Sustainability acronyms once looked like specialist shorthand. In 2026, they have become the operating language for boards, exporters and regulators.

From IFRS and GRI to CBAM and SBTi, the question is no longer what the letters mean, but which ones now move capital, market access and corporate trust across Africa.

Acronyms That Now Move African Markets

The sustainability glossary has stopped being a side note in annual reports. It is now moving into trade rules, stock exchange guidance, lender questionnaires and board packs.

That shift is visible in hard policy. Thirty-seven jurisdictions have already decided to apply, or are taking steps to introduce, the ISSB Standards; together they account for about 60% of global GDP, more than 40% of global market capitalisation and roughly 60% of global greenhouse gas emissions.

The EU’s Carbon Border Adjustment Mechanism entered into force on 1 January 2026.

In Nigeria, the Financial Reporting Council (FRCN) has already updated its roadmap and Sustainability Reporting Guideline 1 to support the implementation of IFRS S1 and IFRS S2.

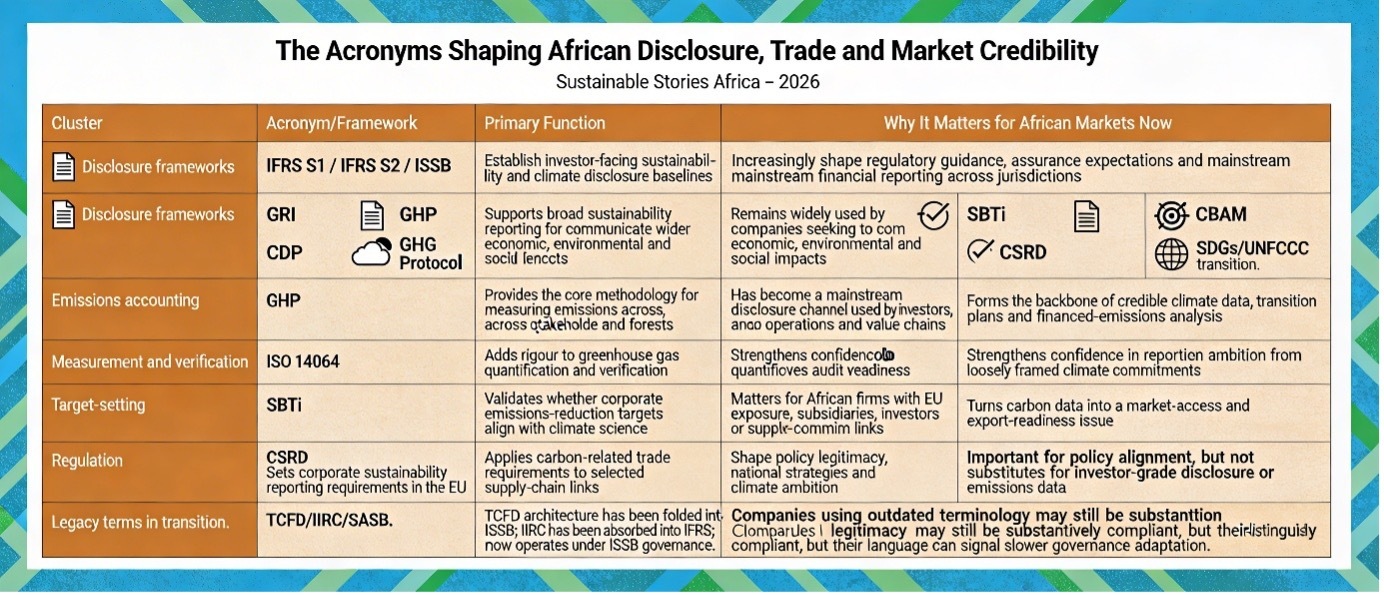

However, the acronym board many executives still carry around mixes very different things: disclosure frameworks, emissions-accounting systems, target-setting tools, development goals and trade measures.

For African businesses, sorting that language is no longer an academic exercise. It now affects export readiness, access to capital, investor confidence and the credibility of every climate or ESG claim.

Why Acronym Fluency Still Fails Disclosure

A revealing number lies at the centre of this debate: 82% of companies globally disclosed information aligned with at least one TCFD recommendation, but fewer than 3% reported in line with all 11.

