Most African companies understand the word ESG. However, few know precisely where they stand on the maturity spectrum that determines their access to capital, supply chain inclusion, and long-term competitive positioning.

A structured four-stage framework, from Unaware to Embedded, is now exposing Africa's corporate readiness gap in sharp relief.

With Nigeria's Financial Reporting Council mandating IFRS S1 and S2 sustainability compliance for public interest entities by 2028, and institutional investors hardening their ESG screening criteria, the window for honest self-assessment is closing fast.

Mapping Africa's ESG Corporate Readiness Gap

Africa’s corporate sector is approaching a defining ESG inflexion point. The four-stage maturity model, Unaware, Reactive, Proactive and Embedded, now serves as both a diagnostic lens and a strategic guide, showing companies not only where they stand, but how far many still have to travel to remain competitive in a changing global market.

The risks of remaining at the lower end of that curve are rising. Companies with weak ESG systems face tighter access to international capital, greater vulnerability to sustainable sourcing requirements and growing exposure to disclosure rules.

In Nigeria, the FRC’s adoption roadmap makes IFRS S1 and S2 mandatory for public interest entities from 2028 and for SMEs from 2030, tightening the timeline for preparedness.

However, the opportunity is equally clear. Access Bank’s sustainability reporting includes independent third-party assurance, while Kenya’s green bond programme shows how credible ESG progress can help mobilise capital for green development.

A Continent at a Crossroads

More than 70% of institutional investors now identify poor and inconsistent ESG data as a major obstacle to investment decisions in emerging markets.

For Africa, a continent drawing growing flows of sustainability-linked capital, that figure cuts directly to the core of the readiness problem.

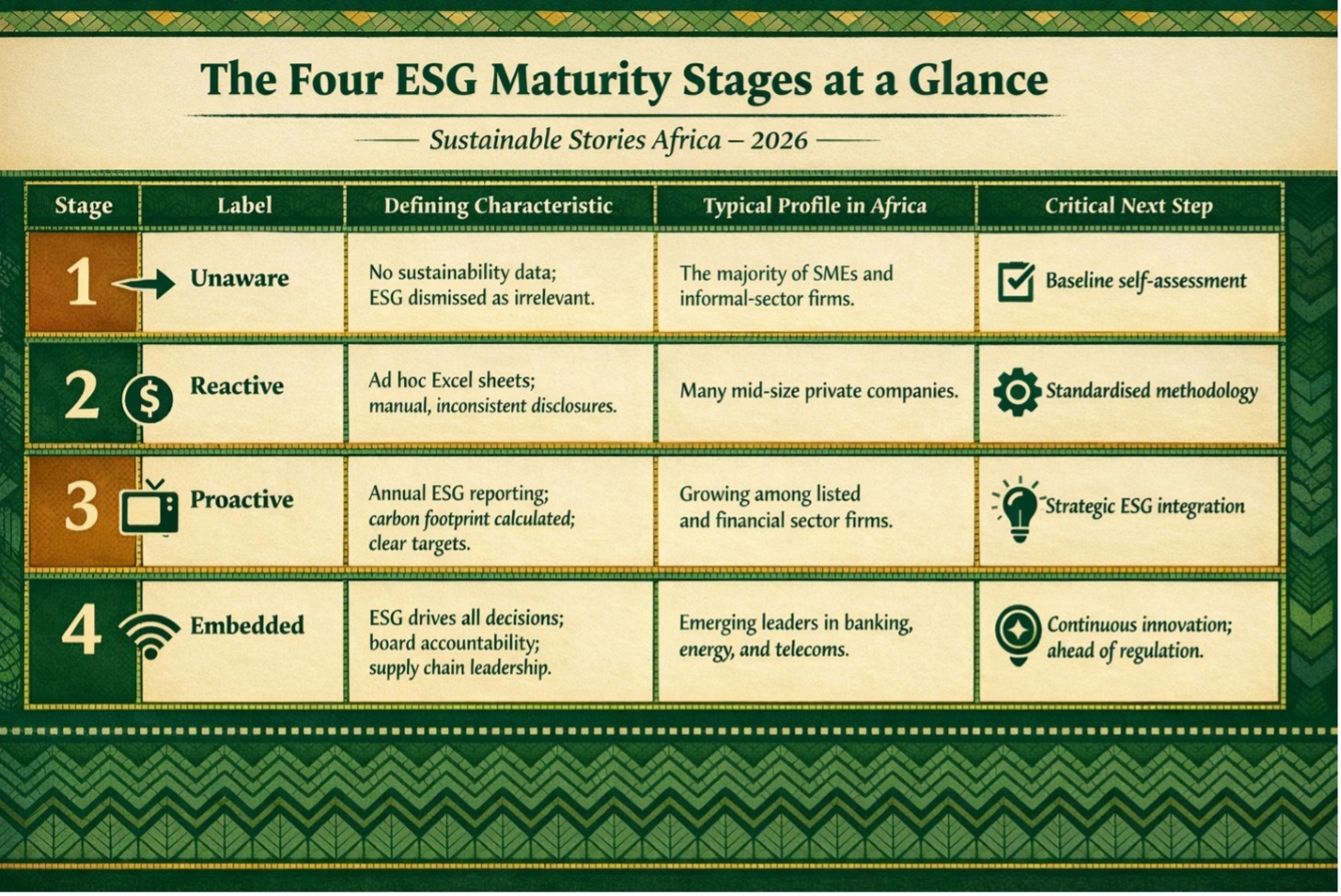

The ESG maturity model maps the full corporate spectrum across four stages.

