Based on Bismarck Rewane’s April 1, 2026, LBS Breakfast Session presentation, the message was blunt: Nigeria may be partly insulated from global conflict, but its households, traders and manufacturers remain dangerously exposed to imported inflation and domestic fragility.

The central question is no longer whether energy shocks matter, but who absorbs the pain first, and how quickly policymakers can stop a temporary external shock from becoming a wider economic and social setback.

When Higher Oil Prices Fail Households

Nigeria entered April with a complicated mix of resilience and risk. In the presentation, Rewane framed the moment as an “inflation surge” that is “externally induced” but “internally magnified”, a warning that global oil and geopolitical disruptions can still hit a country hard when domestic transport, logistics, power, pricing and policy transmission remain weak.

He organised the argument around a six-dimensional stakeholder analysis and three time horizons: a 45-day shock, a 90-day shock and an indefinite scenario.

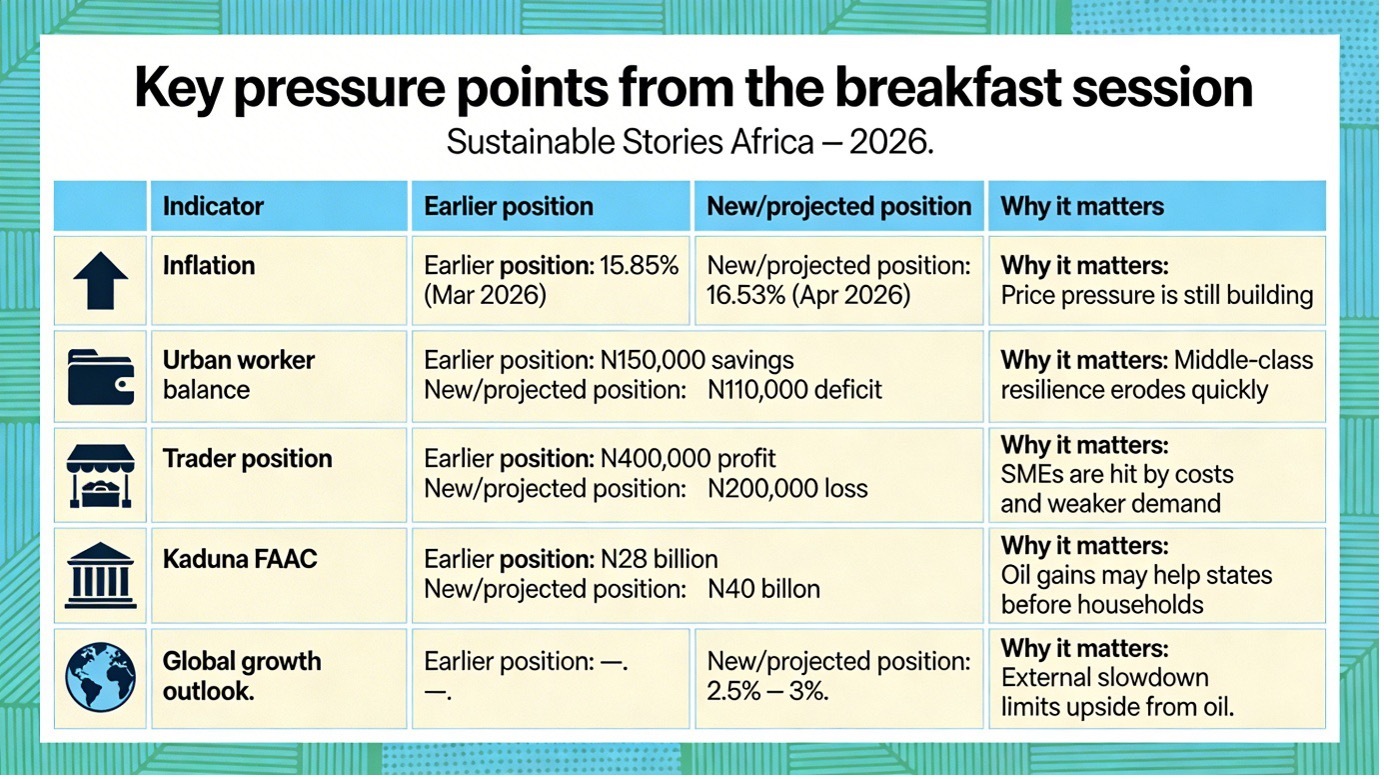

The numbers show why the argument matters now. The deck’s macroeconomic snapshot puts projected Q1 2026 GDP growth at 3.2%, inflation at 15.85% in March and 16.53% in April, while the official exchange rate sits in a band of approximately between N1,380 to N1,430/$ in April and N1,350 to N1,410/$ in May.

