Nigeria’s push to adopt IFRS Sustainability Disclosure Standards is no longer just a policy ambition. It is becoming a practical test of data systems, assurance capacity and regulatory coordination.

An FRC readiness assessment suggests progress is real, but so are the gaps.

The central question now is whether institutions can build credibility fast enough to align with the timetable.

Readiness now matters more

Nigeria has moved beyond asking whether global sustainability disclosure standards matter.

The harder question is whether the institutions expected to implement them are prepared to do so.

In Nigeria’s FRC 17-Document Readiness Assessment, author Chika Onyekwere examines the country's readiness for the phased adoption of IFRS Sustainability Disclosure Standards S1 and S2.

The review draws on work conducted by the Adoption Readiness Working Group (ARWG) under the Financial Reporting Council of Nigeria to assess 17 documents spanning global ESG frameworks and Nigerian regulatory instruments.

That makes the paper more than a technical summary. It is effectively a stress test of Nigeria’s transition to sustainability reporting.

For African markets watching how to align local realities with global disclosure rules, the stakes are significant: investor confidence, regulatory trust, and whether sustainability reporting becomes decision-useful or merely performative.

Nigeria has a roadmap, but readiness gaps are still large

The headline message from the assessment is clear. Nigeria has a roadmap for IFRS sustainability adoption, but the institutions expected to carry the weight of compliance remain unevenly prepared.

The report identifies several “institutions of concern” on page 3: Public Interest Entities (PIEs) such as listed companies, banks, insurers and pension funds; core regulators including SEC, NGX, CBN, NAICOM and PENCOM; large corporates in sectors such as oil and gas, manufacturing and telecoms; and SMEs, which are specifically flagged for capacity gaps in ESG reporting readiness.

The data on page 4 sharpens the urgency.

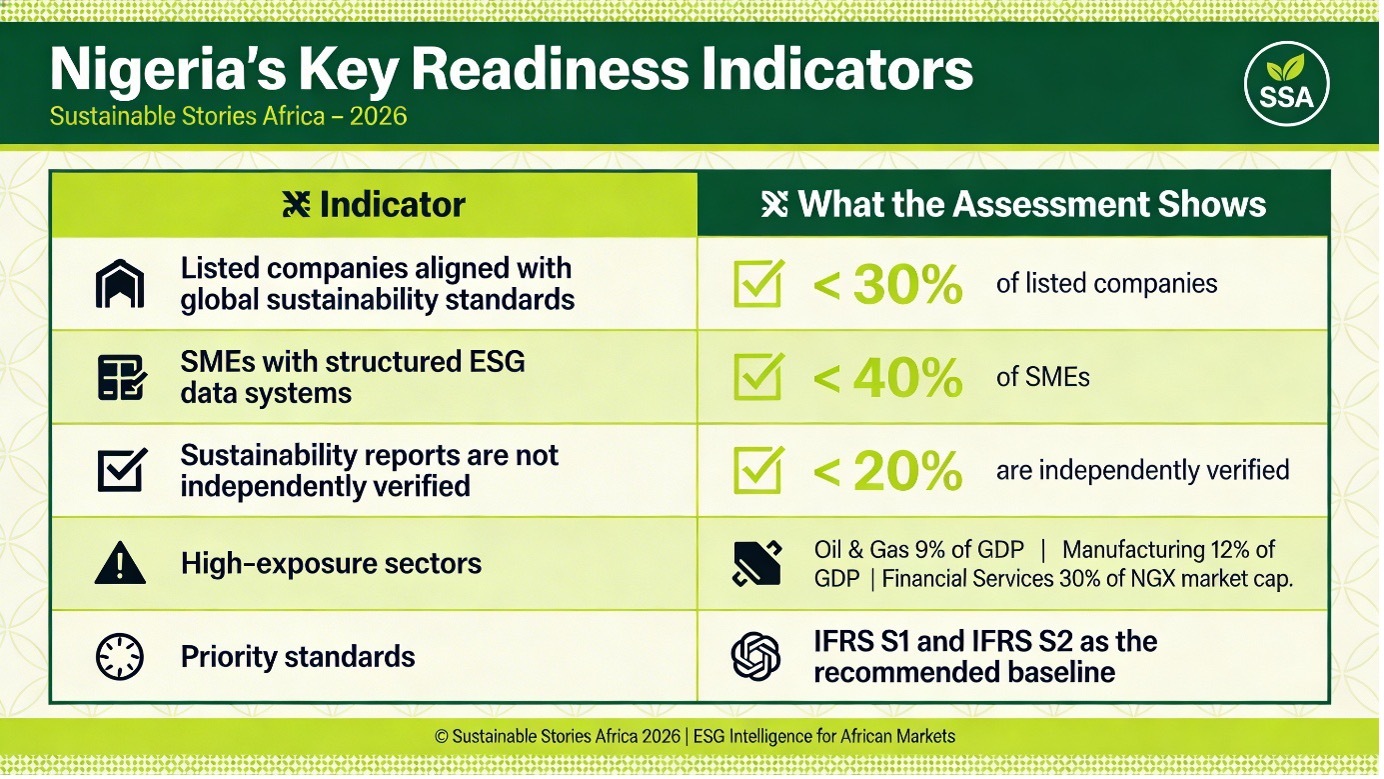

- Fewer than 30% of Nigerian listed companies publish sustainability reports aligned with global standards.

- More than 60% of SMEs lack structured ESG data collection systems.

