Nigeria's 39 million micro, small, and medium enterprises form the backbone of the economy, accounting for nearly half of GDP and over 80% of employment.

However, the majority cannot access the formal financing they need to grow, not because the money does not exist, but because they do not know the rules of the game.

A practical framework published by ESG and sustainability advisor Chika Onyekwere offers a step-by-step guide to navigating microfinance bank funding, government schemes, and borrower protections, changing the equation for millions of entrepreneurs.

Small Business, Massive Stakes

Nigeria's MSMEs are not marginal; they are the economy. With nearly 40 million enterprises generating close to half of the country's GDP and employing more than 80% of its workforce, the health of this sector directly determines whether Nigeria achieves financial inclusion, reduces poverty, and achieves sustainable economic growth.

However, for most operators, the market trader in Surulere, the artisan in Aba, the small agripreneur in Kano, access to formal credit remains a distant reality, blocked by documentation gaps, predatory lenders, and a system that was never clearly explained to them.

That gap is now being directly addressed. Chika Onyekwere, Senior Sustainability Advisor and ESG Strategy Lead, has published a detailed, 12-step practical framework — How Nigerian MSMEs Can Access Microfinance Bank (MFB) Funding, designed to demystify Nigeria's formal microfinance architecture and empower entrepreneurs to access the capital their businesses deserve.

The guide, released in March 2026, is built on CBN regulatory frameworks, borrower rights protections, and ESG-informed due diligence principles that reflect the evolving expectations of responsible finance in African markets.

39 Million Businesses, One Broken Pipeline

Here is the paradox at the heart of Nigerian enterprise: over 39 million MSMEs contribute nearly half of GDP, yet the majority operate without access to a single formal credit facility.

Over-indebtedness from predatory digital lenders, charging monthly interest above 10%, equivalent to 120% or more annually, has become the number one financial trap for micro-entrepreneurs in Nigeria.

Millions of business owners sign agreements they do not understand, for amounts they cannot repay, from institutions that were never licensed by the Central Bank of Nigeria (CBN).

The cost is not just personal. When small businesses are starved of affordable capital, supply chains fragment, jobs are not created, and economic resilience erodes.

For Nigeria, where MSMEs account for more than 80% of employment, this financing deficit is also a sustainability, governance, and development crisis.

Onyekwere's framework arrives as a direct corrective, a plain-language, evidence-led guide that maps the formal system, exposes its risks, and gives entrepreneurs a defensible path forward.

"In today's market, ESG isn't just about compliance — it's about access to capital, operational continuity, and long-term competitive advantage in a rapidly evolving energy landscape." Chika Onyekwere, Senior Sustainability Advisor, ESG Strategy

