Global aviation entered 2026 with its net-zero goal intact, but the route to get there is becoming more contested.

Demand is rising, fuel transitions remain expensive, and geopolitics is reshaping the economics of decarbonization.

The central question now is not whether aviation still wants to decarbonise, but whether policy, technology and finance can move fast enough.

That matters for African and emerging markets seeking growth, connectivity and fair participation in the transition.

Growth Meets A Harder Climate Reality

Aviation is trying to do two difficult things at once: grow and decarbonise. The World Economic Forum’s Global Aviation Sustainability Outlook 2026 says the sector maintained its commitment to net-zero carbon emissions in 2025.

However, it did so in a far more complex operating environment shaped by fuel price pressures, policy uncertainty, geopolitical disruption and trade tensions.

The industry’s ambition remains firm. Its delivery model is becoming more pragmatic.

That shift is easy to understand. Global passenger traffic is still climbing sharply.

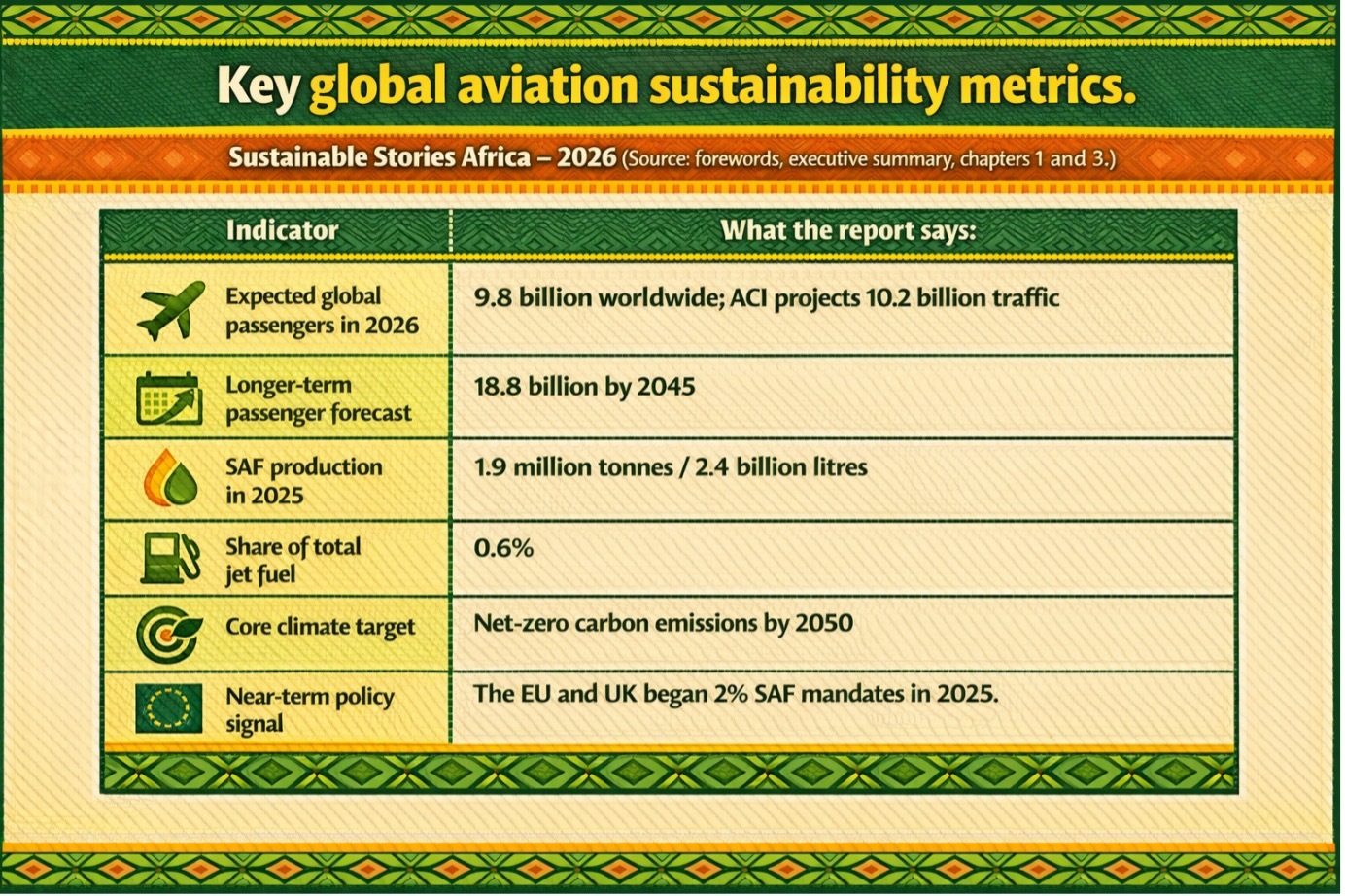

Airports Council International World forecasts 10.2 billion passengers in 2026 and 18.8 billion by 2045.

