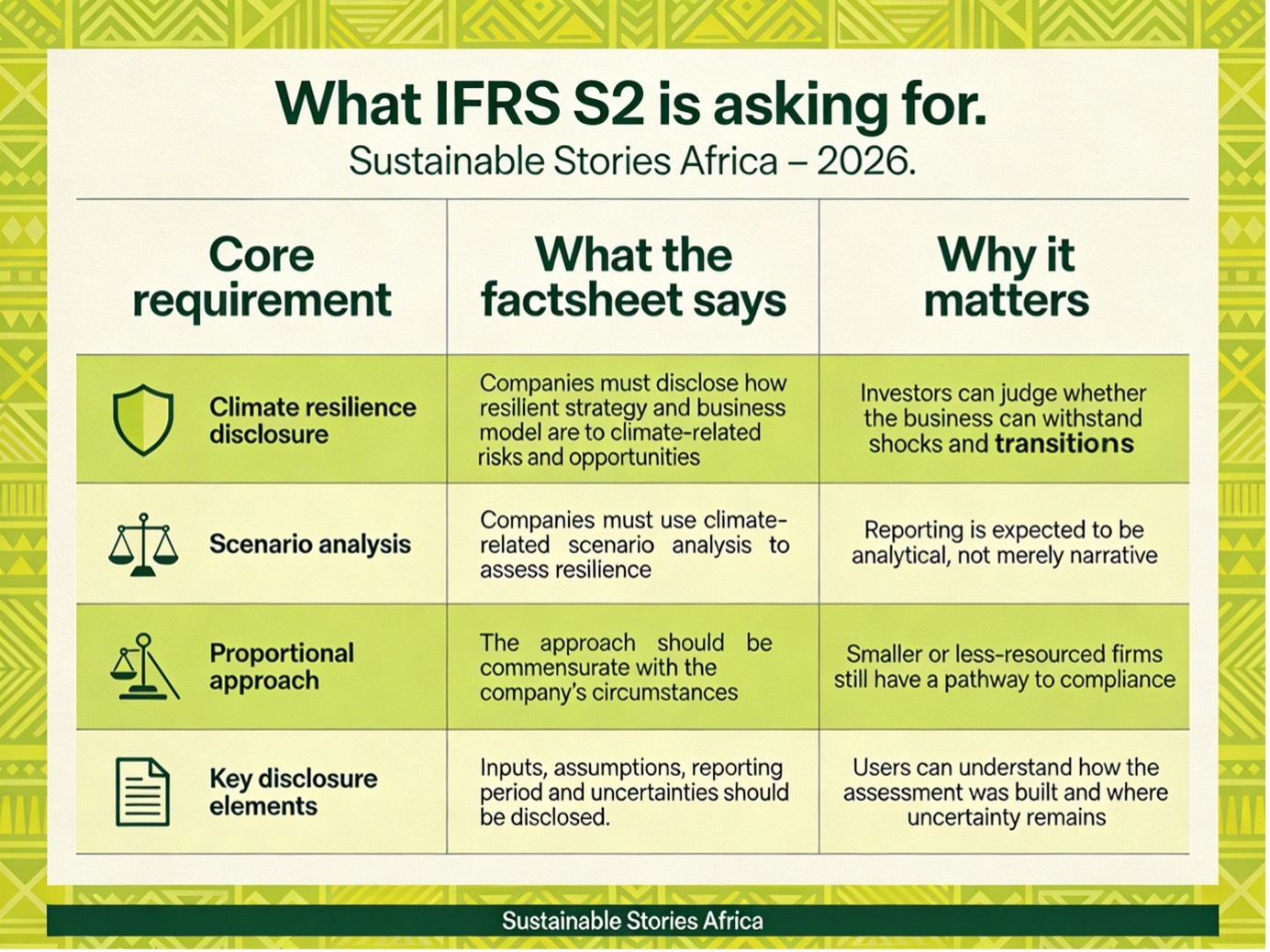

Climate resilience is no longer a peripheral ESG talking point. In its March 2026 factsheet, the IFRS Foundation makes clear that IFRS S2 requires companies to disclose how resilient their strategy and business model are to climate-related risks and opportunities, and to use climate-related scenario analysis to inform that assessment.

For African and other emerging markets, the question is whether climate risks matter.