- Stage 1, Unaware, describes companies with no sustainability data, no reporting infrastructure, and a prevailing mindset that ESG is irrelevant to their size: "We're too small for this" is the defining refrain.

- At the opposite end, Stage 4, Embedded, defines organisations where ESG drives every business decision: board-level accountability is established, supply chains are actively managed for sustainability performance, and the company is recognised as a sector leader.

The distance between these two poles is not merely technical; it is strategic, institutional, and cultural.

The Carbon Border Adjustment Mechanism is now fully operational in 2026, raising the compliance bar for African exporters.

The KPMG ESG Assurance Maturity Index 2025, which for the first time included African firms in its survey of 1,320 global companies, confirms that even in more advanced markets, full ESG assurance readiness remains the exception rather than the rule.

Four Stages, One Urgent Reality

The maturity framework delineates four distinct corporate archetypes, each with specific characteristics, challenges, and a critical next step required to advance.

The Four ESG Maturity Stages at a Glance

| Stage | Label | Defining Characteristic | Typical Profile in Africa | Critical Next Step |

|---|---|---|---|---|

| 1 | Unaware | No sustainability data; ESG dismissed as irrelevant | The majority of SMEs and informal-sector firms | Baseline self-assessment |

| 2 | Reactive | Ad hoc Excel sheets; manual, inconsistent disclosures | Many mid-size private companies | Standardised methodology |

| 3 | Proactive | Annual ESG reporting; carbon footprint calculated; clear targets | Growing among listed and financial sector firms | Strategic ESG integration |

| 4 | Embedded | ESG drives all decisions; board accountability; supply chain leadership | Emerging leaders in banking, energy, and telecoms | Continuous innovation; ahead of regulation |

The data present a clear continental picture. In Ethiopia, corporate sustainability momentum is rising, but the absence of a unified ESG framework, robust monitoring systems, and sufficient numbers of skilled professionals continues to limit progress.

In Nigeria, companies across banking, energy, and manufacturing are preparing for the adoption of IFRS S1 and S2, placing the country among Africa’s early movers while also highlighting the scale of work still needed to move firms from reactive to proactive ESG practices.

The strong turnout at Johannesburg’s Sustainability & ESG Africa Conference 2025 also reflects growing institutional interest, even as implementation remains uneven.

That gap matters because Africa’s green opportunity is expanding quickly. With millions of green jobs projected by 2030, companies will need stronger data systems, governance structures and reporting capacity to capture that growth.

The Opportunity Within the Gap

The same gap that heightens risk also reveals a clear commercial opportunity. Companies moving from Stage 1 to Stage 2 gain structured data systems, reduce manual processes and establish credible sustainability baselines.

Advancing from Stage 2 to Stage 3, through consistent reporting and measured carbon footprints, opens access to ESG-linked capital, green bonds and sustainability-linked loans.

Access Bank Nigeria highlights a pathway that uses embedded ESG practices and third-party assurance reporting to strengthen its leadership position.

The move from Stage 3 to Stage 4 is more transformative still. At that level, ESG shapes core decisions, deepens investor confidence, strengthens supply chains and helps attract values-driven talent.

Value Unlocked at Each Maturity Transition

| Stage Transition | Key Capability Gained | Strategic Opportunity Unlocked |

|---|---|---|

| Stage 1 → Stage 2 | Structured data: manual work eliminated | Baseline ESG credibility; stakeholder trust |

| Stage 2 → Stage 3 | Annual reporting, carbon accounting, and targets set | ESG-linked financing; investor access; export market readiness |

| Stage 3 → Stage 4 | Board-level ESG accountability; supply chain integration | Green bond issuance; sustainability leadership recognition; competitive differentiation |

Who Must Move, and How

Advancing Africa's ESG maturity at scale requires deliberate, coordinated action across multiple actors simultaneously.

- Businesses must begin with an honest assessment of their ESG maturity. Stage 1 requires a baseline; Stage 2 demands standardised data systems; Stage 3 must turn reporting into strategy, while Stage 4 leaders sustain innovation and stay ahead of regulation.

- Regulators and policymakers must accelerate the development of clear, locally adapted ESG frameworks that align with IFRS, GRI, and TCFD standards while reflecting African market realities. Nigeria's FRC roadmap, with its structured timeline and sectoral sequencing, offers a replicable model for other African jurisdictions navigating this transition.

- Financial institutions and capital providers must use allocation decisions to reward maturity advancement. Sustainability-linked loans and green bond issuance criteria should explicitly incentivise stage progression, not just disclosed outcomes.

- Development finance institutions must fund ESG capacity-building across Africa's SME sector, which constitutes the backbone of African economies but remains disproportionately concentrated at Stage 1.

Path Forward

Africa’s ESG maturity journey is no longer a luxury; it is a competitive and systemic necessity.

Businesses must advance with honest self-assessment, stronger data systems and real board-level accountability. In the same vein, regulators, investors and development partners must build the frameworks, access to capital and capacity needed to support progress.

The message is now unmistakable: ESG is not a destination, but an urgent path. For African businesses, the real question is no longer whether to begin, but how quickly they can move and how many can move together.