However, the Forum notes that 9.8 billion passengers are expected worldwide in 2026 and that 2025 was the highest volume of air cargo ever transported.

In other words, aviation demand is not slowing down to make decarbonization easier.

For African and other emerging markets, that creates a double imperative. Aviation remains vital for trade, tourism, investment and mobility.

However, the more the sector grows, the more urgent it becomes to ensure that affordable, cleaner fuels, resilient infrastructure and better access to climate finance and new technology remain at the forefront of this journey.

Net Zero Stays, Pragmatism Rises

The report’s central message is clear: aviation has not walked away from net zero, but it is increasingly rethinking how to get there.

ICAO reaffirmed the sector’s long-term global aspirational goal of net-zero carbon emissions by 2050 at its 42nd Assembly in 2025, and the report says support within industry and governments remains strong.

What is changing is the tone. “Ambitious pragmatism” now defines the mood.

That phrase captures a real tension. Nearly half of senior aviation executives surveyed at the end of 2025 and the start of 2026 said they were optimistic that the sector would make meaningful progress toward decarbonization in 2026.

Although confidence was slightly lower than the year before, the report also notes that approximately one-third expressed apprehension or pessimism, reflecting growing concerns about cost, policy consistency and supply chain resilience.

The biggest near-term pressure point remains sustainable aviation fuel. SAF is still described as the cornerstone of aviation’s decarbonization strategy.

However, it represented only 1.9 million tonnes or 2.4 billion litres of output in 2025, equivalent to just 0.6% of total jet-fuel consumption, even though that was twice the previous year’s level.

Interest: SAF Expands, But Bottlenecks Persist

The report offers a measured view of SAF progress. In 2025, capacity expanded, led by HEFA fuels, while the pipeline for advanced fuels also widened.

The US drove near-term growth, Europe expanded e-fuel activity, and Asia-Pacific posted project gains, including in China.

However, the market remains fragile. Some refineries are producing below capacity, while delays and cancellations have exposed weak margins and high technology risk.

The e-SAF debate has sharpened between reliance on existing biofuels and stronger support for e-fuels.

Policy is moving, but unevenly. In 2025, the EU and UK introduced 2% SAF blending mandates.

The EU plans €2.9 billion by the end of 2027, including €500 million for auctions, while UK data showed SAF reached 2.36% of fuel demand, above target.

Technology trends beyond SAF are reshaping aviation’s transition. Hydrogen is still being tested for ground equipment and energy systems, but aircraft timelines have slipped, making hybrid powertrains the more practical near-term option. eVTOL aircraft may also reach commercial use soon for airport shuttles and short urban routes.

The digital shift is moving faster. AI-driven planning, digital twins, predictive maintenance and emissions analytics are improving efficiency, while contrail-risk tools and standardised labels show data is becoming part of aviation’s climate infrastructure.

A Cleaner System Could Broaden Opportunity

The upside is significant if aviation gets this next phase right. The report frames clean aviation not only as a decarbonisation task, but as a platform for jobs, skills, energy security and industrial growth.

That matters for African economies seeking stronger logistics, tourism expansion and local manufacturing opportunities, because a more inclusive aviation transition could deliver wider economic value, not just lower emissions.

It is a resilience story. By linking decarbonisation with cleaner local fuel production and diversified supply chains, the report suggests that aviation reform can reduce exposure to imported fuel and logistics shocks.

It underscores the value of multilateral alignment through ICAO, since fragmented rules, incompatible SAF systems and carbon-accounting standards would raise costs and deepen inequality for global markets.