It is also whether companies, regulators and investors can translate those risks into decision-useful disclosures without turning reporting into a box-ticking exercise.

Climate resilience becomes a reporting test

IFRS S2 is drawing a clearer line between climate ambition and climate accountability.

The March 2026 fact sheet from the IFRS Foundation says companies must disclose information that enables investors to understand the resilience of strategy and business model to climate-related changes, developments and uncertainties.

It also requires climate-related scenario analysis, using an approach commensurate with the company’s circumstances.

That matters because climate-related risks and opportunities are not static. They are often complex, and their likelihood, magnitude and timing are uncertain.

The fact sheet frames climate resilience as a company’s capacity, strategically and operationally, to manage climate-related risks, opportunities, and adapt to both transition and physical climate risks.

For African markets, this comes at a time when disclosure expectations are rising; however, corporate capabilities remain uneven.

The shift is significant: investors are being told to expect more than broad climate statements. They are being given a framework for asking how resilient a business really is.

Climate Stress Tests the Business Model

A company may talk confidently about sustainability, but IFRS S2 asks a harder question: what happens to the business model under climate stress?

That is the central signal from the fact sheet. IFRS S2 requires companies to disclose information that helps investors understand the implications of climate risks and opportunities for strategy and business model, the significant uncertainties considered, and the company’s capacity to adjust or adapt over the short, medium and long term.

It also requires companies to explain how and when scenario analysis was carried out, including the inputs used, key assumptions made and the reporting period covered.

This is important because it shifts climate disclosure away from generic commitment language and towards structured evidence.

It tells markets that resilience is not a slogan. It is an assessed condition, backed by analysis, assumptions and governance choices.

Climate Scenario Analysis Requires Proportionate Maturity

The fact sheet is especially useful because it explains not only what companies must disclose, but also how they are expected to approach the task.

It defines scenario analysis as a process for identifying and assessing a range of possible future outcomes in times of uncertainty.

In practical terms, this helps a company examine how climate-related risks and opportunities could affect its strategy and business model over time, and whether it can adapt.

The fact sheet sets out a three-step process.

- First, a company assesses its own circumstances, including its exposure to climate-related risks and opportunities, as well as the skills, capabilities and resources available.

- Second, it chooses an approach suited to those circumstances, including the scenarios, inputs and variables it will use, and whether the method should be more qualitative or quantitative.

- Third, it interprets the results, assesses climate resilience, and discloses that assessment in line with IFRS S2.

That emphasis on proportionality is especially important for African and Global South companies, because it allows a credible approach without assuming complex modelling from the start.

The fact sheet makes two important temporal points. Companies assess climate resilience annually, but they do not need to rerun full scenario analysis every year.

At a minimum, the analysis should be updated in line with the strategic planning cycle, with circumstances reassessed each time.

That is a practical message for African companies. A bank, manufacturer, telecom or energy firm may begin with a simpler qualitative approach, but rising exposure, stronger investor scrutiny or improved internal capacity should push the analysis to mature.

Climate Resilience Disclosure Can Strengthen Markets

Handled well, this requirement could improve much more than annual reports.

- For investors, it could produce better visibility into whether companies are prepared for heat stress, flooding, energy transition risks, carbon pricing, supply-chain instability or policy change.

- For boards, it could sharpen strategic thinking by forcing climate assumptions into capital allocation, operations and long-term planning. For regulators and exchanges, it could improve comparability across issuers.

- For citizens and communities, it could mean more honest conversations about business continuity, resilience investment and where adaptation gaps remain.

For African markets in particular, the upside is strategic. Many economies face high physical climate exposure while also needing industrial growth, infrastructure finance and deeper capital markets.

Better climate-resilience disclosure can help separate companies that merely acknowledge climate risk from those that are actually planning for it. That distinction matters for trust, cost of capital and long-term competitiveness.

