Nigeria’s 2025 Tax Act is forcing the oil and gas industry to rethink. Signed in June 2025 and took effect on January 1, 2026, the reform changes deal with economics, tax planning and investment incentives across the sector.

The central question is whether the new framework will improve fiscal clarity without choking capital.

For upstream players, the answer may depend on how higher taxes, tighter exemptions and gas-focused incentives balance out in practice.

Tax Reform Meets Energy Strategy

Nigeria’s oil and gas sector is entering 2026 under a new fiscal script. The country’s 2025 Tax Act, signed into law in June 2025 and rolled out on January 1, 2026, is described by Chika Onyekwere’s briefing as the most sweeping tax overhaul in decades, with direct consequences for corporates, multinationals and sector-specific incentives.

For oil and gas, that means the reform is not a technical back-office adjustment. It is a strategic reset for capital allocation, asset transfers, gas expansion and competitiveness.

The law’s core signal is mixed but deliberate. It raises fiscal pressure through a higher capital gains tax, a development levy, tighter treatment of free-trade-zone activities and a 15% minimum effective tax rate for large multinationals.

On the other hand, it supports gas adoption through VAT relief on CNG and LPG, aligning parts of the tax system with Nigeria’s transition narrative.

In effect, the state is asking the sector to pay more carefully, invest more selectively and pivot more visibly toward gas.

For African and emerging-market observers, the Nigerian case matters beyond one jurisdiction. It shows how hydrocarbon economies are trying to modernise tax administration, protect revenues and still court capital in a world where oil remains vital, gas is being framed as a bridge fuel, and investors are increasingly sensitive to policy risk.

A bigger tax bill, a narrower margin for error

The clearest signal is the shift in capital gains tax. CGT on companies rises from 10% to 30%, with some asset-transfer regimes pushing rates to 85%.

For an industry built on farm-outs, divestments and restructuring, that materially changes deal economics and could slow capital recycling.

The reform package introduces a 4% development levy, presented as a consolidated charge. It sets a 15% minimum effective tax rate for large multinationals, narrowing room for incentive-driven tax planning and tightening pressure on operators.

The urgency is timing. The law took effect on January 1, 2026, meaning that companies should have spent the time from when the Act was signed to reprice assets, remodel transactions, test compliance exposure and reassess operating structures.

In upstream oil and gas, small tax shifts can decide whether deals proceed.

