South Africa’s market watchdog is moving sustainable finance from principle to practice, testing the use of taxonomy, tightening climate disclosure pathways and probing weak points in carbon markets and ESG data.

The bigger question for Africa is whether credible rules can arrive fast enough to protect investors, empower consumers and channel capital into a just, investable transition.

Rules Are Meeting Market Reality Fast

South Africa’s Financial Sector Conduct Authority (FSCA) is trying to do something many regulators still discuss more than implement: turn sustainable finance from a broad policy ambition into a conduct, disclosure and market-integrity agenda.

Its March 2026 update shows progress across taxonomy testing, retail claims guidance, climate disclosure design, carbon-market development, ESG ratings oversight and consumer education.

That matters beyond Pretoria. For African and emerging markets, the problem is no longer whether sustainability will shape capital flows.

The question is whether markets can build disclosure systems, product rules and consumer trust quickly enough to keep pace with global expectations while staying practical for local institutions and households.

The report suggests South Africa is choosing a phased route: climate first, conduct first, credibility first.

It is not promising instant perfection. It is building the plumbing, definitions, claims guidance, data standards, exchange engagement and market architecture that make sustainable finance believable rather than promotional.

Integrity Is Becoming Infrastructure

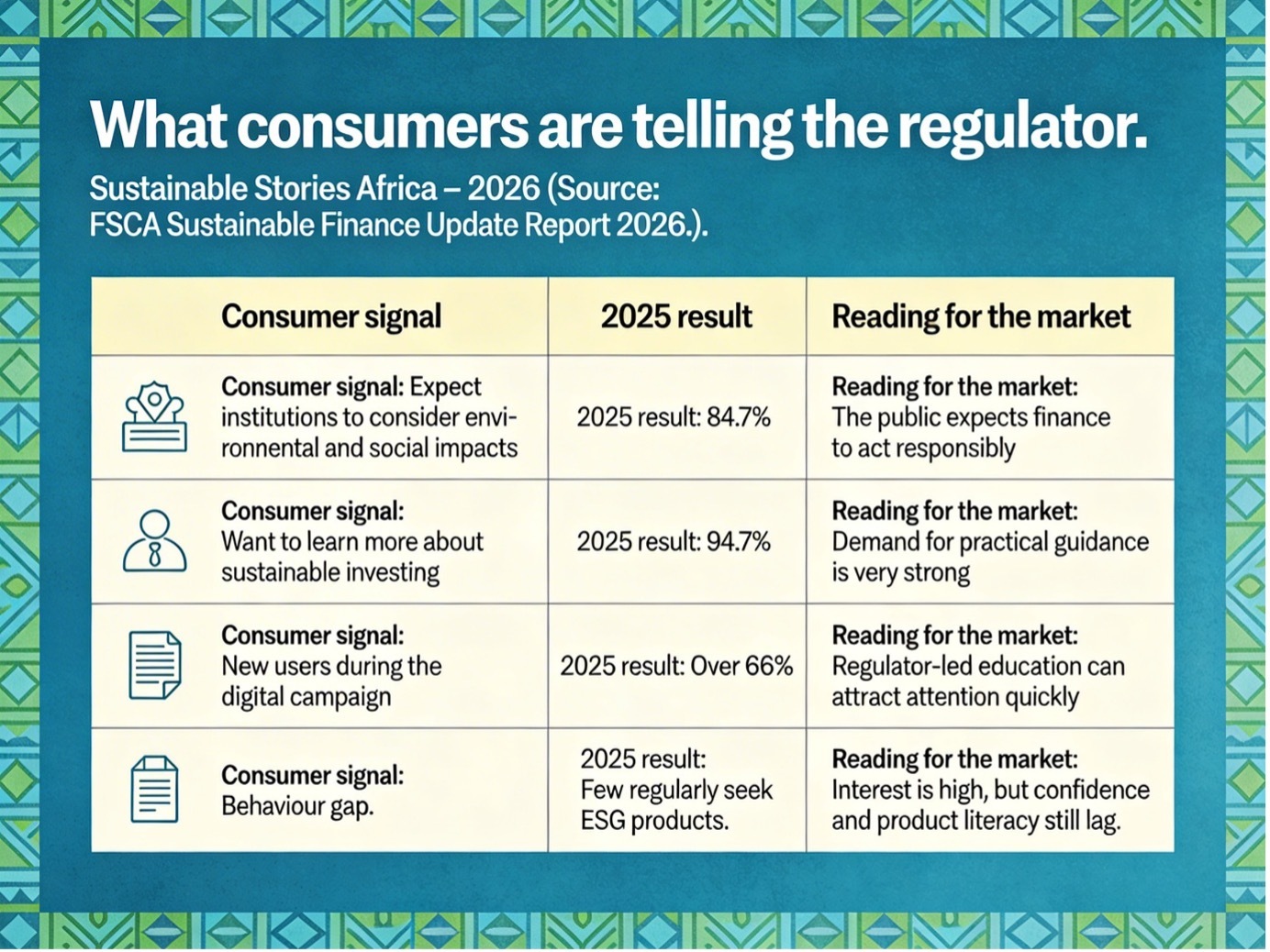

Consumer data suggests that South Africans are not just hearing about sustainable finance; they are actively looking for it.

During the FSCA’s March 2025 digital awareness campaign, new users on its consumer education platform jumped 66% week-on-week, while survey results show 84.7% of respondents want financial institutions to consider environmental and social impacts, and 94.7% want to learn how investments can help society and the environment.

That demand brings both opportunity and risk. Without stronger standards, rising interest could fuel greenwashing and impact washing.

The FSCA’s 2026 update responds by tightening what it calls the “sustainable finance information chain,” from corporate disclosures and retail product claims to ESG data providers, carbon-credit integrity and consumer literacy.

Geopolitics is amplifying the shift. Under South Africa’s G20 Presidency, sustainable finance work focused on global architecture, adaptation and just transitions, and unlocking carbon-market finance, including a Common Carbon Credit Data Model designed as a voluntary backbone for more consistent, interoperable carbon-credit data across markets.