At the same time, stock market capitalisation rose from N129.45 trillion in March to N135.50 trillion in May, underscoring how financial indicators can improve even while real economy pressures intensify.

The shock is global, but the squeeze is local

Rewane’s core thesis is that an energy shock now travels fast: energy prices rise, inflation rises, demand falls, and recession risk rises.

Where Brent had traded above $110 per barrel, global growth is expected to slow to 2.5 – 3% as tighter monetary conditions compound the pressure.

But the most striking part of the presentation is not the headline oil price. It is the way the deck translates that shock into lived Nigerian realities. Rewane’s six stakeholders were not abstract categories. They were a Lagos salary earner, a trader, a Kaduna State, an oil militant in the creek economy, a manufacturer and an artist. That framing moved the conversation away from averages and into distribution: who loses first, who gains temporarily, and who remains fragile even when crude prices rise.

The metrics tell a sharper story

The urban worker example is especially revealing. A Lagos professional earning N900,000 monthly had expenses of N750,000 in January and savings of N150,000. By April, the same person’s monthly cost profile had risen to N1.01 million, pushing them into a N110,000 deficit.

Petrol costs were shown to be doubling, food rising 30% – 40%, and rent up 40%. The presentation’s conclusion was simple: the middle class gets squeezed into fragility, and consumption weakens.

The trader's story is just as stark. A business previously generating N2 million in monthly revenue and N400,000 in profit is shown moving into an approximate N200,000 loss as logistics rise 80% – 100%, supplier prices increase 25% – 40%, and customer demand falls 20% – 30%. That is a familiar Nigerian problem: costs rise faster than purchasing power.

The deck widens the lens further. It warns that households could face a 15% – 20% drop in real purchasing power, with food and commodity prices rising 15% – 30% as transport costs surge.

It adds that low-income families already spending 40% – 60% of their income on basics would likely cut staples and healthcare, deepening multidimensional poverty.

One exception in the six-stakeholder model is government finance. Using Kaduna State as a case study, the presentation shows that monthly FAAC receipts increase from N28 billion to N40 billion, reducing the fiscal deficit from N28 billion to N16 billion.

However, the warning is clear: higher revenue alone does not guarantee better outcomes. Efficiency, capital allocation and discipline determine whether windfall funds are used to improve infrastructure or to enlarge recurrent and political spending.

These figures are drawn directly from the uploaded presentation.

Where resilience is still visible

The presentation is not wholly pessimistic. It argues that some parts of the “new economy” remain more adaptable than older cost-heavy sectors.

On the artist side, the deck shows a deeper shift toward digital distribution. For film, production costs for a blockbuster are shown doubling from N250 million to N500 million, while cinema attendance falls from 450,000 to 200,000, and box office sales drop from N2.1 billion to N1 billion.

However, music metrics move differently: YouTube subscribers rise from 4.95 million to 8 million, while Spotify monthly listeners increase from 9.2 million to 15 million. That points to a broader economic lesson: digital channels can soften shocks when physical consumption weakens.

There is also a policy window. A slide on naira settlement accounts argues that routing diaspora inflows through regulated naira accounts could improve FX transparency, strengthen formal liquidity, narrow the spread between official and parallel rates, and gradually reduce imported inflation, although not immediately.

What policymakers and businesses should do next

The practical message from the breakfast session is that Nigeria should not confuse higher oil prices with broad-based relief.

Rewane’s scenario work suggests that without better logistics, stronger production security, tighter inflation management and more disciplined fiscal choices, oil windfalls will bypass households and leak away through higher costs, lower demand and insecurity.

That point is reinforced by the oil output slide, which shows production falling to 1.31 mbpd in February from 1.46 mbpd in January before only a modest recovery, limiting Nigeria’s ability to benefit from higher prices.

For businesses, the call is to protect cash flow, trim avoidable input exposure, and move faster on distribution efficiency and digital channels.

For state governments, the test is whether extra FAAC becomes productive capital or political consumption.

For federal policymakers, the real task is to stop an imported price shock from becoming a domestic confidence shock.

Path Forward – What Comes Next After Shock

Nigeria’s best response is not denial, but faster adjustment: protect purchasing power, improve FX transmission, secure oil infrastructure, and direct windfall revenues into productivity-enhancing spending rather than short-term comfort.

The breakfast session’s strongest insight is that resilience now depends less on headline oil prices than on policy quality.

External shocks may start abroad, but whether they become prolonged domestic pain is still a local decision.