Nigeria's oil and gas sector sits at the intersection of the world's most urgent ESG challenge and its greatest ESG opportunity.

A comprehensive two-part beginner's guide, authored by Senior Sustainability Advisor Chika Onyekwere, delivers the sector's most accessible and data-rich introduction to ESG foundations, global reporting standards, and what compliance actually demands.

The guide arrives as global capital markets, EU border regulations, and domestic regulators collectively close the door to companies that still treat sustainability as optional.

Africa's O&G ESG Reckoning

The energy sector sits at the centre of the ESG debate, not at its margins. Oil and gas operations account for a large share of global carbon emissions across Scopes 1, 2 and 3, making production, flaring and infrastructure decisions increasingly material to disclosure, regulation and finance.

In Nigeria, Africa’s largest oil producer, that pressure is intensifying as global ESG standards, investor scrutiny, community expectations and regulatory convergence begin to reshape the sector.

That shift now has a practical guide. Chika Onyekwere, Senior Sustainability Advisor and ESG Strategy Lead, has published a two-part Oil and Gas ESG: A Beginner’s Guide, covering ESG foundations, materiality, standards and frameworks.

Released between February and March 2026, the guides are designed to help professionals across Nigeria’s oil and gas value chain build fluency in ESG requirements through a framework that is both globally benchmarked and locally grounded.

The stakes are no longer theoretical. As mandatory reporting expands globally and Nigerian regulators align more closely with international standards, ESG non-compliance is becoming a financial risk, rather than merely a reputational one.

The 42% Problem and the Capital Ultimatum

The numbers are increasingly hard for Nigeria’s oil and gas sector to ignore. The industry accounts for 42% of global emissions, while gas flaring in Nigeria still represents 7% of gas produced, a sharp improvement from 50% in the 2000s.

However, still a material ESG liability. Methane leakage across extraction, processing and transport remains one of the sector’s most potent and closely scrutinised climate risks.

The financial case is just as clear. Strong ESG performers can access capital at up to 50% lower cost, while weak ESG performance is linked to an estimated $25 billion in annual incident costs globally.

With $100 trillion in assets under management now demanding stronger ESG disclosure, reporting has become a financing requirement, rather than a voluntary gesture.

“Companies that understand and act on ESG are not just managing risk; they are building the resilience to lead through Africa’s energy transition.” – Chika Onyekwere, Senior Sustainability Advisor, ESG Strategy