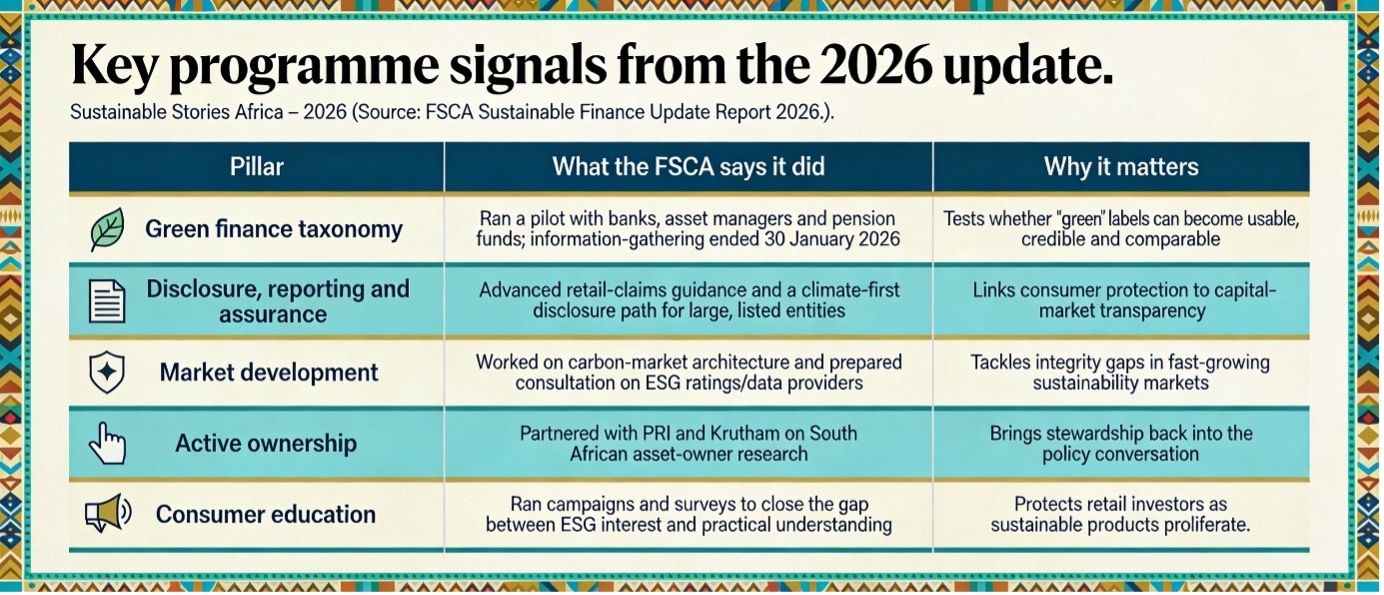

Five Pillars, One Market Signal

The report’s framework diagram organises sustainable finance into five pillars, taxonomy, disclosure and assurance, market development, active ownership and consumer education, underpinned by four enablers: capacity, research and engagement, regulatory development and stakeholder coordination.

It signals a full market‑conduct agenda, not a narrow reporting exercise.

The FSCA’s taxonomy work is deliberately cautious. South Africa’s 2022 Green Finance Taxonomy is being piloted through a “learn-by-doing” approach, testing how institutions collect, validate and disclose taxonomy data before any tougher rules are introduced, with findings due in 2026/27.

The taxonomy is globally interoperable but harder to use in practice, especially around Do No Significant Harm tests, Minimum Social Safeguards and incentive design, creating governance and adoption gaps.

On disclosure, the FSCA is tightening sustainability claims in retail markets and designing a climate-first pathway for listed companies aligned with IFRS S2 and the national ISSB roadmap.

It plans to use listing rules as a bridge to better climate disclosure. Market development is another priority: strengthening South Africa’s carbon tax and building a high-integrity compliance carbon-credit market, potentially classifying credits as unlisted securities.

The FSCA is also scrutinising ESG ratings and data providers, flagging opaque methods and inconsistent outcomes and preparing consultations based on IOSCO guidance.

What Credible Sustainable Finance Could Unlock

If this programme works, the gains will be much greater than compliance. Clearer use of taxonomy can reduce labelling disputes and lower credibility costs for green instruments.

Better retail claims guidance can help consumers distinguish evidence from marketing. Climate-first disclosure for large, listed companies can improve comparability, price discovery and capital allocation.

Stronger carbon-credit architecture can make decarbonisation finance more tradable and more trusted.

There is also a broader African lesson here. Many markets want more climate and transition capital, but capital rarely scales into systems that look inconsistent, poorly defined or vulnerable to misleading claims.