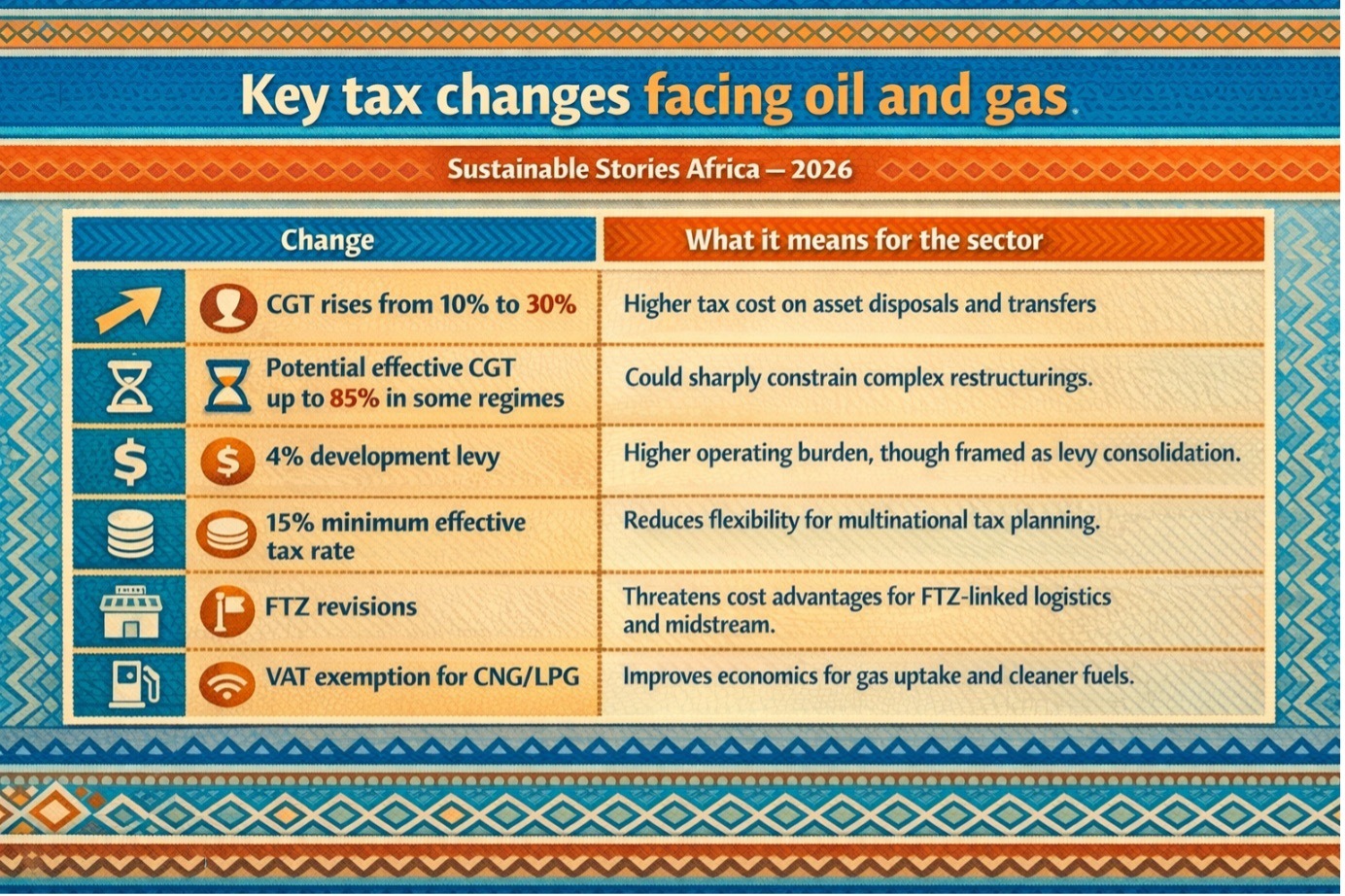

Key tax changes facing oil and gas

| Change | What it means for the sector |

|---|---|

| CGT rises from 10% to 30% | Higher tax cost on asset disposals and transfers |

| Potential effective CGT up to 85% in some regimes | Could sharply constrain complex restructurings |

| 4% development levy | Higher operating burden, though framed as levy consolidation |

| 15% minimum effective tax rate | Reduces flexibility for multinational tax planning |

| FTZ revisions | Threatens cost advantages for FTZ-linked logistics and midstream |

| VAT exemption for CNG/LPG | Improves economics for gas uptake and cleaner fuels |

