A practical guidance series published in March 2026 provides Africa's financial institutions with a comprehensive, framework-aligned roadmap for assessing, measuring, and disclosing climate-related financial risks.

Authored by Senior Sustainability Advisor Chika Onyekwere, the guide addresses physical, transition, and liability risk types, aligned with ISSB IFRS S2, TCFD, NGFS, and Nigeria's CBN Sustainable Banking Principles.

With $2.5 trillion in global assets at risk by 2030 and a disorderly climate transition projected to wipe between 10% and 15% off global GDP, the guidance is no longer theoretical; it is an operational imperative for banks, insurers, and asset managers across the continent.

Pricing the Unpriced Risk in Finance

Climate risk is no longer a macro concern; it is actively migrating into loan books, investment portfolios, and insurance liabilities across African financial markets. A new practical guidance series, published on 12 March 2026 by Chika Onyekwere, Senior Sustainability Advisor at ESG Strategy, offers a landmark framework for how financial institutions in Africa must identify, quantify, and disclose climate-related financial risks embedded in their portfolios.

The stakes are particularly acute for African institutions. Sub-Saharan Africa is projected to experience temperature increases of 1.5°C to 3.5°C by 2050, with cascading impacts on agricultural lending books, coastal collateral values, and capital adequacy for institutions most exposed to flooding, drought, and infrastructure degradation.

Nigeria's FRCN mandate for IFRS S2 adoption, the CBN Sustainable Banking Principles, and Basel Pillar 2 requirements for emerging markets are collectively compressing the window for action.

With over 140 jurisdictions now adopting ISSB standards and $130 trillion in assets under management committed to net-zero targets, the ability to assess and disclose climate risk is rapidly becoming a precondition for market access, not merely a compliance formality.

The Cost of Inaction Is Quantifiable

—"Financial institutions that fail to assess these risks today will face capital adequacy challenges tomorrow." – NGFS, 2024

That warning is no longer hypothetical. Under a Hothouse World scenario, where global temperatures exceed 3.5°C due to policy inaction, physical climate losses could exceed $5 trillion in global GDP by 2050, sovereign risk ratings for African agricultural states would deteriorate sharply, and coastal and delta assets would approach near-zero collateral value.

For Nigeria, where major financial institutions hold significant exposure to coastal real estate, oil and gas infrastructure, and agricultural lending, the risk is systemic.

Under even a disorderly transition scenario, delayed action followed by abrupt policy tightening, insurance flood and storm claims in Africa are projected to surge three to five times, while non-performing loans across oil and gas portfolios could spike by up to 8%, and lending rate premiums could rise by 30 – 60 basis points above current levels.

Three Risk Types Every Institution Must Assess

The guidance delineates three core categories of climate-related financial risk, each requiring distinct methodologies and metrics.

- Physical risks – both acute and chronic - arise from climate-driven weather, temperature, and ecosystem changes. They impact borrower creditworthiness, collateral values, and operational resilience. For African lenders, river and coastal flooding, extreme rainfall, sea-level rise (projected to be +0.44m by 2100 under SSP2-4.5), and chronic drought are the most material hazards.

- Transition risks – emerge from the policy, technology, and market shifts associated with moving to a lower-carbon economy. Carbon pricing, regulatory mandates, and technology disruption can render high-carbon assets stranded and push up the cost of capital for institutions with undisclosed exposures.

- Liability risks – arise where inadequate climate disclosure exposes institutions to legal challenge, regulatory sanction, or reputational damage, a growing concern as mandatory frameworks tighten.

