Nigeria’s banking sector is being pushed to treat sustainability reporting less as branding and more as an operating discipline. The Central Bank of Nigeria’s Sustainable Banking Principles now sit at the centre of that shift.

The real question is no longer whether banks should disclose, but whether they can do so credibly, consistently and on time, with evidence that stands up to regulators, investors and communities alike.

Rules Tighten, Credibility Gets Pricier

Nigeria’s financial sector is entering a more demanding phase of ESG accountability. The Central Bank of Nigeria’s Sustainable Banking Principles, first launched in 2012 and revised in 2023, provide a regulatory framework for banks, merchant banks, non-interest banks, discount houses and development finance institutions to integrate environmental, social and governance factors into operations and credit decisions.

The guide’s core message is blunt: reporting is no longer a side exercise. It is part of how institutions prove resilience, discipline and credibility.

That matters now because the reporting burden has become more specific. The scope summary in the guide makes clear that institutions are expected to disclose annual sustainability reports, environmental and social risk policies, portfolio exposure by risk tier, and operational footprint data, including energy, water, Scope 1 and 2 emissions, and waste.

For December year-end institutions, the guide says submission is due within three months of year-end, effectively by 31 March.

For Nigerian banks, this is not just a governance story. It is a capital-markets story, a risk story and, increasingly, a development story.

The guide says sustainability reporting under the SBPs is “not merely a compliance exercise” because it helps build credibility with international lenders and ESG-focused investors, while also demonstrating accountability to host communities and satisfying supervisory expectations.

