Africa’s oil and gas sector is under growing pressure to do two hard things at once: support energy access and economic development while meeting tougher expectations on sustainability, governance and resilience.

The deeper question is whether sustainability matters.

The question is whether African operators can move from compliance language to operational change fast enough to protect capital, communities and long-term relevance.

From field realities to boardroom choices

Sustainability in African oil and gas is no longer a boardroom slogan or a reporting appendix.

It is becoming an operating condition. As policy shifts, and investor scrutiny and climate risk tighten around the sector, African producers are being pushed to prove that resource development can still create value without ignoring environmental stress, social tensions and governance failures.

In Sustainability in the African Oil & Gas Sector: From the Boiler Room to the Boardroom, author Chika Onyekwere frames the challenge as one of translation: taking field-level operational realities and turning them into strategy, data-backed decisions and long-term sustainability planning.

That framing matters because many of the sector’s biggest problems do not begin in disclosure templates. They begin in water systems, community relations, methane leaks, waste practices and weak governance.

For African markets, the stakes are unusually high. Oil and gas still underpin jobs, fiscal revenues and foreign exchange in many economies, even as climate shocks, energy poverty and shifting capital markets reshape what investors and citizens now expect. Sustainability, in that sense, is no longer peripheral to sector survival. It is central to it.

Africa’s oil and gas sector sits in a double bind

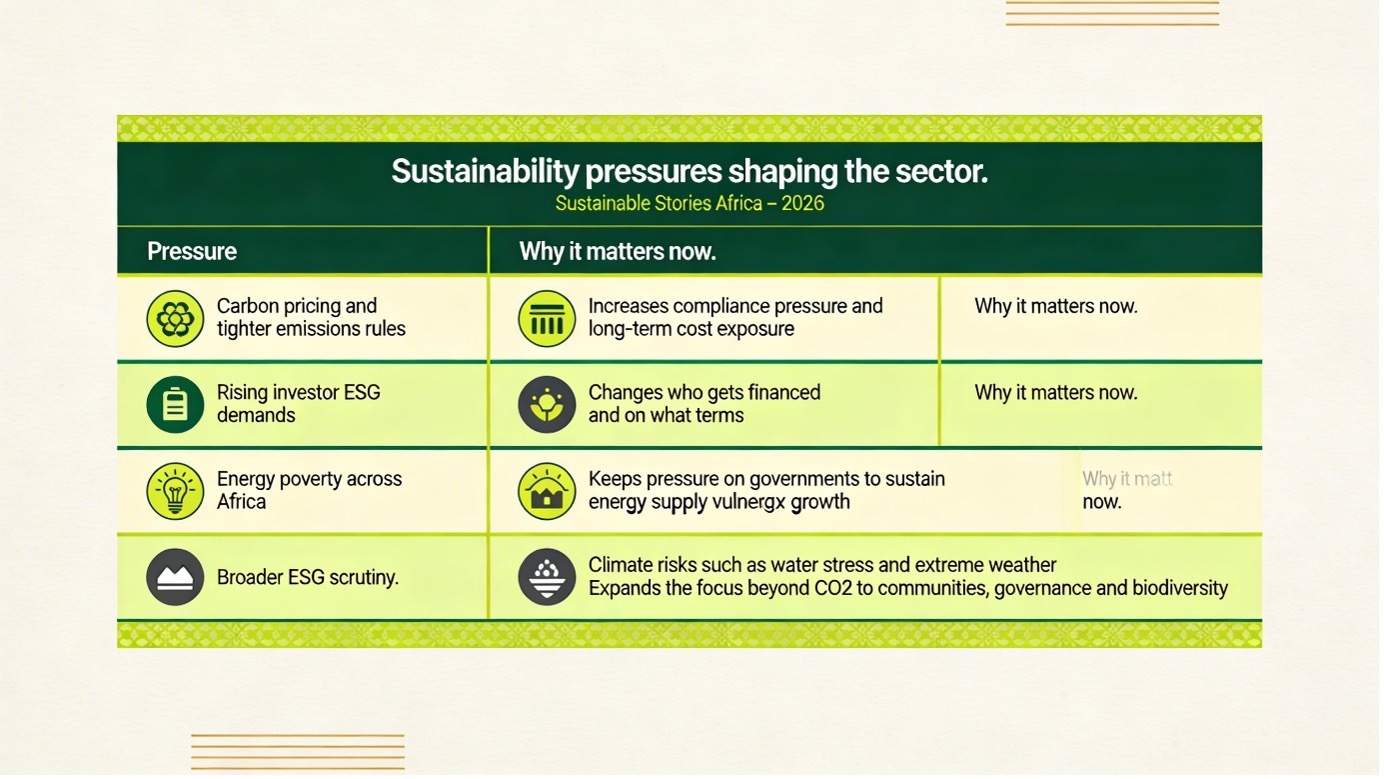

The sector’s central tension is stark. Global energy demand is rising, but the policy environment around hydrocarbons is becoming more restrictive.

On page 3, the presentation highlights three forces now shaping the global context:

- Increased carbon pricing mechanisms

- Stricter emissions regulations

- Growing investor demand for ESG compliance.

Africa’s reality is different from that of richer, already-industrialised markets. On page 4, the deck describes a “dual challenge”: meeting urgent energy needs for economic growth while adopting more sustainable practices.

It identifies three realities that make the transition more complex:

- Energy poverty

- Economic dependence on oil and gas revenues and jobs

- Emerging climate risks such as water scarcity, extreme weather and ecosystem degradation.

That contrast is what makes the sustainability debate in Africa harder than many global narratives suggest.

The continent cannot simply switch off hydrocarbons without deep economic consequences. However, it cannot assume that the old model of extraction, weak oversight and delayed accountability will remain financeable.

The presentation’s strongest insight is that sustainability now needs to be read from “the boiler room to the boardroom.” In practical terms, that means operational discipline and strategic credibility have become inseparable.