Policy Stability Now Matters Most

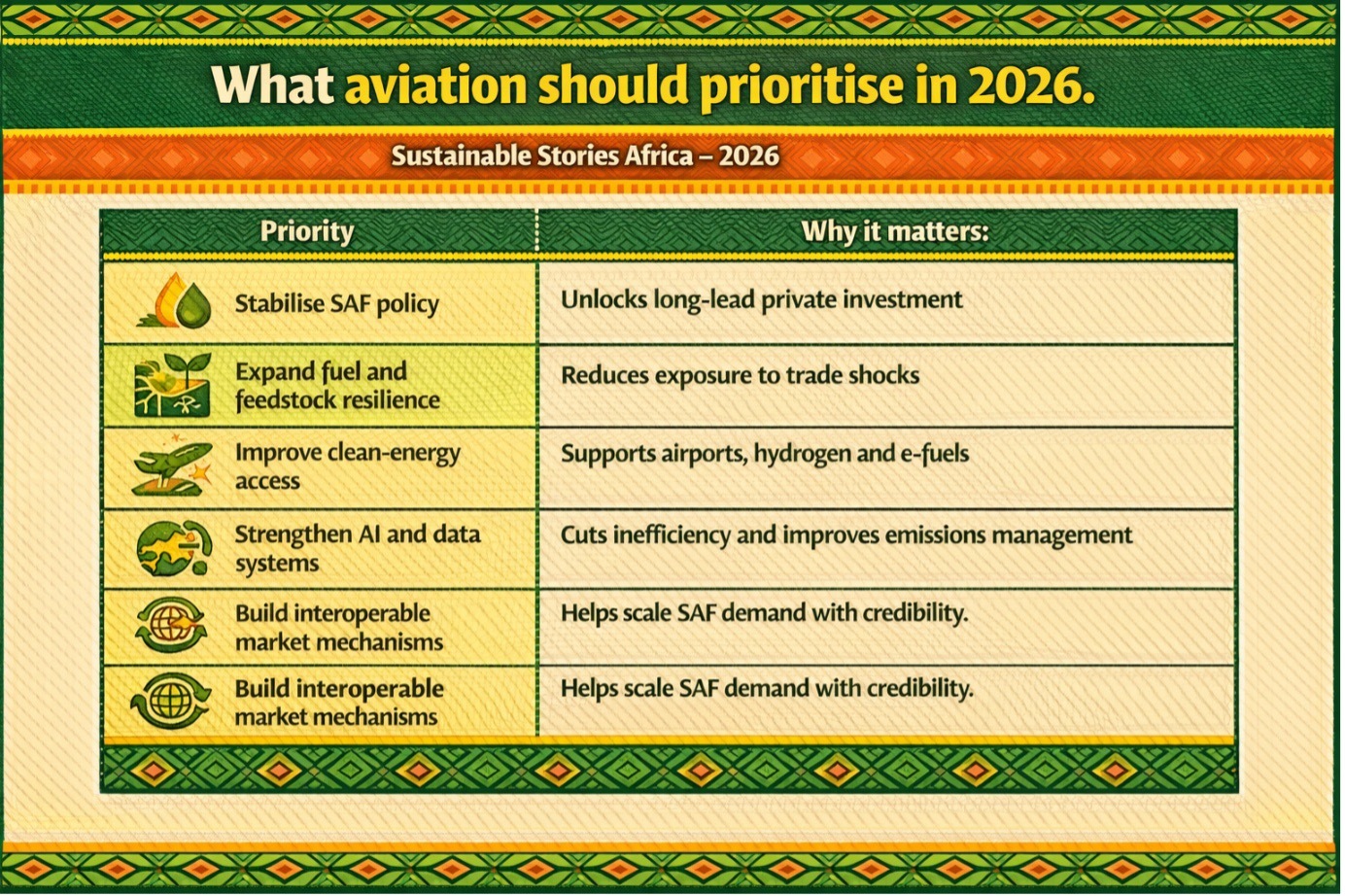

The report’s practical message is straightforward: aviation does not need more slogans; it needs clearer investment conditions.

- Stable policy, aligned SAF standards, stronger fuel and feedstock supply chains, affordable clean electricity and deeper public-private coordination will determine whether the transition can scale.

It also calls for a credible market infrastructure. Book-and-claim systems must become more transparent and interoperable, advanced fuels need stronger but realistic support, and airports must prepare for climate shocks, cyber risks, workforce strain and grid weakness.

The report’s wider signal is clear: while SAF availability, demand and policy are improving, affordability, resilience, and system reliability remain the constraints.

These priorities are drawn from the report’s executive summary, Chapter 1, technology chapters and conclusion.

For African policymakers and carriers, the implication is straightforward: the transition cannot be treated as a rich-market agenda imported later.

If aviation growth is going to continue, then planning for SAF access, airport resilience, digital efficiency and regional policy coherence needs to start now.

Path Forward – Keep Ambition, Fix Delivery

Global aviation is not retreating from net zero. It is entering a harder phase in which credibility will depend less on ambition and more on whether fuel, finance, policy and infrastructure can move together.

The priority for 2026 is pragmatic acceleration: scale SAF, stabilise rules, strengthen resilience, and make sure emerging markets are part of the solution.

That is how aviation can keep growing without losing sight of climate responsibility.