Compliance Has Entered the Core

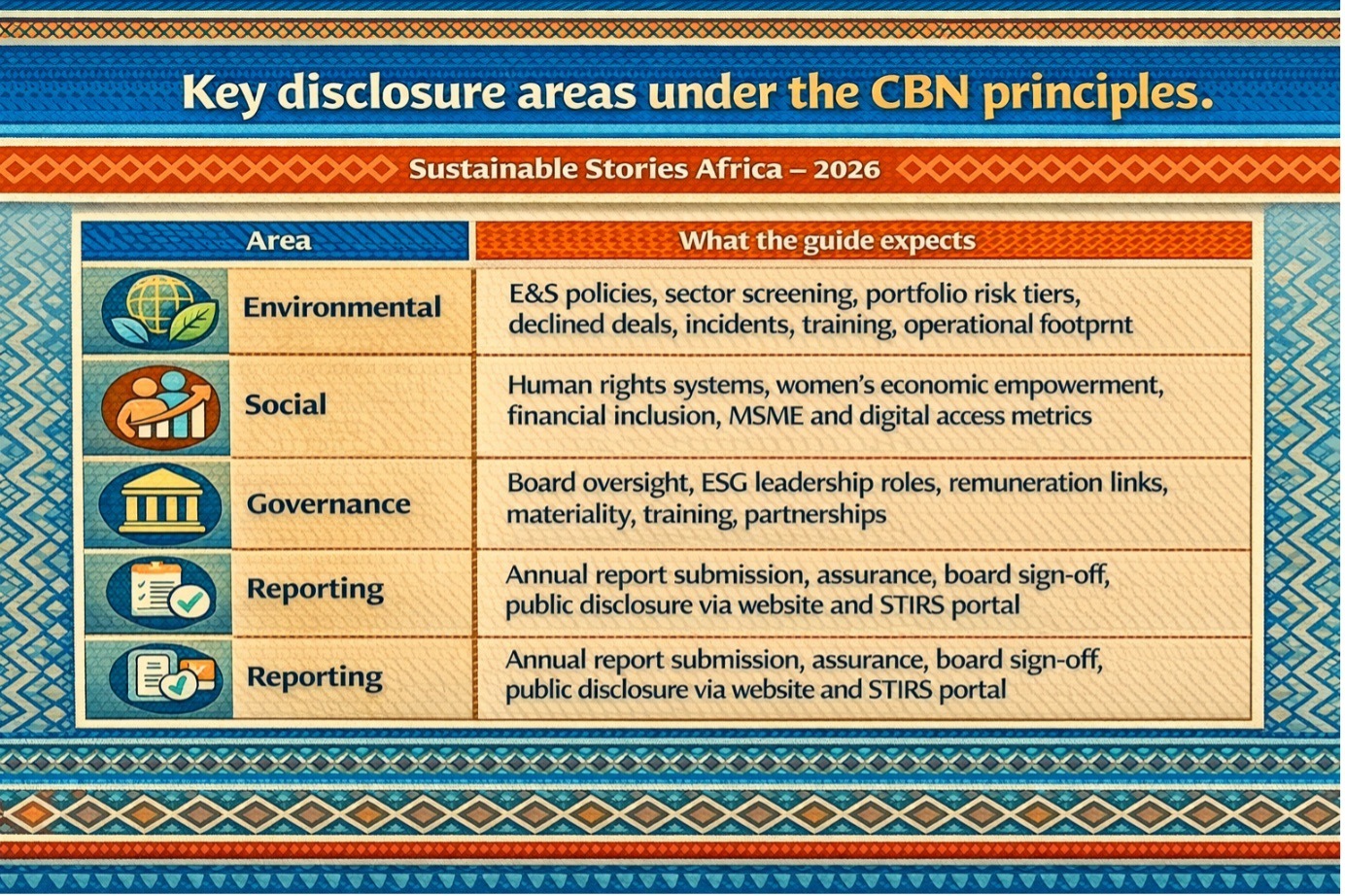

The sharpest signal in the document is that ESG has been translated into a practical reporting architecture. The overview on page 4 reduces the regime to nine principles across:

- Environmental & Social Risk Management – Environmental Dimension

- Environmental & Social Footprint – Environmental Dimension

- Human Rights – Social Dimension

- Women's Economic Empowerment – Social Dimension

- Financial Inclusion – Social Dimension

- E&S Governance – Governance Dimension

- Capacity Building – Governance Dimension

- Collaborative Partnerships – Governance Dimension

- Reporting – Governance Dimension

That breadth matters. It means banks are no longer being asked only whether they finance greener projects or publish polished reports.

They are being asked whether ESG is embedded in lending screens, grievance systems, board structures, women-focused finance, inclusion metrics, staff training and public disclosure processes. In other words, the regulator’s lens is moving from narrative intent to operational proof.

What Nigerian Banks Must Actually Show

The guide turns broad policy ambition into a disclosure checklist.

- On the environmental side, banks are expected to highlight whether E&S risk policies exist, which sectors face screening, how portfolios are distributed by risk, how many transactions were declined, and how incidents were reported and remediated.

- On the social side, the framework moves beyond philanthropy. It links ESG reporting to inclusion by tracking human rights, grievance cases, stakeholder consultations, female representation, lending to women-owned businesses, rural agent-banking reach, underserved-customer onboarding, MSME finance and digital use.

- On governance, the guide asks whether oversight sits at board level, whether sustainability roles and policies are in place, whether executive pay includes ESG targets, and whether materiality assessments, training partnerships and internal champions support implementation.

Why Better Reporting Could Change More Than Reports

If banks implement this well, the gains go beyond disclosures. Better sustainability reporting can improve access to international capital, reduce greenwashing risk, strengthen board visibility over hidden exposures, and support sharper pricing, monitoring and governance. Credible ESG data becomes an advantage.

There is a wider public dividend. A bank that tracks women-owned enterprise lending, rural access, grievance resolution, climate-sensitive exposure and emissions data is better placed to see who it serves, where risks are building, and where communities remain underserved today.