What the trends are signalling now

The production story is mixed. According to the chart on page 5, African oil production has declined slightly over the period shown, while gas production has continued to rise.

The deck presents this as evidence that gas is becoming a more important transition fuel for the continent, offering producers a more defensible bridge between current hydrocarbon dependence and lower-emissions expectations.

However, page 6 argues that sustainability in African oil and gas must go beyond carbon alone. It highlights three pillars of holistic sustainability: environmental stewardship, social responsibility and good governance.

That matters because, in many African extractive markets, the biggest risks also include polluted water, weak community trust, poor benefit-sharing, corruption and fragile enforcement.

The capital picture is shifting too. On page 7, the chart shows stronger allocation toward renewable integration, methane abatement, carbon capture and community development, warning that operators who ignore this trend risk losing access to crucial funding.

What stronger sustainability performance could unlock

The presentation is not only a warning. It also sets out a positive commercial case for early action.

Companies that move sooner can become more resilient, more investable and more credible with regulators and communities.

Better methane control, cleaner technology, stronger environmental management, improved community engagement and better governance can reduce waste, lower conflict risk, and strengthen access to capital.

That matters in African markets, where projects often fail not because the geology is weak, but because the surrounding systems are fragile.

Sustainability, treated seriously, becomes part of project durability. The framing on page 2 is especially useful: the sector now needs a bridge between operational insight, executive vision and data-driven decision-making.

What African operators and policymakers should do next

The path set out in the deck is direct. On page 9, it identifies three strategic imperatives:

- Integrate ESG into core business strategy

- Innovate and diversify into cleaner technologies

- Strengthen partnerships with governments, communities and NGOs.

These points deserve to be made more concrete.

- First, companies need to move sustainability out of the reporting silo and into investment decisions, procurement, operations and executive accountability.

- Second, methane abatement, water stewardship and waste reduction should become operational priorities, not secondary talking points.

- Third, boards should treat community relations and governance as hard risk issues, not soft social ones.

- Fourth, governments and regulators need to make the rules more predictable and enforce them more consistently.

- Fifth, financiers should continue rewarding projects that show credible transition planning rather than broad ESG branding.

