Assurance is moving from a sustainability slogan to a reporting discipline. The IAASB’s November 2025 supplemental guidance to ISSA 5000 provides practitioners with eight model reports showing how sustainability assurance should be written across clean, combined and modified conclusions.

For African markets, the signal is practical and urgent: as IFRS sustainability reporting spreads, the quality of assurance language, scope, limitations and independence disclosures will increasingly shape trust, comparability and access to capital.

Assurance language is becoming market infrastructure

The new ISSA 5000 Supplemental Guidance does not create another ESG acronym. It does something more consequential: it shows, in report form, how sustainability assurance should be communicated when disclosures are clean, partial, combined, qualified, disclaimed or adverse.

Issued by IAASB staff in November 2025, the document is non-authoritative; however, it is designed to supplement Appendix 3 of ISSA 5000 with eight illustrative reports.

That matters because sustainability reporting is no longer just about what companies say. It is increasingly about what practitioners can stand behind, how clearly they describe uncertainty, and whether users can understand the level of assurance actually obtained.

The guidance repeatedly stresses that reports must be tailored to the circumstances, rather than reduced to boilerplate.

For African and other emerging markets, where disclosure systems, data quality and assurance capacity are still developing unevenly, that distinction is critical.

Credible assurance can strengthen confidence in climate, governance and broader sustainability reporting; weak assurance language can do the opposite.

Assurance Reporting Is Becoming More Exact

The headline message in the guidance is simple: sustainability assurance is becoming more granular, more transparent and less forgiving of vague language.

IAASB staff say the supplement provides eight illustrative sustainability assurance reports, covering both unmodified and modified outcomes, and pairs each with a fact pattern plus explanatory notes on the technical basis for the wording used.

That architecture matters. The publication moves beyond generic reassurance and shows how practitioners should report across limited assurance, reasonable assurance, combined engagements, selected disclosures, comparative information, inherent limitations and legally required reporting responsibilities.

It also shows what changes when conclusions are modified, including qualified, disclaimer and adverse outcomes.

Sustainability Assurance Now Demands Clearer Reporting

The guidance is best read as a map of what sustainability assurance explains. For African reporters and assurance providers, one key point is that IFRS Sustainability Disclosure Standards are treated as fair presentation criteria.

That means practitioners must assess overall presentation, structure and content, not just technical compliance.

The document also recognises that forward-looking transition plans and Scope 3 emissions estimates carry significant uncertainty and may require explicit language to address inherent limitations.

It further stresses that comparative information and other information in annual reports cannot be treated casually or assumed away.

One practical illustration is the limited assurance example built around IFRS sustainability disclosures and SASB metrics.

It includes comparative information, a going-concern emphasis-of-matter paragraph, caution highlighting forward-looking transition-plan information, and a warning that Scope 3 estimation methods can affect comparability across time and entities.

The guidance is also clear about what happens when assurance breaks down.

In the disclaimer of conclusion, it emphasises that “Other Information” and “Summary of Work Performed” sections should be omitted so they do not dilute the significance of insufficient evidence.

Clearer Assurance Can Strengthen ESG Trust

If adopted seriously, this guidance could help solve one of the biggest ESG credibility problems in African markets: the gap between expanding disclosure ambition and uneven assurance quality.

- For companies, the benefit is clearer expectations.

- For practitioners, it is a more usable template for explaining scope, limitations, evidence and responsibility.

- For regulators and exchanges, it offers a common language that can support more consistent supervisory expectations.

- For investors and lenders, it improves the odds that sustainability reports will become more decision-useful rather than more decorative.

That is especially important in markets where companies may report under overlapping local rules, emerging stock-exchange requirements and global frameworks at the same time.

Illustration D, which combines national sustainability standards with IFRS Sustainability Disclosure Standards, is therefore more than a technical footnote.

It points to a future in which cross-framework reporting will be the norm, rather than the exception.

