The voluntary carbon credit market is expanding rapidly, growing at 21.5% annually and projected to reach $2.29 billion in 2026.

However, across Africa, many governments, companies and investors still lack a practical understanding of what carbon credits are, how they are structured, and which types offer the strongest value.

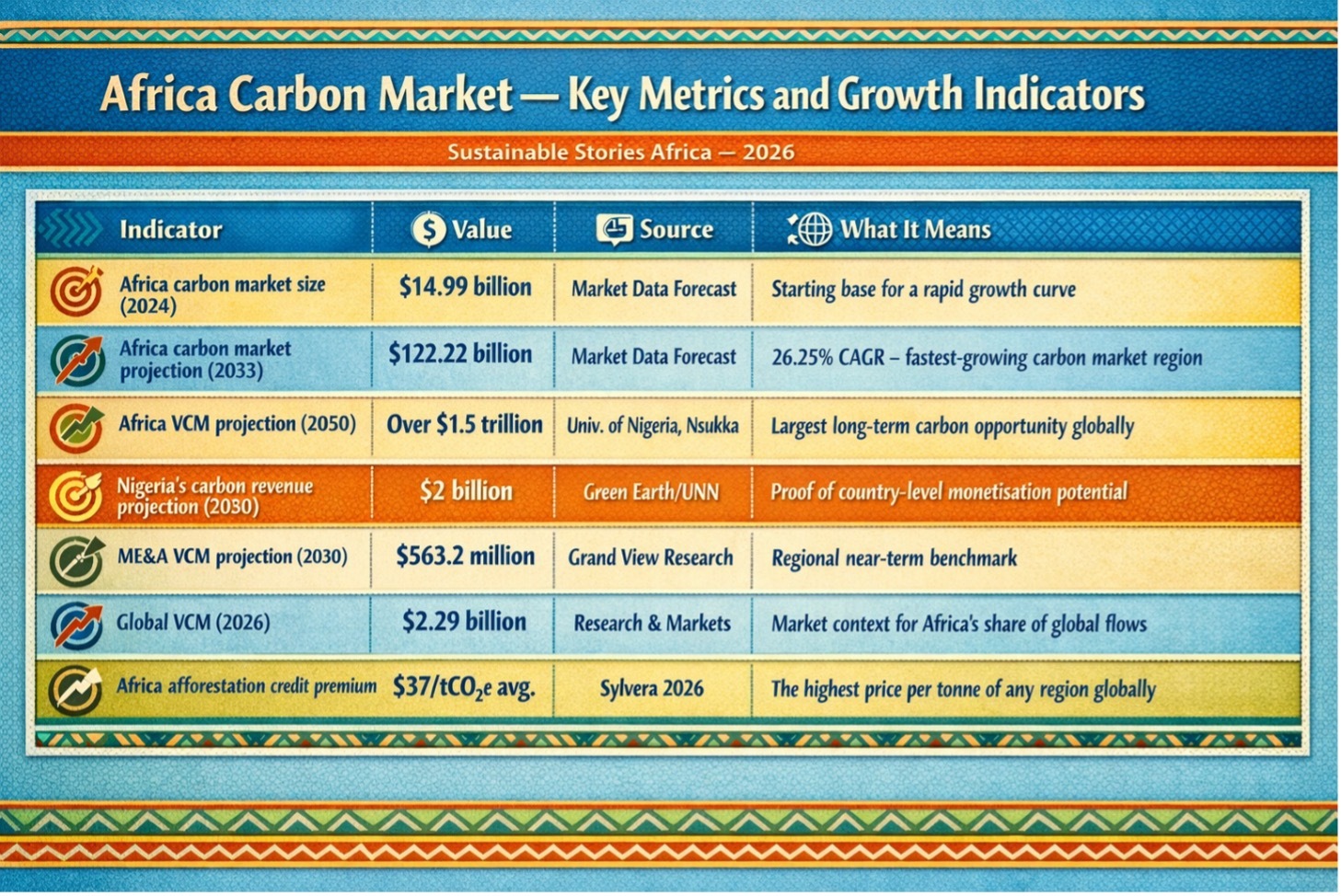

That gap matters, especially as Africa holds the world’s largest untapped carbon sink, with long-term market potential estimated at more than $1.5 trillion by 2050.

Understanding the taxonomy, especially the distinction between nature-based and tech-based credits, is now central to participating effectively in one of the century’s most important green finance markets.

Carbon Credits: Africa's Climate Finance Blueprint

A carbon credit is a tradeable certificate representing the reduction or removal of one tonne of carbon dioxide equivalent (CO₂e).

Bought by companies, governments and financial institutions to offset emissions, these credits generally fall into two main categories: Nature-Based and Tech-Based.

That distinction is strategic, not merely technical. Nature-Based credits rely on ecosystems such as forests, grasslands, and mangroves.