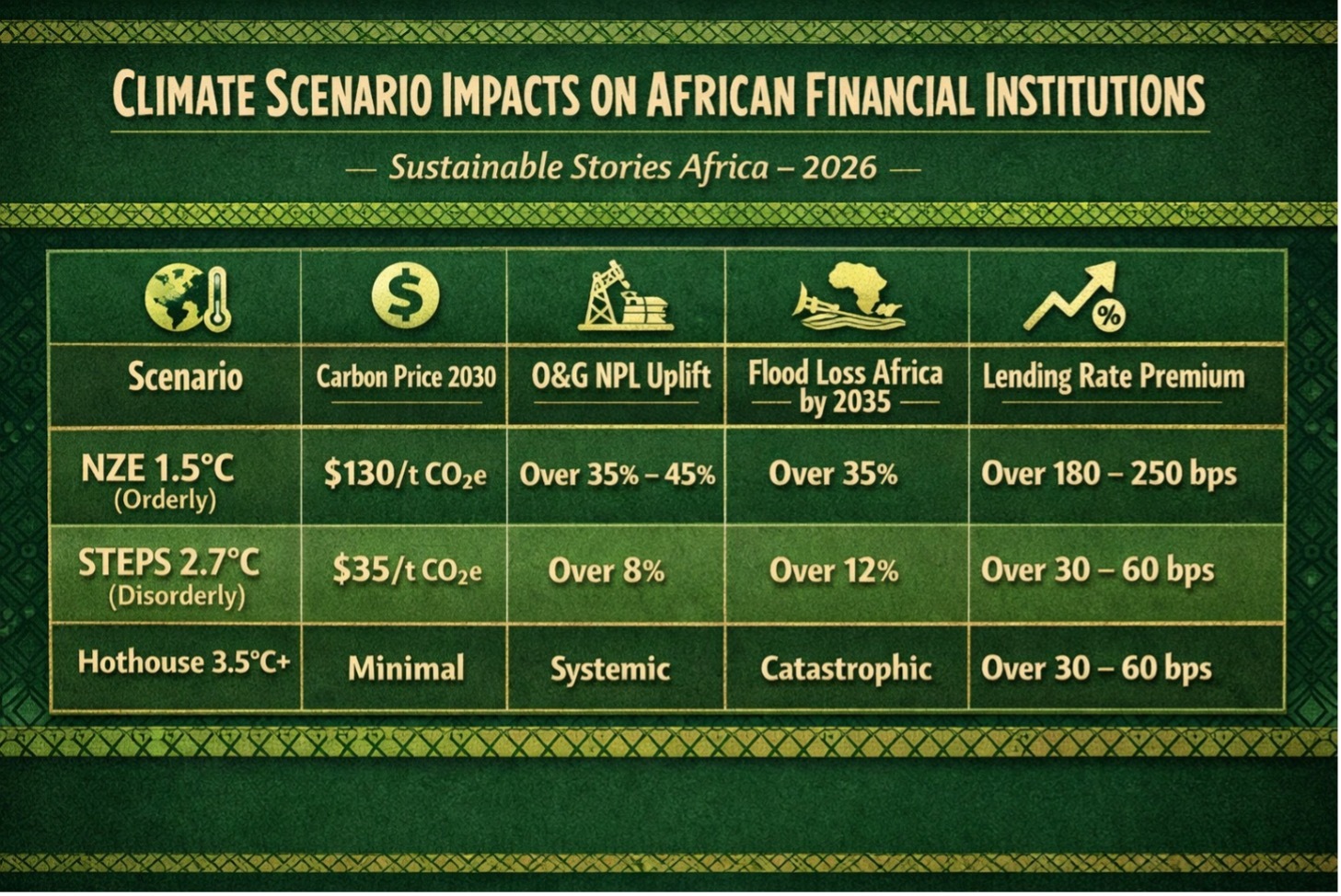

Climate Scenario Impacts on African Financial Institutions

| Scenario | Carbon Price 2030 | O&G NPL Uplift | Flood Loss Africa by 2035 | Lending Rate Premium |

|---|---|---|---|---|

| NZE 1.5°C (Orderly) | $130/t CO₂e | Over 35% – 45% | Over 35% | Over 180 – 250 bps |

| STEPS 2.7°C (Disorderly) | $35/t CO₂e | Over 8% | Over 12% | Over 30 – 60 bps |

| Hothouse 3.5°C+ | Minimal | Systemic | Catastrophic | Capital adequacy failure |

What Strong Climate Risk Management Unlocks

Institutions that build robust climate risk capabilities stand to gain decisive advantages. Access to development finance institution facilities, from the African Development Bank to the IFC, increasingly requires demonstrated climate risk management aligned with NGFS, TCFD, and IFRS S2 standards. Institutions that cannot evidence this alignment face exclusion from concessional capital pools and credit rating downgrades.

Conversely, proactive portfolio rebalancing toward green infrastructure and climate-resilient sectors opens access to the rapidly growing universe of sustainability-linked financing instruments that have seen double-digit growth in African markets. Under an orderly transition scenario, renewables and green infrastructure lending are explicitly projected to expand strongly.

A Five-Step Path to Portfolio Integration

The guidance prescribes a clear, executable five-step methodology for integrating climate risk across a financial institution's entire portfolio, from data collection to board-level disclosure:

- Map all exposures – to sector codes; identify geographic location of collateral; flag high-carbon sectors including oil and gas, mining, transport, power, and agriculture

- Screen for materiality – compute weighted average carbon intensity (WACI) and identify top 20 counterparties by climate-related revenue exposure

- Score and heat-map – each counterparty using physical (location-based) and transition (sector-based) risk scores; flag RED/AMBER exposures for enhanced due diligence

- Run scenario analysis – using NGFS Orderly, Disorderly, and Hothouse pathways; quantify PD uplift, LGD change, revenue stress, and capital ratio impact

- Disclose and embed – results in TCFD/IFRS S2 reports, Pillar 3 regulatory submissions, and credit pricing processes; submit to CBN and FRCN as required