That gap matters because it shows that acronym familiarity is not the same as disclosure readiness. TCFD itself has now been disbanded, with its monitoring role transferred and its architecture folded into the ISSB era; IFRS S2 has been effective for annual reporting periods beginning on or after 1 January 2024.

In other words, the problem for African markets is not a shortage of vocabulary. There is a shortage of translators. Companies may know the letters but still confuse a reporting baseline with a target framework, a carbon inventory method with a trade rule, or a development goal with an investor disclosure requirement. That confusion now carries financial consequences.

Why Sustainability Acronyms Need Strategic Clarity

The sustainability disclosure landscape has become both crowded and transitional. The Global Reporting Initiative (GRI) remains the world’s most widely used framework, with over 14,000 organisations in 100 countries and referenced in hundreds of policy instruments.

CDP, now mainstream rather than voluntary, captures disclosures from more than 24,000 companies representing approximately two-thirds of global market value.

Meanwhile, IFRS, through the ISSB sustainability standards, is emerging as the baseline shaping regulation and assurance expectations that global investors face.

Some acronyms have changed in meaning.

The former International Integrated Reporting Council (IIRC) was dissolved into the IFRS Foundation in 2022, and SASB Standards now operate within ISSB governance as industry-specific disclosure tools.

Companies still using legacy terminology may not be outdated in substance, but their language risks underselling governance maturity in an evolving reporting environment.

Measurement frameworks remain the operational backbone.

The Greenhouse Gas (GHG) Protocol provides accounting principles for emissions across value chains, complemented by the ISO 14064 verification structure.

The Science Based Targets initiative (SBTi) extends that chain by validating alignment with climate science; by early 2026, it had engaged 13,160 companies, with 10,000 holding validated targets.

On the policy side, Europe’s Corporate Sustainability Reporting Directive (CSRD) is being re‑calibrated under the 2025 Omnibus Proposal to focus reporting on large entities, while the Carbon Border Adjustment Mechanism (CBAM) is fully operational for carbon‑intensive trade sectors.

For global and African institutions, frameworks such as the SDGs and UNFCCC remain foundational to policy legitimacy. However, without GHG‑grade data and investor‑level transparency, corporate sustainability claims risk falling short of market credibility.

Why Systems Literacy Beats Acronym Fluency

If companies and regulators get this translation right, the upside is substantial.

A cleaner acronym map reduces duplication, improves reporting discipline and helps boards separate what they must disclose, what they must measure, what they may target and what they may face at the border. Inference from the direction of travel is straightforward: when standards, inventories and targets are aligned, companies are better placed to speak a language investors, regulators and procurement teams already recognise.

That is especially important in African markets, where credibility gaps can be expensive.

Nigeria’s updated FRC roadmap shows how local regulation is trying to narrow that gap with practical implementation guidance. For exporters, CBAM makes carbon data a trade issue.

For listed firms and banks, ISSB adoption means sustainability disclosure is steadily becoming part of mainstream financial reporting rather than a separate CSR annex. The winners will be companies that turn acronym literacy into systems literacy.