The FSCA’s update suggests that sustainable finance becomes more investable when regulators focus not just on ambition but on definitions, data integrity, proportionate supervision and consumer understanding. That is how trust compounds.

What Needs To Move Next

- The first task is to publish and follow through. The taxonomy pilot results need to be published, translated into clearer user guidance and linked to practical expectations for taxonomy-aligned disclosure. The report also says the dormant Climate Risk Forum is expected to be revived during 2026, which could help co-develop the next phase of taxonomy governance and usability.

- Second, disclosure reform needs sequencing, not drift. The FSCA should establish its climate-first approach for large, listed entities, and it also needs to define the initial scope, timing and proportionality of expectations clearly enough for boards, issuers and exchanges to prepare. On the retail side, claims guidance must be accessible and enforceable so that sustainability language in product design, advertising, advice and communications becomes more consistent.

- Third, carbon markets and ESG data cannot remain grey zones. The report makes clear that legal certainty, registry design, trading infrastructure and regulatory classification will shape whether carbon markets become credible sources of transition finance. The same is true for ESG ratings and data products: without more transparency and clearer policy expectations, market participants may rely on tools they do not fully understand.

Finally, consumer education must move from awareness to usable judgement. The FSCA’s next campaign, “Investing in Tomorrow: Understanding ESG and Sustainable Finance,” is designed to help consumers interpret claims, recognise red flags and seek authorised advice where appropriate.

That may sound modest beside taxonomy reform or climate disclosure, but it is central to market integrity.

A sustainable finance market that consumers cannot navigate will not stay credible for long.

Path Forward – Credibility Before Scale

South Africa’s regulator is building a phased sustainable-finance framework to support the usability of its taxonomy, climate disclosure, carbon-market integrity, ESG data oversight and consumer understanding. The message is simple: trust must be built before scale.

For African markets, the practical objective is not more ESG language. It is better rules, clearer data, stronger claims discipline and a transition architecture that investors and citizens can believe.