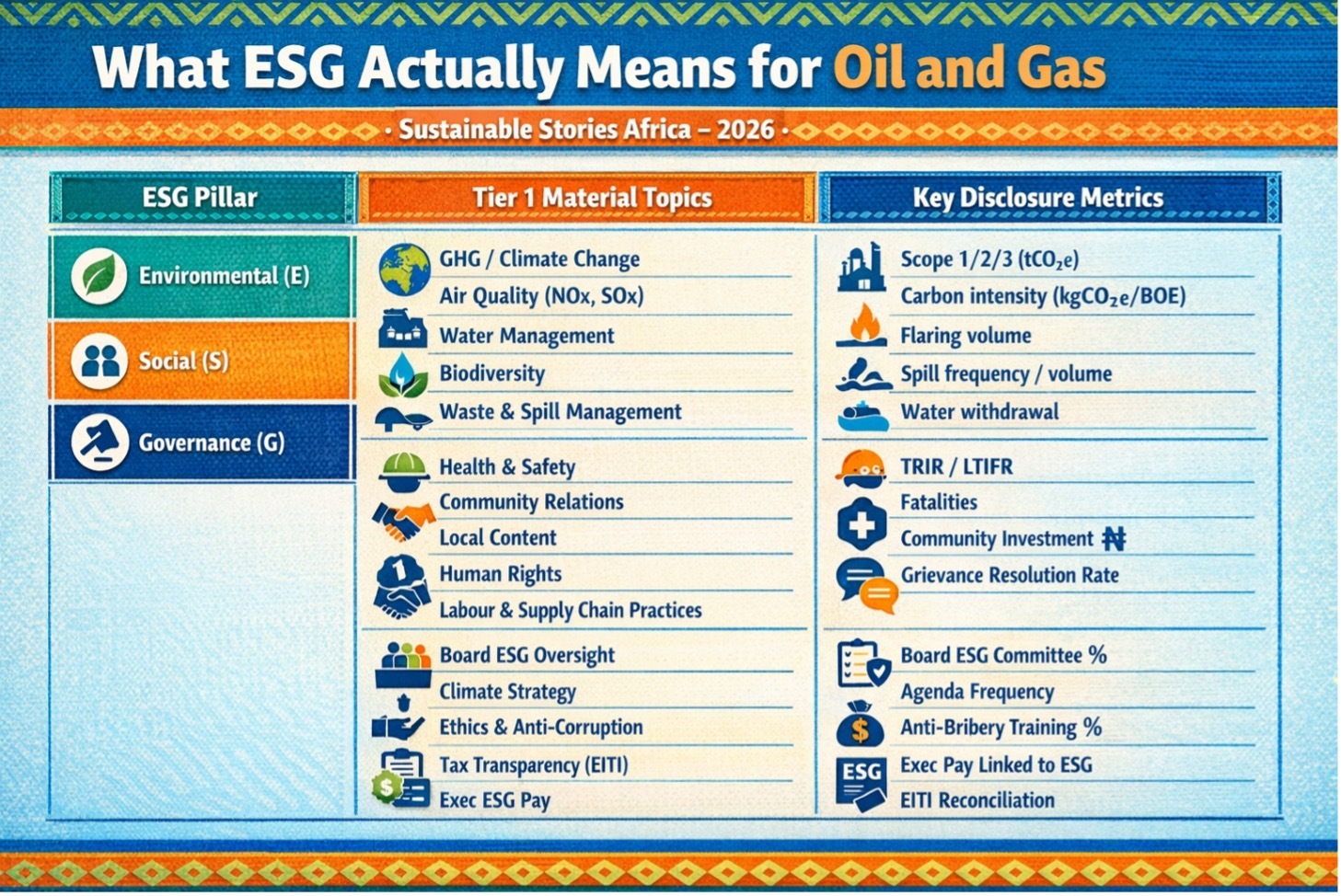

What ESG Actually Means for Oil and Gas

Part 1 of the guide brings operational clarity to ESG for Nigeria’s oil and gas sector, treating it not as a vague acronym but as a framework built around Environmental, Social and Governance pillars, each with material topics and measurable KPIs that investors, auditors and regulators now track closely.

It also shows why ESG is unusually complex in oil and gas. Most emissions are embedded in Scope 3, with 80% – 90% coming from end use rather than extraction.

Long asset life cycles mean much of today’s infrastructure was not built for current ESG expectations, making retrofitting costly.

At the same time, companies face a transparency challenge: disclosing enough to satisfy markets without increasing legal risk.

The guide also underscores the financial importance of a social licence to operate, especially in the Niger Delta, where weak community relations can quickly translate into protests, shutdowns, sabotage and lost production.