Tech-Based credits come from industrial and engineered solutions, including renewable energy, efficiency improvements and carbon-removal technologies.

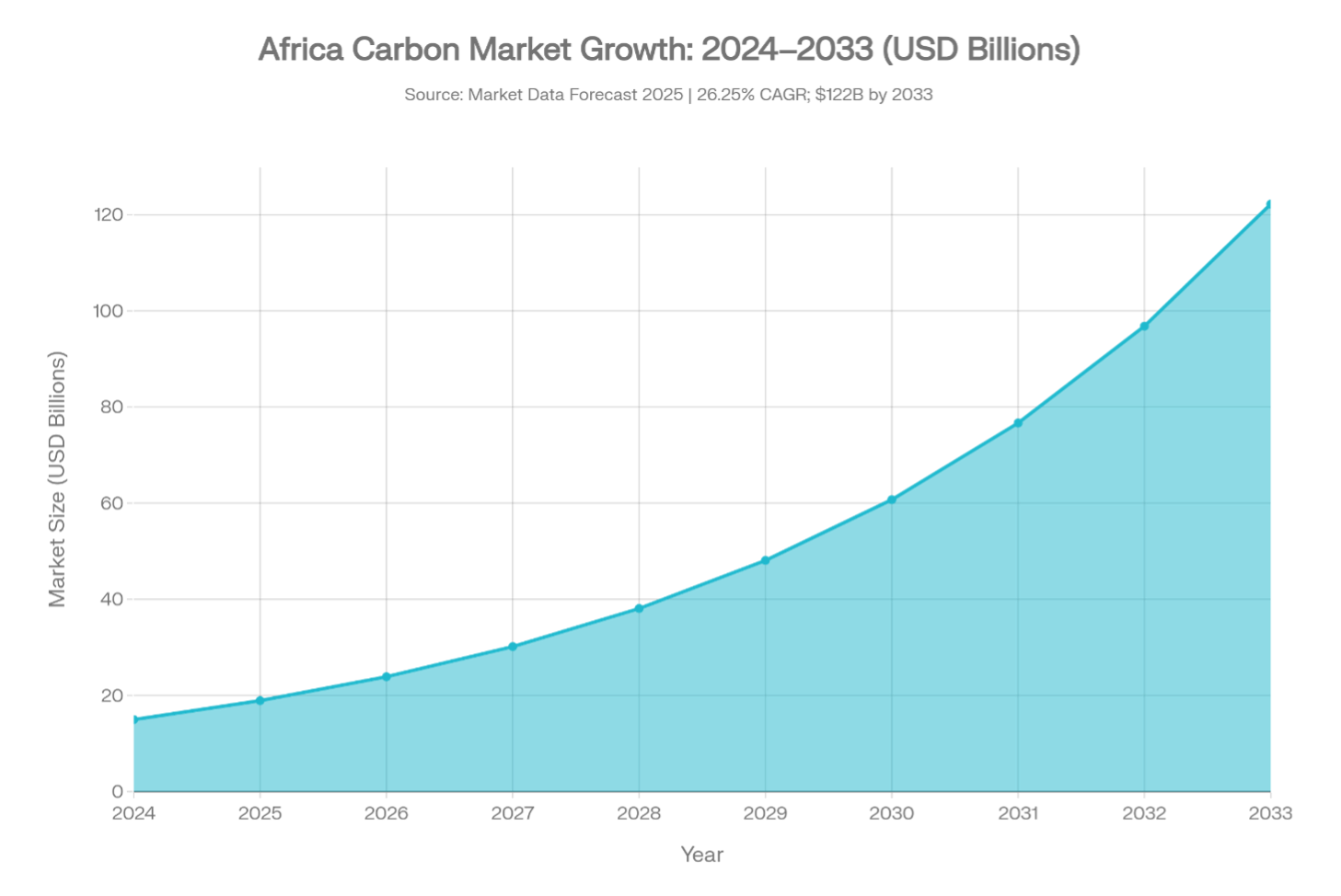

For Africa, understanding that taxonomy is critical, as it shapes opportunities to access the carbon market projected at $122 billion by 2033.

A $1.5 Trillion African Opportunity, Mostly Untapped

Africa’s voluntary carbon market carries extraordinary long-term potential, with projections exceeding $1.5 trillion by 2050.

The continent also holds natural assets capable of producing some of the world’s highest-value carbon credits, with African afforestation projects averaging $37 per tonne of CO₂e, above prices in North America, South America and Asia.

However, Africa still accounts for only a small share of global carbon credit issuance, held back by awareness gaps, regulatory uncertainty and limited technical capacity.

That matters because the market is expanding fast: from $14.99 billion in 2024 to a projected $122.22 billion by 2033.