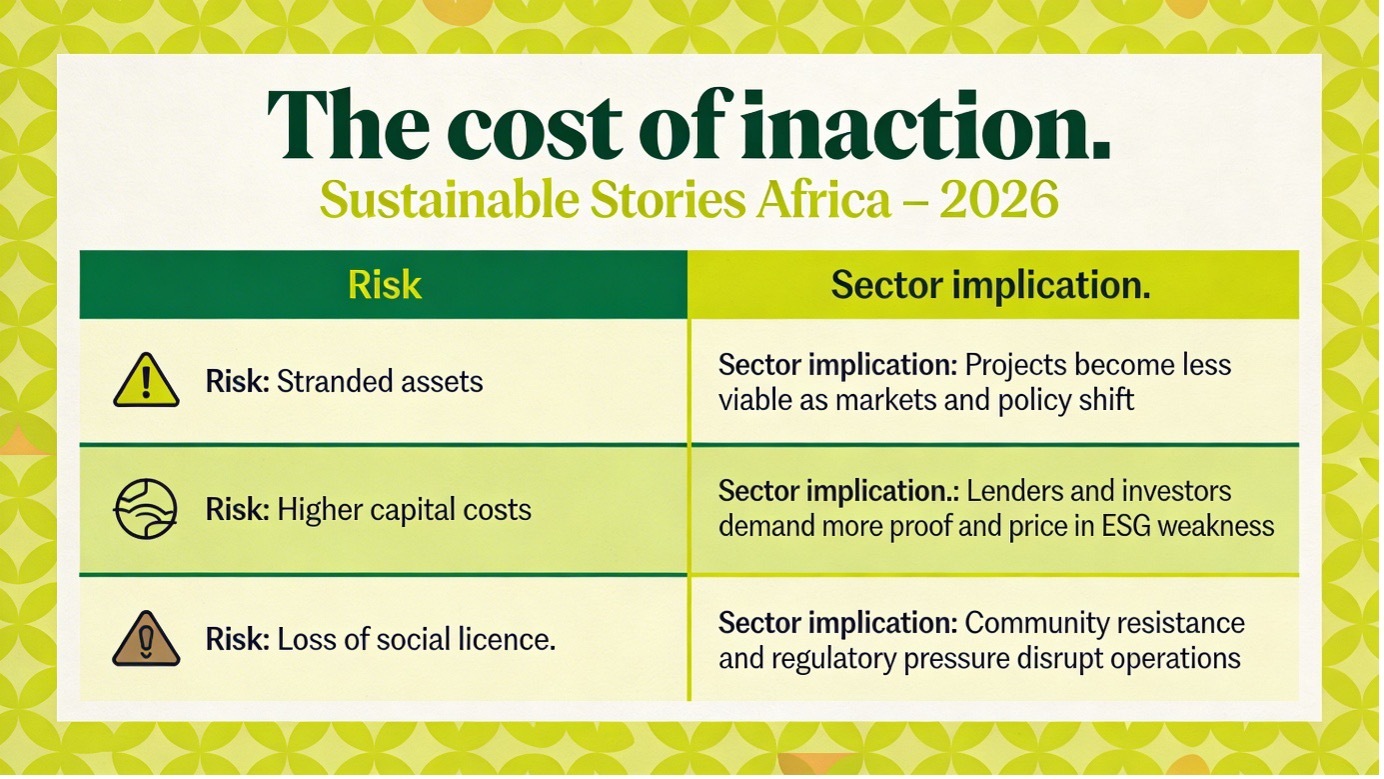

The cost of failing to do this is made explicit on page 8. The presentation lists three major risks of inaction:

- Stranded assets

- Increased capital costs

- Loss of social licence.

These are not abstract threats. They go directly to asset value, borrowing conditions and project continuity.

Path Forward – Make sustainability operational

African oil and gas do not need less realism. It needs more of it.

The sector’s future depends on recognising that sustainability is now part of operational fitness, financial credibility and long-term competitiveness.

The practical agenda is clear: embed ESG in strategy, invest in cleaner systems, strengthen governance and build trust with communities.

In Africa’s extractive economy, that is no longer optional. It is the new threshold for resilience.