Implementing Climate Resilience Requires Stronger Governance

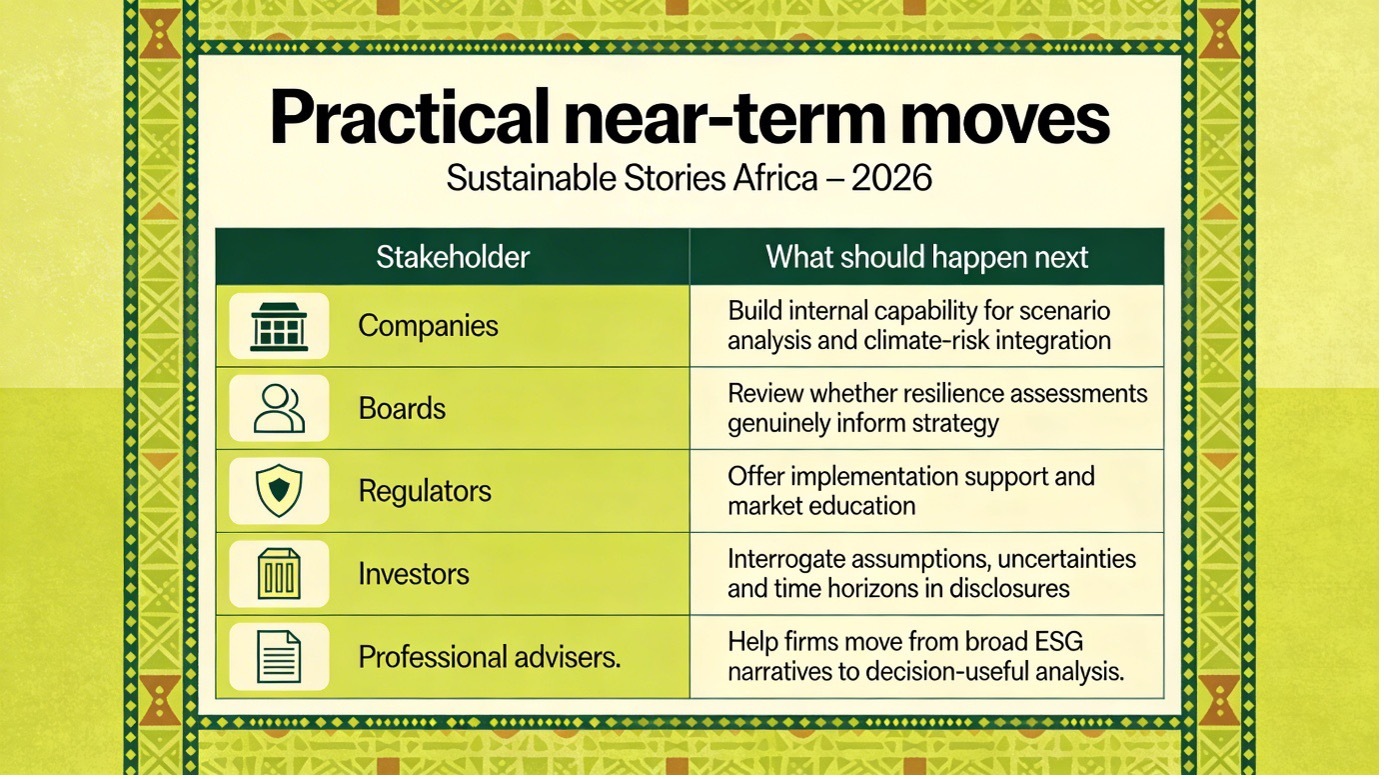

The immediate task is implementation.

- Companies need to map climate-related risks and opportunities more systematically, identify which parts of the business model are most exposed, and align scenario analysis with strategic planning cycles.

- Finance teams, sustainability teams and risk functions will need to work together more closely.

- Boards and audit committees will need to ask sharper questions about assumptions, data quality and material uncertainty.

- Regulators, standard-setters and market institutions in African economies also have work to do. They need to support capacity building so that proportionality does not become a loophole for weak disclosure.

- Investors should press for clarity on assumptions, time horizons and adaptive capacity, rather than rewarding polished language alone.

The broader message from the factsheet is not that every company must become a climate-modelling specialist. It is that companies must now show, in a structured way, how they think about resilience in the light of uncertainty. That is a higher reporting bar, but also a more useful one.

Path Forward – African Markets Need Credible Climate Disclosure

IFRS S2 is pushing climate disclosure towards strategy, evidence and adaptation capacity. The priority now is to help companies, especially in emerging markets, build proportionate but credible scenario-analysis practices that support better decision-making.

For African markets, the opportunity is clear: stronger climate resilience disclosures can improve comparability, investor confidence and long-term planning. The challenge is execution, and the next phase will depend on capability, consistency and follow-through.