The Full Taxonomy – Nature-Based and Tech-Based Credits Explained

The carbon credit universe is broader and more nuanced than most stakeholders realise. The infographic maps all major credit types under the two fundamental categories. Here is what each means and why it matters.

Category 1: Nature-Based Credits – Nature-Based credits are generated by projects that protect, restore, or enhance natural carbon sinks. They divide into two sub-families:

- Nature Restoration covers both reduction and removal mechanisms:

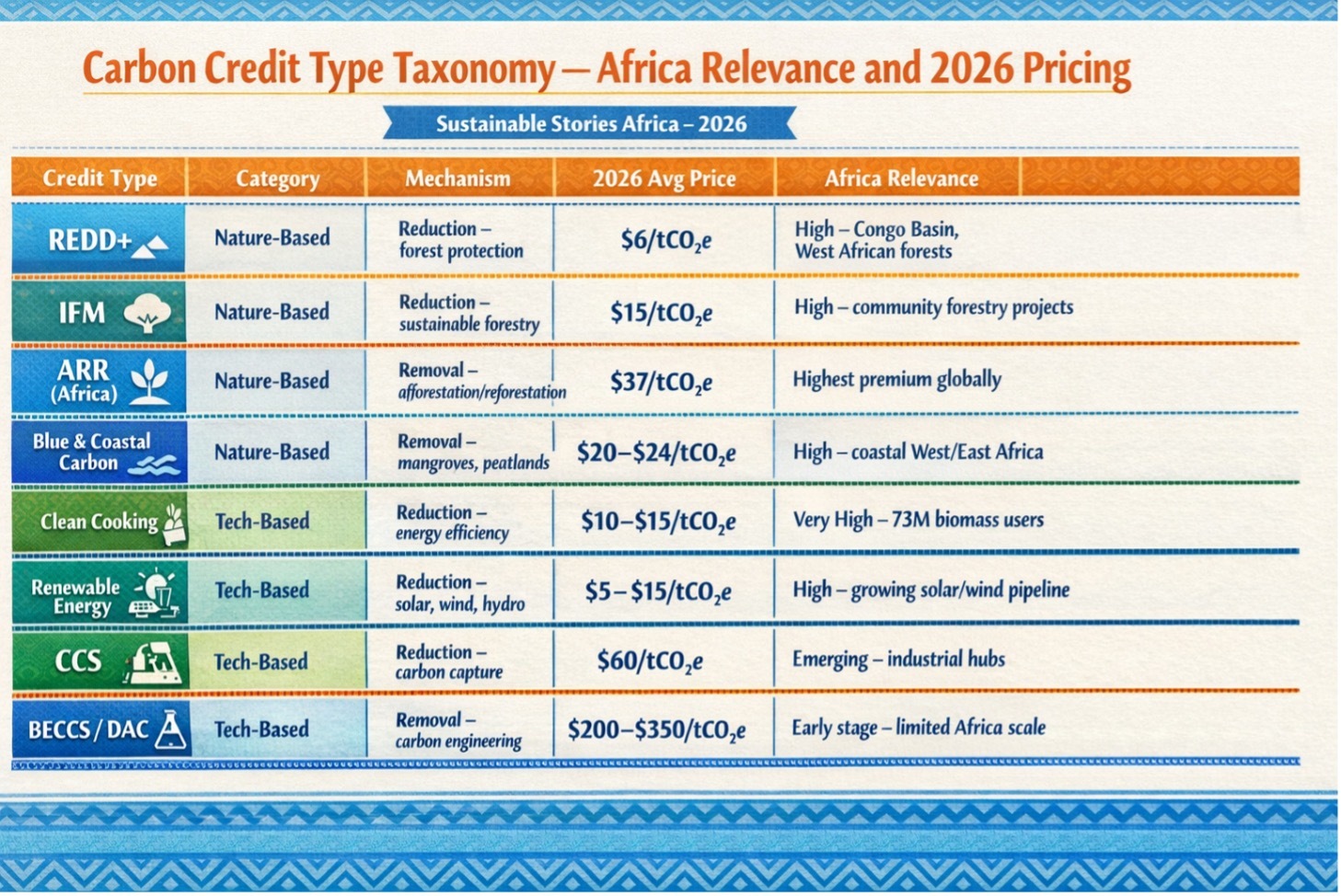

- Reduction: Avoided Conversion of Grasslands and Shrublands (ACoGS), Agricultural Land Management (ALM), and Improved Forest Management (IFM) all prevent carbon-releasing land-use changes. IFM credits currently average $15/tCO₂e globally.

- Removal: Blue and Coastal Carbon (mangroves, seagrasses, salt marshes) and Peatlands actively sequester carbon from the atmosphere. Blue carbon projects are particularly relevant for Nigeria, Ghana, and East African coastal states with significant mangrove coverage.

