The Greenhouse Gas Protocol, the world's most widely used framework for measuring and managing corporate emissions, has been undergoing its most significant revision since 2004.

As the GHG Protocol's third edition takes shape and IFRS S2 mandates Scope 3 reporting, African businesses face a defining question: do they understand what they are required to measure?

For a continent where Ghana and Nigeria report ISSB readiness scores of just 46% and 48%, respectively, and where Scope 3 emissions can represent between 70% and 90% of a company's total carbon footprint, building GHG accounting literacy is no longer optional; it is market critical.

Africa's Carbon Reporting Knowledge Gap Exposed

Corporate carbon accounting has entered a new era of accountability, and Africa's businesses must move quickly to keep pace.

The GHG Protocol, established as the global standard for corporate greenhouse gas measurement and reporting, structures emissions across three scopes: Scope 1 (direct emissions), Scope 2 (indirect emissions from purchased energy), and Scope 3 (all other value chain emissions).

Understanding this framework is now a baseline competency requirement for any company subject to IFRS S2, CBN Sustainable Banking Principles, JSE listing requirements, or international investor scrutiny.

The GHG Protocol is simultaneously undergoing a major update, and Phase 1 revisions to its Corporate Standard are progressing, with a third edition set to replace the current 2004 version.

Public consultation on revised Scope 2 guidance closed in December 2025, while IFRS S2 amendments now allow jurisdictional flexibility on certain Scope 3 Category 15 (financed emissions) disclosures.

The landscape is shifting, but only companies that have already mastered the fundamentals will be positioned to navigate these changes.

The knowledge gap in Africa is real and measurable. Studies of listed companies in Ghana, Nigeria, and South Africa reveal that readiness for ISSB standards, which require full GHG accounting, stands at 46%, 48%, and 78%, respectively, with the primary constraint cited as insufficient technical expertise and inconsistent GHG data.

Addressing this gap starts with a clear, shared understanding of the GHG Protocol itself.

70% – 90% of Emissions Are Hidden in Scope 3

Most African companies are measuring the wrong part of their carbon footprint or not measuring it at all.

For the majority of organisations, Scope 3 emissions account for 70–90% of their total carbon impact.

However, Scope 3, encompassing all indirect emissions across a company's value chain, from the goods it purchases to the products it sells and the investments it holds, remains the most underreported, most poorly understood, and most strategically consequential emissions category in corporate sustainability reporting.

With IFRS S2 now effective in over 140 jurisdictions that explicitly require Scope 3 disclosure alongside Scope 1 and Scope 2, the consequence of this knowledge gap is direct: non-compliant disclosures, misleading carbon footprints, restricted access to capital, and growing legal and reputational exposure.

Three Scopes, Fifteen Categories, One Framework

The GHG Protocol provides a structured, comprehensive architecture for corporate emissions accounting.