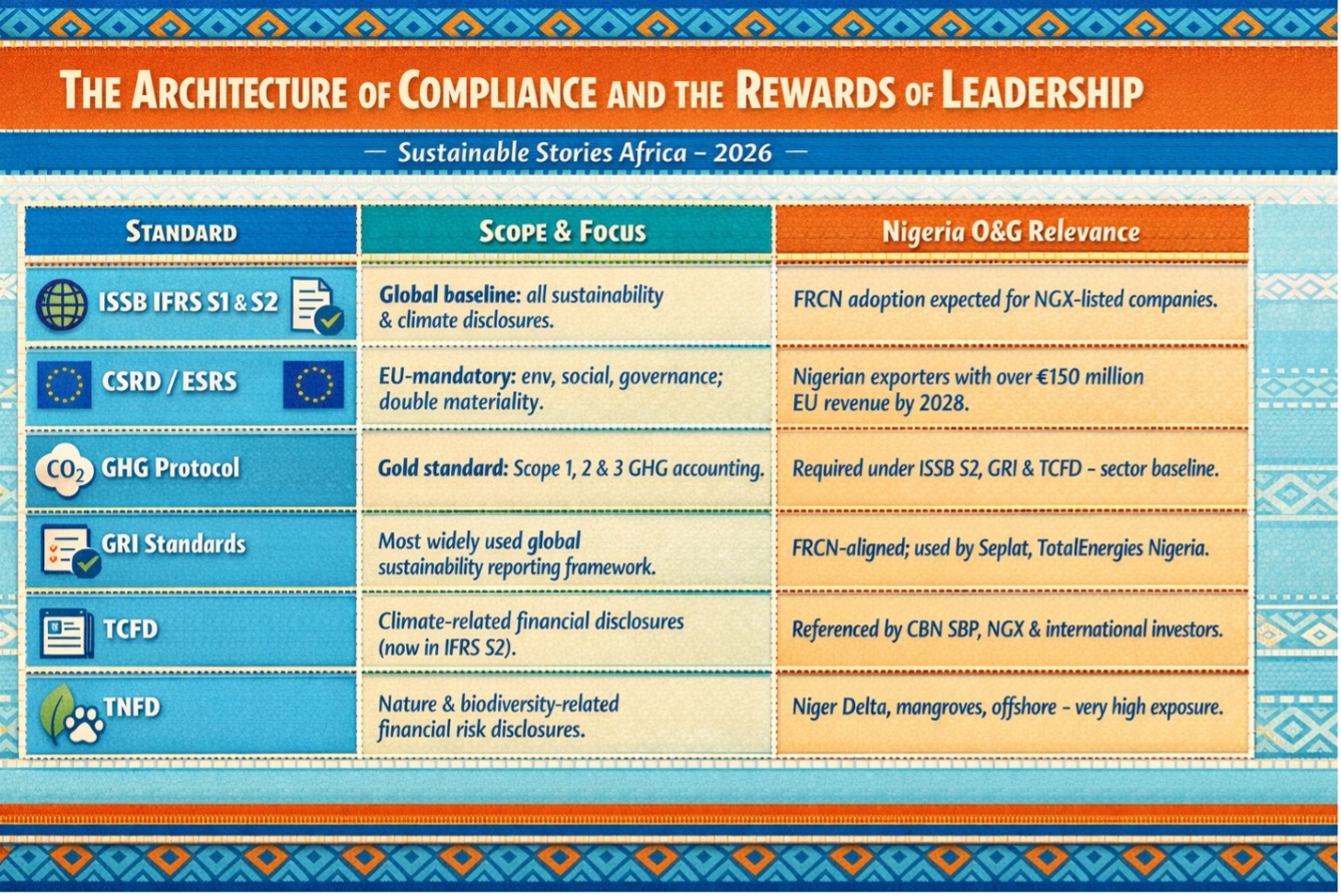

The Architecture of Compliance and the Rewards of Leadership

Part 2 of the guide maps the global standards architecture Nigerian oil and gas companies must now navigate, showing that at least six major frameworks already shape how ESG performance is disclosed and assessed across the sector.

Its treatment of the GHG Protocol is especially important. Under IFRS S2, Scope 3 Category 11, emissions released when customers burn the oil and gas a company sells, are mandatory for most operators and often represent 85% – 95% of total emissions. For Nigerian producers, that makes end-use emissions too large and too material to omit from any credible ESG report.

The guide argues that companies that master this framework early can build a lasting competitive advantage.

As global oil demand weakens and carbon prices rise, early movers into gas, carbon capture and blue hydrogen will be better placed to protect earnings, lower financing costs and preserve their social licence to operate.

Four Phases Every Nigerian O&G Company Must Initiate

The guide closes Part 2 with a phase-by-phase audit checklist that translates global standards into operational action. Every Nigerian O&G company should initiate four parallel workstreams without delay:

- Governance Audit – Name the board committee responsible for ESG oversight, verify meeting frequency (quarterly minimum), document board members' ESG expertise, and confirm that executive compensation contracts formally link pay to ESG KPIs. Auditors will check board minutes; the absence of documented climate discussion is a red flag that triggers immediate scrutiny.

- GHG Emissions Inventory – Complete Scope 1 across all five source categories, such as stationary combustion, flaring, fugitive emissions, vented emissions, and mobile combustion. Report Scope 2 using both location-based (Nigeria grid EF: 0.587 tCO₂e/MWh) and market-based methods. Prioritise Scope 3 Category 11 above all else; its omission is the single most common gap in Nigerian O&G reports.

- Scenario Analysis: Conduct resilience testing against at least two climate pathways, the IEA Net Zero 2050 (1.5°C) and IEA STEPS (2.7°C+) scenarios, and quantify the financial impact of each on revenues, costs, assets, and liabilities. Scenario analysis, absent or superficial, is a direct red flag for IFRS S2 and TCFD auditors.

- Nature & Community Risk Mapping – Apply the TNFD's LEAP framework, Locate, Evaluate, Assess, Prepare, to map operations against Nigeria's biodiversity-sensitive zones, including Niger Delta wetlands, mangrove systems, and offshore marine habitats. Community grievance data, GMOU implementation coverage, and oil spill incident volumes should all be disclosed under GRI 413 and linked to financial risk quantification.

Regulators, such as NUPRC, FRCN, CBN, NGX, must urgently publish binding domestic timelines for ISSB adoption, with clear transition provisions for smaller operators and mandatory assurance requirements for Tier 1 companies.

Path Forward – Nigeria’s Oil Sector ESG Test Deepens

Nigeria’s oil and gas sector cannot lead Africa’s energy transition without mastering ESG disclosure. ISSB, GRI, TCFD, TNFD and the GHG Protocol already provide the framework, while Chika Onyekwere’s guides translate it into practical direction for sector professionals.

The path ahead is clear: govern with accountability, measure what matters, disclose with integrity and build community trust. Companies that move early will do more than comply. They will strengthen competitiveness in a decarbonising global market.