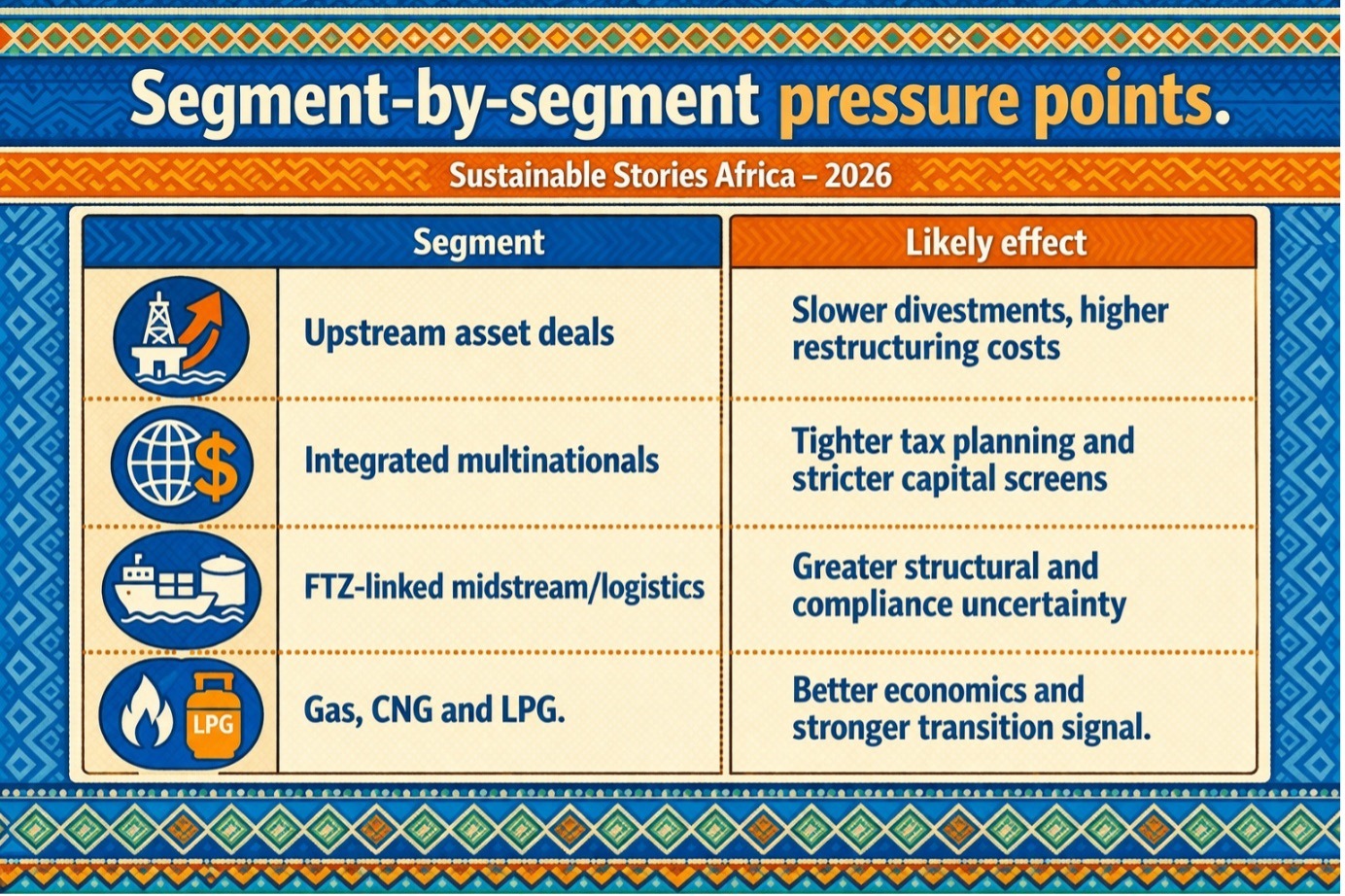

How the impact breaks across the value chain

The burden will not fall evenly. Upstream oil and gas companies face the most immediate pressure because asset transactions sit directly in the path of the CGT increase.

Mature field divestments, interest transfers and farm-in or farm-out structures become more costly, encouraging earn-outs, deferred consideration and deeper tax due diligence.

For multinationals, the problem is reduced room to optimise. The 15% minimum effective tax rate limits incentive-led planning and, alongside higher CGT, could force operators to reassess Nigeria against competing basins. Brownfield upgrades and marginal field acquisitions may face tougher hurdle rates.

Midstream and logistics players face increased uncertainty from the changes in free-trade-zone rules. Tighter FTZ exemptions could erode the cost advantage of fabrication yards, storage facilities and processing hubs.

That would not only raise tax bills; it could also reshape supply chains, customs planning and local-content execution.

However, the reforms may also open a clearer lane for gas. Removing VAT on CNG and LPG improves the economics of fleet conversion, LPG distribution, pipelines and compression infrastructure.

The analysis suggests that targeted incentives have already been linked to about $6 billion in oil investment. The broader signal is that while the fiscal net tightens around oil assets, policy is still trying to direct capital toward transition-linked gas investment.

What a better-balanced framework could unlock

The most constructive reading is that Nigeria is trying to do two things at once: extract value from a mature hydrocarbon sector and steer capital toward assets with long-term policy relevance.

Gas best shows this, with VAT exemptions for CNG and LPG improving fuel economics.

If implementation holds, that could matter. Nigeria has long cast gas as central to its transition, especially in transport, distributed power and industrial fuel switching.

Fiscal support for CNG and LPG will not decarbonise everything, but it lowers the costs of switching to cleaner energy sources.

There is also a governance test. The package aims to modernise tax administration and reduce leakages.

For investors, predictability can matter as much as low rates. A clearer regime could still support long-term energy investment, provided implementation stays transparent throughout.

What companies and policymakers need to do now

The paper urges operators to respond pragmatically. Companies need to rework portfolios and deal models around higher CGT, reprice acquisitions and divestments, and test options such as staggered sales, asset swaps and joint-venture restructuring.

Multinationals should also build the 15% effective tax floor into capital allocation, while firms exposed to FTZ rules should have reviewed their zone footprints, tested onshore alternatives and adjusted operating models.

At the same time, gas strategies should move faster, not slower, as VAT-free CNG and LPG improve the case for fleet conversion, distribution and smaller-scale gas hubs.

For policymakers, the test is clarity. Higher fiscal pressure without clear guidance on levies, FTZ treatment and deal structuring could deepen uncertainty as much as the tax burden itself.

Path Forward – Harder terms, clearer choices

Nigeria’s 2025 Tax Act does not read like a simple pro-investment package or a simple revenue grab.

It is a harder-edged fiscal redesign that raises costs for traditional oil strategies while giving gas a more visible policy tailwind.

What is being advocated, implicitly and explicitly, is adaptation: reprice deals, simplify structures, protect competitiveness and move faster where the incentives are clearest.

In Nigeria’s oil and gas sector, the next winners may be the operators that can handle tougher tax rules without losing strategic flexibility.