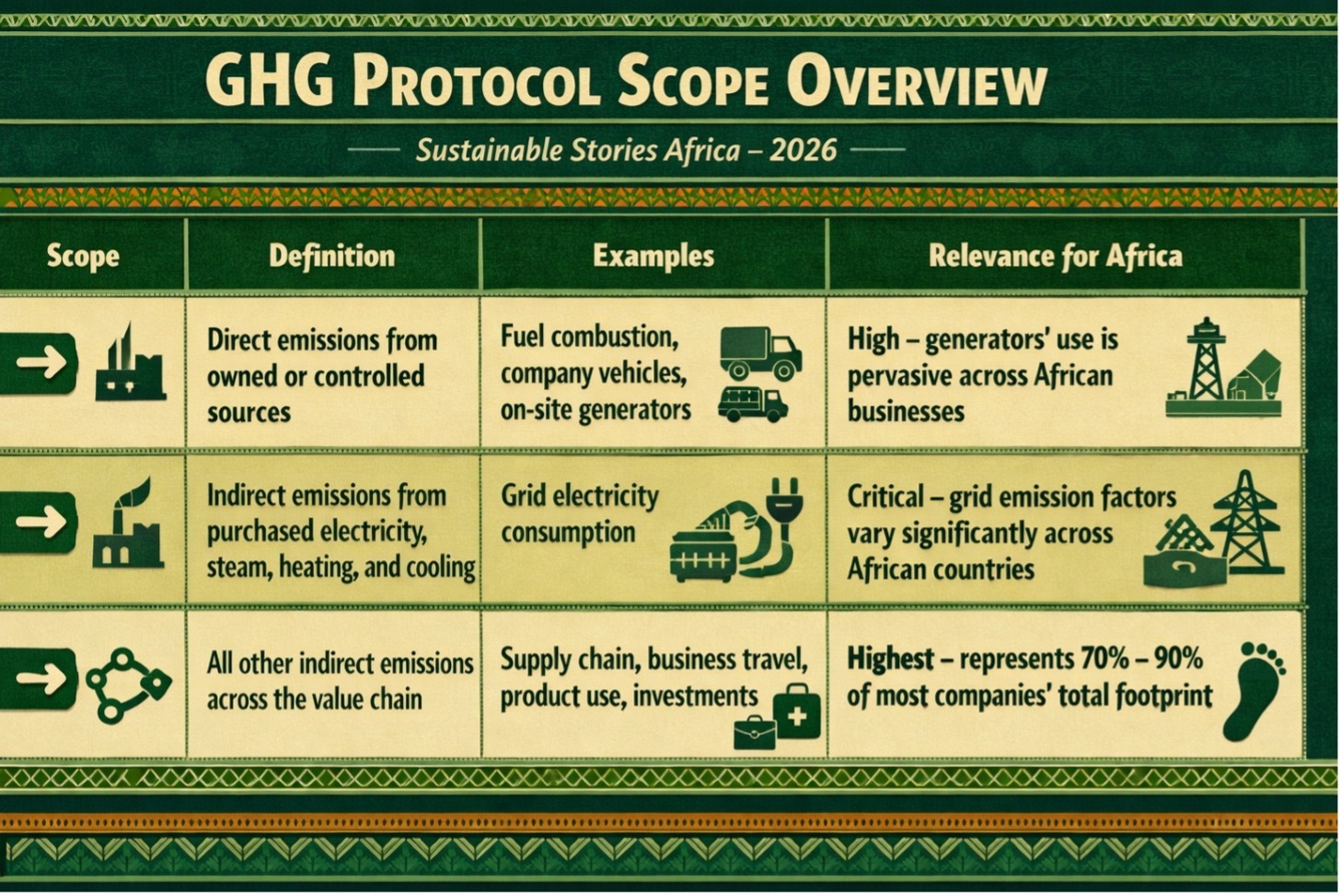

GHG Protocol Scope Overview

| Scope | Definition | Examples | Relevance for Africa |

|---|---|---|---|

| Scope 1 | Direct emissions from owned or controlled sources | Fuel combustion, company vehicles, and on-site generators | High–generators ' use is pervasive across African businesses |

| Scope 2 | Indirect emissions from purchased electricity, steam, heating, and cooling | Grid electricity consumption | Critical – grid emission factors vary significantly across African countries |

| Scope 3 | All other indirect emissions across the value chain | Supply chain, business travel, product use, investments | Highest – represents 70 % – 90% of most companies' total footprint |

Within Scope 3 alone, the GHG Protocol identifies 15 distinct categories spanning upstream and downstream activities. For African companies, several are particularly material:

- Category 1 (Purchased Goods and Services) – critical for manufacturers, retailers, and agribusinesses dependent on often-informal supply chains with no emissions data

- Category 4 (Upstream Transportation – highly relevant in economies with fragmented, multi-modal logistics networks

- Category 11 (Use of Sold Products) – material for energy, technology, and consumer goods companies as Africa's consumer markets expand

- Category 15 (Investments) – the most consequential category for African banks and DFIs, covering financed emissions; now subject to targeted IFRS S2 relief amendments.

Key terms every sustainability professional in Africa must master include:

- CO₂e (the standardised unit comparing greenhouse gases by global warming potential)

- Emission Factor (the coefficient translating activity data into emission quantities)

- Activity Data (the measurable quantity, including fuel consumption, electricity use, distance travelled, from which emissions are calculated).