Understanding the System Before You Enter It

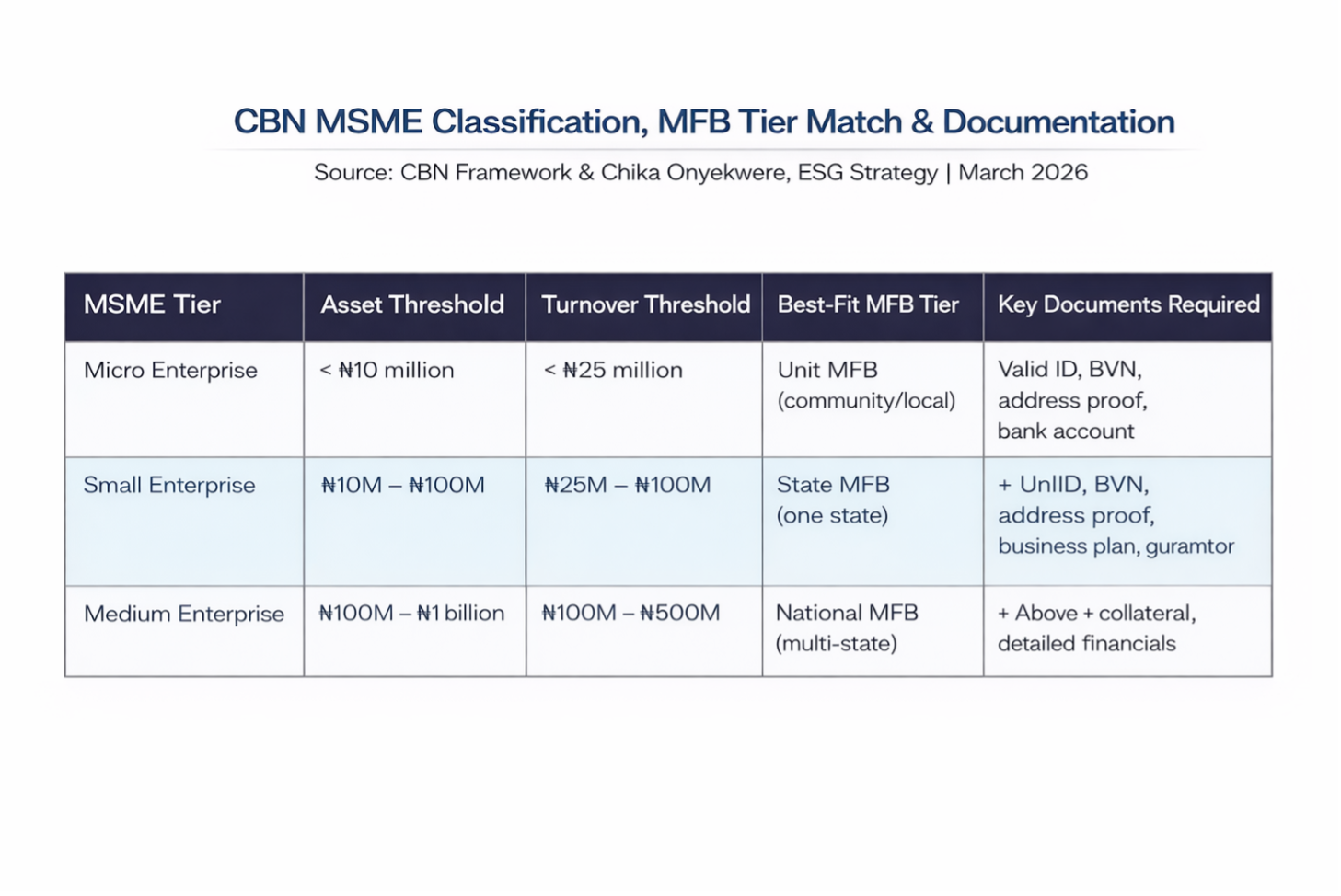

The framework begins with a simple but decisive principle: know your business category. The CBN classifies MSMEs into Micro, Small and Medium tiers based on asset value and annual turnover, and that classification shapes which microfinance bank tier an entrepreneur can access, the products available, and the documentation required.

It then links enterprise size to the three licensed MFB tiers. Unit MFBs serve traders and artisans within a single community, State MFBs support growing SMEs across one state, and National MFBs cater to established businesses operating across multiple states.

Choosing the wrong tier can waste time and expose entrepreneurs to unlicensed lenders.

The framework’s second message is financial discipline. Before applying, entrepreneurs should calculate monthly revenue, expenses, profit and existing repayment obligations.

The core rule is clear: new loan repayments should stay within 30% – 35% of monthly profit. Beyond that, the guidance is to walk away.

It also introduces a less visible but important reality: due diligence now runs deeper. Through a Two-Tier Due Diligence Framework, environmental and social screening applied by commercial banks to MFBs can extend to MSME borrowers.

That means businesses in higher-risk sectors such as charcoal production, artisanal mining, plastic recycling and some agricultural activities may face enhanced checks designed to support safer, more responsible finance.

What Formal Credit Can Unlock

When Nigerian MSMEs successfully use the formal microfinance system, the benefits can build quickly.

A well-managed loan can strengthen credit history, opening the door to larger facilities, lower borrowing costs, access to commercial banks and eligibility for government-backed funding.

However, many entrepreneurs still do not use existing credit bureau tools, including free annual reports from CRC Credit Bureau and First Central Credit Bureau.

The opportunity extends beyond lending. Government schemes already serve different MSME segments, while the ESG dimension of finance is becoming more important.

Microfinance banks that apply Social Performance Management, by tracking income improvement, offering financial literacy and adapting products to the borrower’s borrowing needs, are increasingly aligned with what regulators, development finance institutions and impact investors want.

MSMEs that fit that model will be better placed to access green finance, impact capital and wider development funding.

What Must Change, and Who Must Move

The framework sets out seven non-negotiable Client Protection Principles that every entrepreneur should use to assess a microfinance bank: appropriate products, prevention of over-indebtedness, transparency, responsible pricing, fair treatment, data privacy and accessible complaint channels.

It also points to three immediate actions for borrowers: register with the CAC, build a consistent banking history and check credit reports annually through recognised bureaux.

- For lenders, the message is equally clear. These protections should be treated as a minimum standard.

- Social Performance Management should focus on borrower outcomes rather than extraction.

- Regulators must step up action against predatory lending.

- Government agencies need to close the awareness gap around existing MSME funding schemes so more eligible businesses can access formal support.

Path Forward – Nigeria’s MSME Finance Gap Is Fixable

Nigeria’s MSME financing gap is not mainly a shortage of products. It is a gap in financial literacy, awareness and accountability.

The formal tools, institutions and funding schemes needed to serve millions of enterprises already exist; however, many business owners still lack a clear practical understanding of how to use them.

The way forward is straightforward. Regulators must enforce borrower protections more firmly, microfinance banks must compete on social impact rather than extraction, and MSME owners must approach formal credit with a clear grasp of their numbers, their rights and the opportunities responsible finance can unlock.