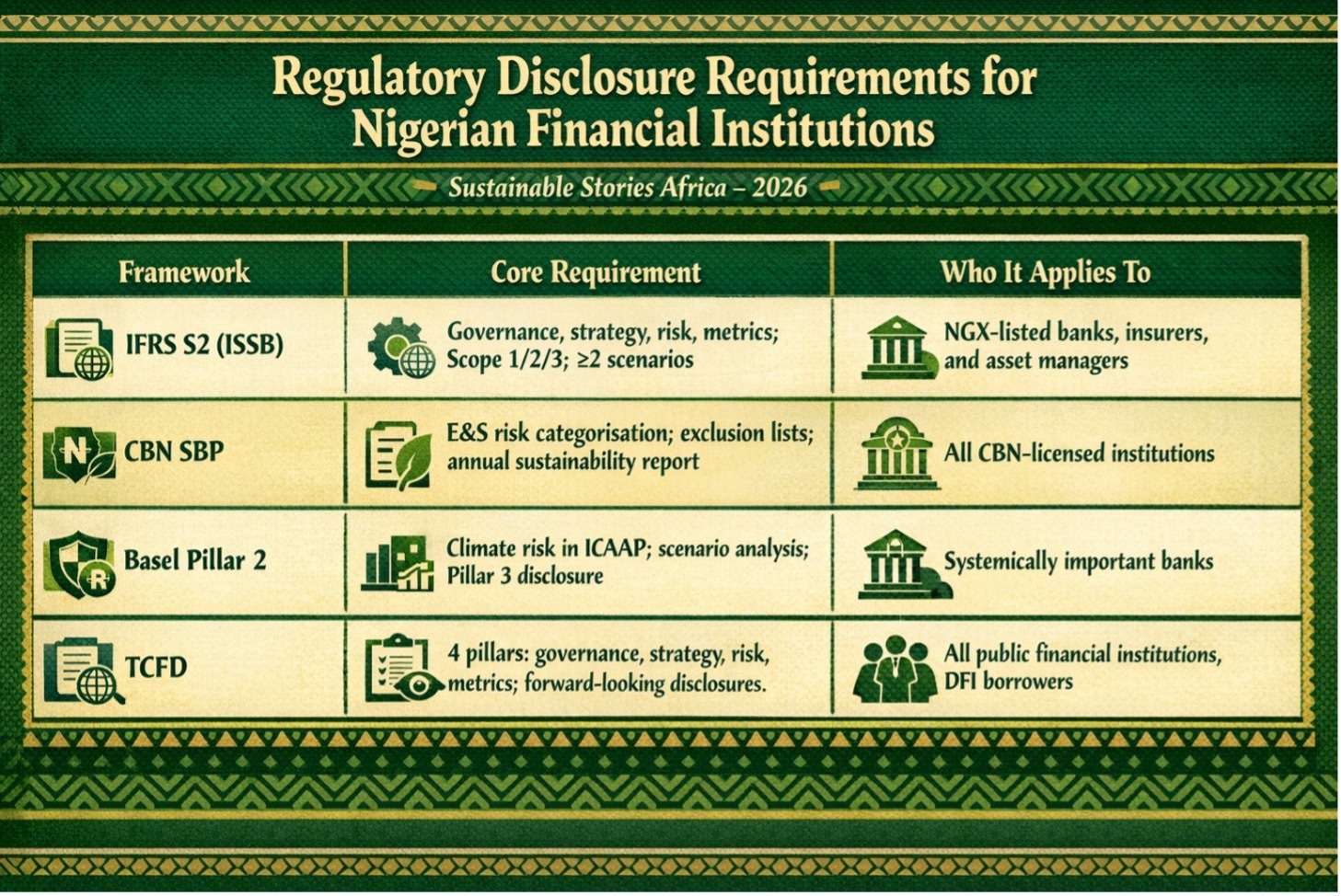

Regulatory Disclosure Requirements for Nigerian Financial Institutions

| Framework | Core Requirement | Who It Applies To |

|---|---|---|

| IFRS S2 (ISSB) | Governance, strategy, risk, metrics; Scope 1/2/3; ≥2 scenarios | NGX-listed banks, insurers, and asset managers |

| CBN SBP | E&S risk categorisation; exclusion lists; annual sustainability report | All CBN-licensed institutions |

| Basel Pillar 2 | Climate risk in ICAAP; scenario analysis; Pillar 3 disclosure | Systemically important banks |

| TCFD | 4 pillars: governance, strategy, risk, metrics; forward-looking disclosures | All public financial institutions, DFI borrowers |

Path Forward – Risk to Resilience: Financing Climate Accountability

Africa's financial institutions must treat climate risk assessment not as a future obligation but as an active, board-owned discipline embedded in credit, risk, and capital management processes today.

The guidance framework published by Chika Onyekwere provides an executable, standards-aligned pathway that removes the excuse of uncertainty.

The direction of regulatory travel, across the CBN, FRCN, ISSB, and Basel, is unambiguous. Institutions that invest now in climate risk capabilities will access cheaper capital, avoid NPL shocks, and lead the green economic transition.