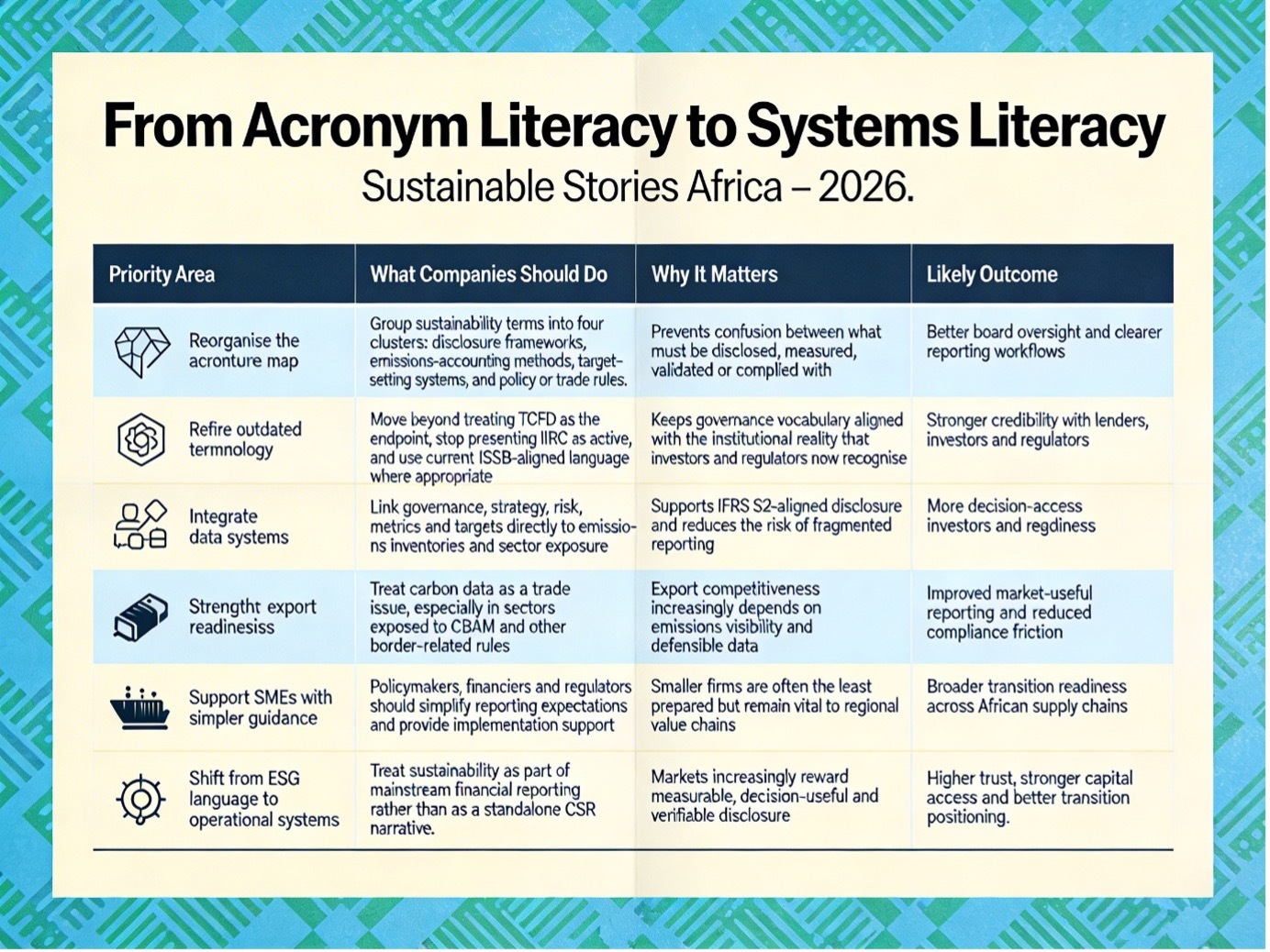

How Boards Can Simplify Sustainability Disclosure

The first practical step for companies is to reorganise the sustainability alphabet. Boards should group acronyms into four clusters

- Disclosure frameworks

- Emissions-accounting methods

- Target-setting systems

- Policy or trade rules.

This structure clarifies that IFRS/ISSB and GRI serve different reporting needs, GHG Protocol and ISO support measurement integrity, SBTi validates ambition, and CBAM and CSRD drive compliance pressure.

The second step is to retire outdated terminology. Firms should move beyond TCFD as an endpoint, stop presenting IIRC as active, and avoid using “ESG” as a one-size-fits-all label. The third step is data integration, linking governance, strategy, risk, metrics and targets directly to emissions inventories and sector exposure, as required under IFRS S2 and Nigeria’s evolving guidance.

Finally, policymakers and financiers must simplify reporting guidance, particularly for SMEs, treating clarity not as bureaucracy, but as a lever for competitiveness in global transition markets.

Path Forward – Translate, Align, Then Execute

African markets do not need more acronym clutter. They need clearer translation between disclosure rules, emissions accounting, targets and trade obligations.

That means updated glossaries, stronger data systems, export-focused readiness and governance that turns ESG language into measurable action.