- REDD+ (Reducing Emissions from Deforestation and Forest Degradation) is Africa's most commercially developed nature-based credit pathway, covering:

- General Deforestation prevention

- High Forest Low Deforestation / Jurisdictional REDD+

- Planned (APD) and Unplanned Deforestation (AUDD) avoidance

REDD+ credits average about $6 per tonne of CO₂e, offering lower prices than afforestation credits but strong volume potential for Africa, especially as 2025 supply constraints widened regional pricing gaps.

Category 2: Tech-Based Credits – Tech-Based credits are generated by industrial and engineering interventions that reduce or remove emissions through technology. They span five sub-categories:

- Non-CO₂ Gases (Reduction): Credits generated by eliminating non-carbon greenhouse gases, methane (CH₄) from landfills and fugitive sources, ozone-depleting substances (CFCs, HFCs, PFCs), and chemical sector emissions. These are high-impact, high-volume credits particularly relevant for Nigeria's gas flaring crisis and South Africa's industrial emissions profile.

- Energy Efficiency (Reduction): Clean cooking, efficient distribution networks, efficient transport systems, and energy demand reduction. Clean cooking credits are directly relevant to the 73 million West Africans still relying on biomass fuels, each clean cookstove project simultaneously generates carbon credits and addresses SDG 7 and SDG 3.

- Fuel Switch (Reduction): Biofuel, hydrogen and hybrid systems, and general fuel switching projects, all generating tradeable credits by replacing fossil fuels with lower-emission alternatives. Biofuel credits are particularly bankable in Africa's agricultural economies.

- Renewable Energy (Reduction): Credits from solar, wind, hydro, geothermal, and organic waste-to-energy projects. Solar and wind dominate Africa's renewable pipeline — and each verified megawatt-hour of clean electricity generated translates directly into carbon credit revenue for project developers.

- Non-CO₂ / Carbon Engineering (Reduction & Removal):

- Carbon Capture and Storage (CCS) generates reduction credits, with an average price around $60/tCO₂e.

- Carbon-engineering removal credits sit at the high-value frontier of the market, with BECCS trading at $200–$400/tCO₂e and DAC reaching as high as $350/tCO₂e, though scale remains limited.

What Getting This Right Could Mean for Africa

The case for Africa mastering carbon credit taxonomy is not only environmental, but also financial and developmental.

A community-managed afforestation project in Cross River State, for example, could generate significant annual revenue while supporting local livelihoods and restoring degraded land.

Scaled effectively, such models could become economically transformative, with Nigeria alone projected to earn $2 billion from carbon markets by 2030.

Adding tech-based projects such as clean cookstoves, solar mini-grids and biogas systems would deepen that opportunity.

These projects can cut emissions, improve livelihoods and generate high-integrity credits for global buyers. Without that capability, Africa risks leaving major climate value unrealised while bearing the heaviest climate costs.

What Every African Stakeholder Must Do Now

The market is growing, but it will not wait. Carbon credits have a quality hierarchy, a price hierarchy, and an integrity hierarchy, and Africa's players must navigate all three with sophistication. Here is what must happen:

- Governments and regulators – African governments must accelerate the implementation of a national carbon market to align with Article 6, clearly defining standards, eligible credits and approval processes, or risk losing the value of natural assets to discounted external deals.

- Corporations with ESG commitments and net-zero targets operating in Africa should begin auditing their emissions against both nature-based and tech-based credit opportunities within their supply chains to identify whether offset purchasing or credit generation is the more strategic play.

- Development Finance Institutions and green financiers should prioritise blended finance vehicles that de-risk nature-based credit projects in Africa, particularly ARR and Blue Carbon, where the price premium is highest, but up-front development costs deter smaller project developers.

- Community organisations and NGOs working in forested and coastal landscapes must engage with carbon market standards bodies, Verra, Gold Standard, and Plan Vivo, to ensure communities retain carbon rights and revenue, not just conservation obligations without compensation.

- ESG reporters and sustainability teams must include carbon credit strategies, not just offset purchases, in their GRI and IFRS Sustainability disclosures, distinguishing clearly between reduction credits (avoiding future emissions) and removal credits (reversing past emissions) to maintain credibility with investors and regulators.

Path Forward – Nature and Technology, Africa's Twin Credit Engines

Africa must move from carbon market awareness to market strategy by building the regulatory frameworks, technical capacity and project pipelines needed to monetise both nature-based and tech-based opportunities.

That includes developing REDD+, clean cooking and renewable energy projects under recognised international standards, with strong benefit-sharing systems that keep value in-country.

Understanding carbon credit taxonomy is the essential first step. Policymakers, investors and ESG practitioners must recognise that REDD+, clean cooking and DAC credits are fundamentally different instruments, with distinct pricing, verification pathways, co-benefits and durability.