025 alone, the fund posted N23.6 billion pre-tax profit, driven by N21.5 billion in interest income from a loan book that expanded 22.26% year-on-year, with members’ funds at N130.7 billion.

These are the numbers of a structurally sound, development-aligned asset class that has financed over 40 resilient projects, including pipelines, marine assets, off-grid solar, and telecom towers, with zero non-performing loans across multiple shocks.

By catalysing more than eight successor funds, NIDF has created a template that, scaled through a National Deal Room, could simultaneously deepen returns for pension contributors and close Nigeria’s infrastructure gap.

What Must Shift and Who Must Move

Nigeria’s infrastructure-finance case is proven; the challenge now is execution at scale. According to Balogun, the task is to turn a compelling structural argument into coordinated, time-bound action across fiscal, regulatory, and market institutions.

- First, the government must stop crowding out the market it needs. Borrowing trillions of naira to service debt while compressing capital expenditure is unsustainable. A credible medium-term fiscal consolidation plan that steadily reduces debt service as a share of revenue is essential to restore confidence and create space for market-led infrastructure financing.

- Second, PenCom must activate, rather than permit, infrastructure allocation. Pension funds can allocate up to 20% of assets to qualifying instruments; however, actual exposure is below 1%, constrained by a thin pipeline of eligible projects. Turning guidelines into deployment requires proactive collaboration with fund managers, sponsors, DFIs, and the SEC.

- Third, the capital market must build a project pipeline infrastructure, not only securities. A National Deal Room would institutionalise disciplined project origination, preparation, and matching, extending the NIDF model to the system level.

- Fourth, regulation must reward patient capital. Rules on fees, capital requirements, and concentration limits need to reflect the economics of long-duration infrastructure funds, rather than treating them like liquid equity vehicles.

Path Forward – From Blueprint to Market at Scale

Nigeria’s infrastructure gap is structural, but it is not insurmountable. The NIDF model, underpinned by a decade of regulatory work from Chapel Hill Denham, PenCom, the SEC, and NGX, shows that disciplined, market-led infrastructure finance can scale.

The imperative now is to move from proof of concept to national architecture: more funds, more listed instruments, a credible National Deal Room, and fiscal consolidation that stops government crowding out institutional capital.

Nigeria’s N29.43 trillion pension pool is constrained less by appetite than by a shortage of bankable projects, a gap only coordinated action can close.