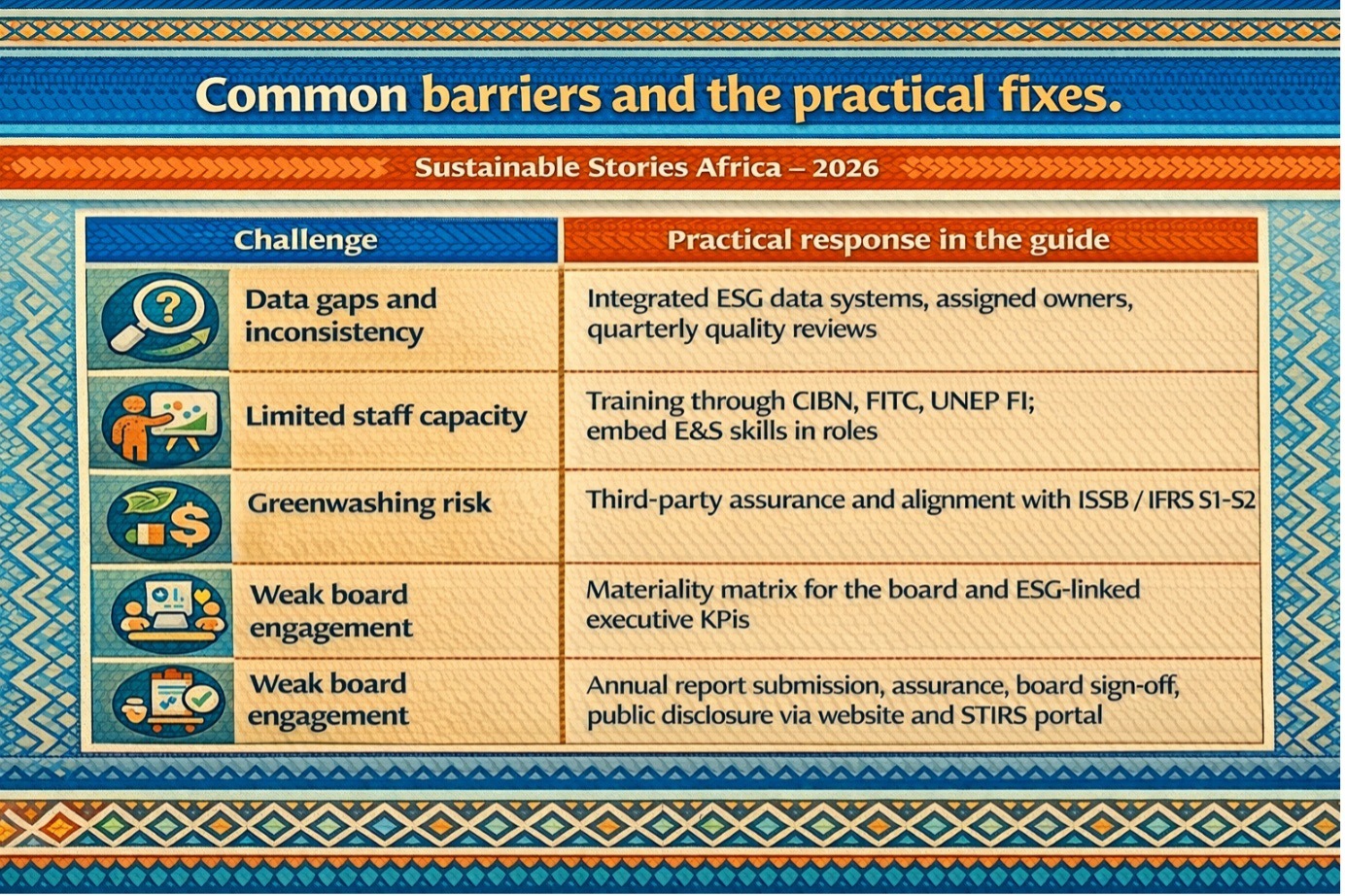

The risk is weak execution. Poor data, unclear boundaries, limited staff capacity and shallow board engagement can turn reporting into box-ticking. The answer is integrated data systems, defined ownership, quarterly reviews, external assurance and stronger executive accountability across the institution.

What Needs to Happen Next

The guide’s five-step reporting process is a useful operating agenda: establish a baseline, use the CBN template, seek assurance, secure board sign-off, then disclose and submit.

That sequence matters because it forces institutions to move from fragmented departmental data to a governed, attestable report.

- For regulators, the task is consistency and follow-through.

- For boards, it is ownership.

- For management teams, it is systems-building.

- For the market, it is to stop rewarding glossy language without comparable data.

The most practical strategic priorities in the document are also the most revealing: embed

- ESG in planning calendars

- Appoint a senior ESG reporting lead,

- Adopt globally credible frameworks

- Invest in reporting technology

- Collaborate through sector workstreams.

Path Forward – From disclosure to discipline

Nigeria’s banks are being asked to prove that sustainability is governed, measured and disclosed with the same seriousness as credit, liquidity and capital.

The CBN framework points toward structured data, board accountability, assurance and comparability.

What is being advocated is straightforward: make ESG reporting operational, not ornamental.

The institutions that move fastest will not only satisfy the regulator; they will be better placed to earn trust, attract capital and finance transition in a market that increasingly demands evidence.