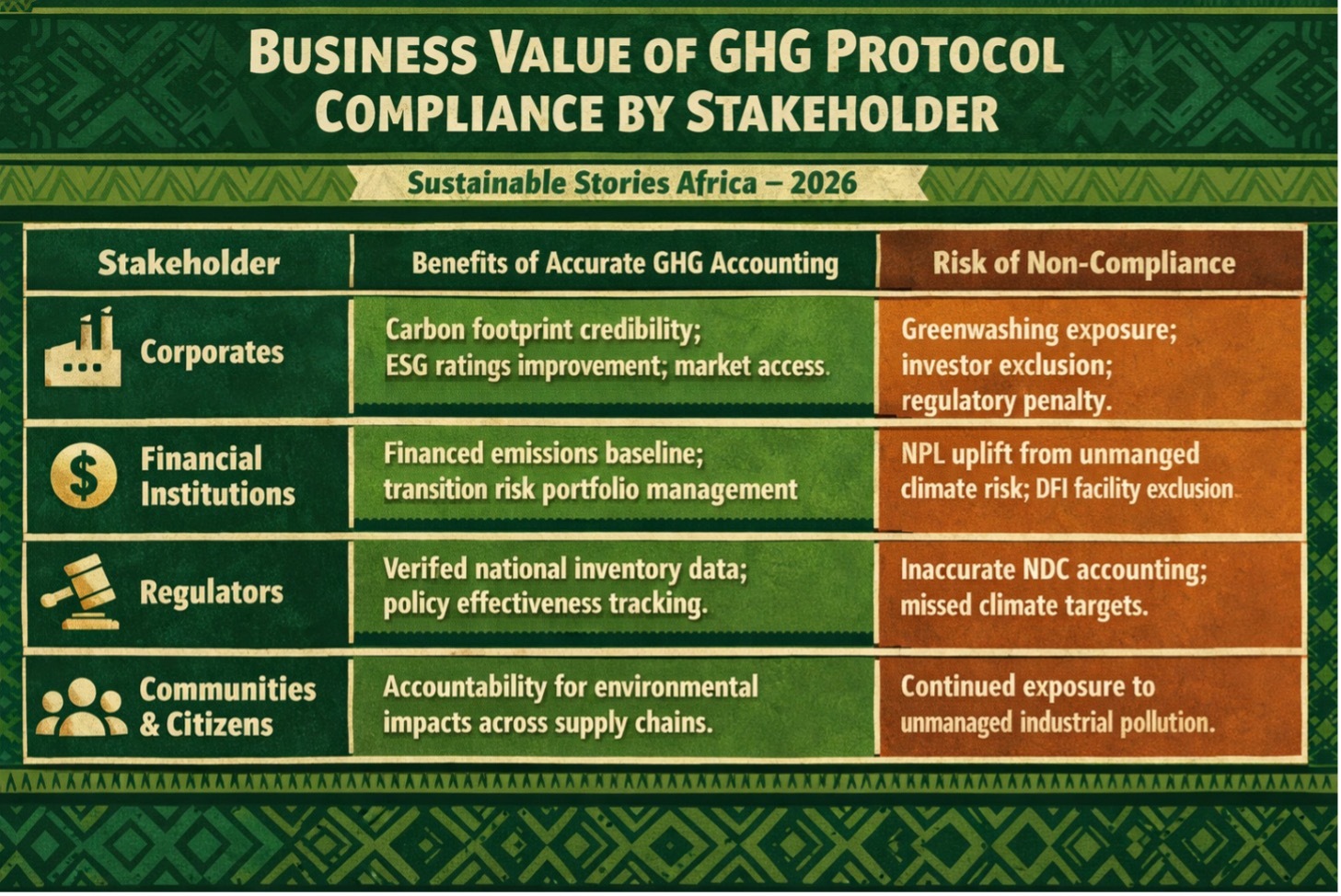

What Accurate GHG Accounting Unlocks

Business Value of GHG Protocol Compliance by Stakeholder

| Stakeholder | Benefits of Accurate GHG Accounting | Risk of Non-Compliance |

|---|---|---|

| Corporates | Carbon footprint credibility; ESG ratings improvement; market access | Greenwashing exposure; investor exclusion; regulatory penalty |

| Financial Institutions | Financed emissions baseline; transition risk portfolio management | NPL uplift from unmanaged climate risk; DFI facility exclusion |

| Regulators | Verified national inventory data; policy effectiveness tracking | Inaccurate NDC accounting; missed climate targets |

| Communities & Citizens | Accountability for environmental impacts across supply chains | Continued exposure to unmanaged industrial pollution |

South Africa's financial sector provides an instructive benchmark. Sanlam's FY2025 Carbon Footprint Report, prepared in compliance with GHG Protocol and ISO 14064, demonstrates that rigorous Scope 1, 2, and 3 accounting builds the credible, auditable emissions baseline that investors, regulators, and rating agencies require.

The same standard is now expected across African markets as IFRS S2 adoption accelerates.

From Understanding to Implementation

The path from conceptual awareness to credible GHG reporting requires deliberate action across three levels:

- Companies should first define their GHG inventory boundary, gather activity data across all three scopes and apply relevant emission factors. For Scope 3, credible supplier and counterparty data are essential, while proxies need improvement in roadmaps.

- Regulators and policymakers must fast-track country-specific electricity emission factors and sector benchmarks, the core inputs for accurate Scope 2 and Scope 3 accounting. Nigeria’s FRC engagement on IFRS S2 matters, but guidance on GHG infrastructure remains essential.

- Capacity builders, financial institutions, and development partners must invest in technical training, tools, and sector guidance to close the 48% to 52% readiness gap that currently separates African listed companies from the ISSB standard their markets are adopting.

Path Forward – Counting Carbon: Closing Africa’s GHG Gap

Africa’s corporate sector cannot reduce emissions it has neither measured nor reported. Closing the GHG accounting gap, from Scope 1 basics to Scope 3 complexity, is essential to credible climate action.

The GHG Protocol sets the framework, while IFRS S2 and the CBN SBP provide the mandate. What businesses need now is technical investment, data infrastructure and sustained leadership commitment.