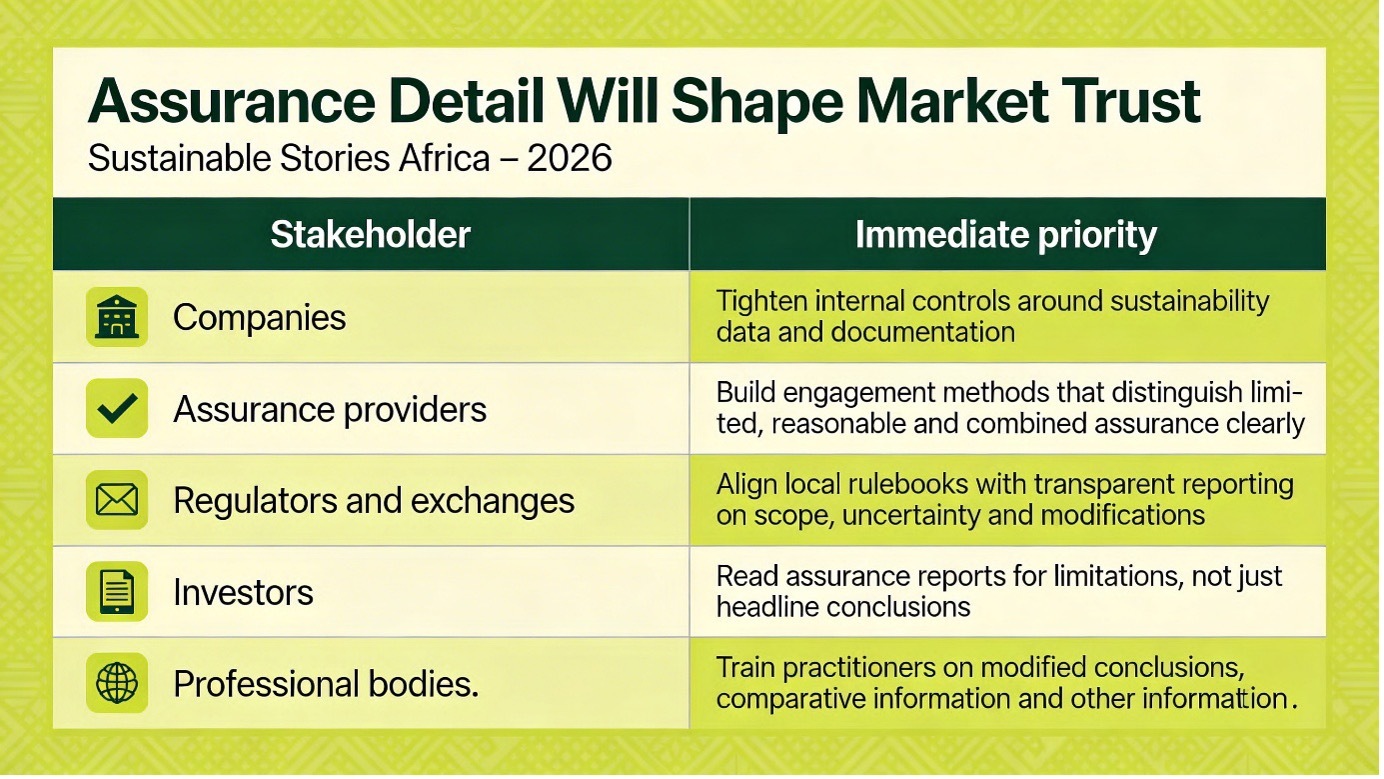

Assurance Detail Will Shape Market Trust

The next move is not to treat ISSA 5000 supplemental guidance as reading material for specialists alone.

Boards, audit committees, regulators, stock exchanges and reporting teams need to translate it into implementation.

The broader lesson is that corporate integrity in sustainability reporting will increasingly be tested in the detail of the assurance report itself: what was covered, what was not, what remains uncertain, and whether the practitioner could genuinely obtain enough evidence.

In that sense, ISSA 5000’s supplement is not just guidance on wording. It is guidance on market trust.

Path Forward – African ESG Assurance Needs Credible Execution

African markets do not need more ESG theatre. They need assurance reports that explain scope, evidence, uncertainty and responsibility with precision.

ISSA 5000’s supplemental guidance offers a workable template for that shift.

The priority now is execution: stronger data systems, better-trained practitioners, clearer regulatory alignment and more disciplined reading of assurance conclusions.

That is how sustainability reporting begins to earn, rather than assume, credibility.