- Fewer than 20% of sustainability reports undergo independent verification.

Meanwhile, the sectors most exposed to transition and disclosure pressure are far from marginal:

- Oil and gas account for roughly 9% of GDP

- Manufacturing accounts for about 12% of GDP

- Financial services account for around 30% of NGX market capitalisation.

That is why the readiness question matters now. IFRS S1 and S2 are not just new templates.

They require systems for governance, strategy, risk management, metrics and targets. Without credible data and assurance, the transition risks exposing a wide gap between disclosure expectations and institutional capacity.

What the 17 – document review shows

The assessment is important because it does not approach readiness from a narrow perspective. It links global standards to domestic regulation and policy intention to execution risk.

On page 5, the document summary shows the breadth of the review. It covers the rationale for IFRS adoption, international frameworks such as:

- IFRS S1 and S2, GRI, SASB, TCFD and TNFD, and local rules including CAMA, SEC requirements, NGX listing rules, CBN guidelines and NAICOM directives.

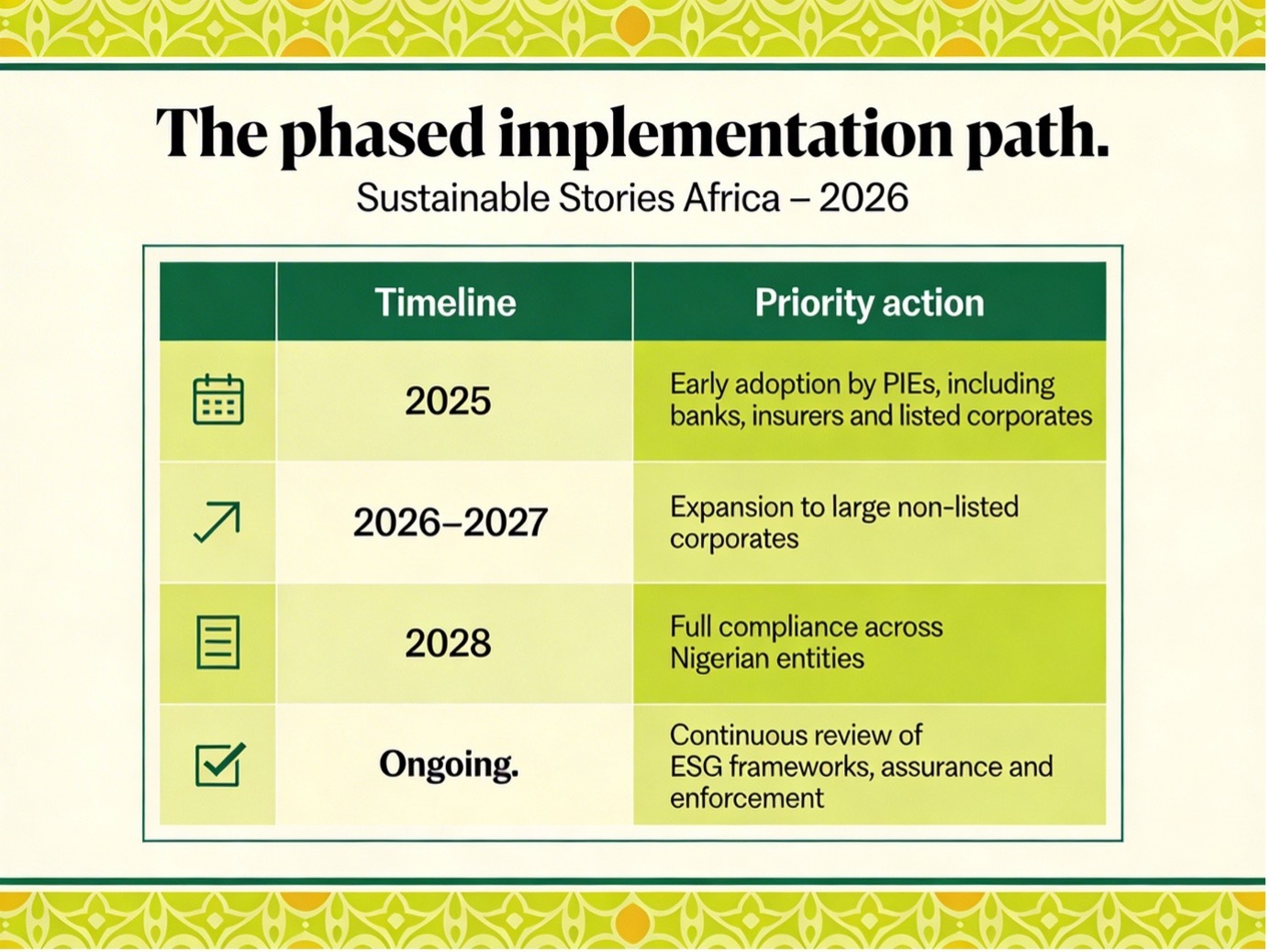

- It recommends IFRS S1 as the baseline for general sustainability disclosures and IFRS S2 for climate-related disclosures, while proposing a phased roadmap from 2025 to 2028, with PIEs first and SMEs later.

That sequencing reflects a practical truth. Nigerian institutions are not starting from the same point.

Banks and listed firms may be more visible and better resourced, but even among them, alignment and assurance are still limited.

SMEs face a more basic challenge: many don’t have structured ESG data systems.

The report also outlines the core frictions slowing progress. On page 6, it lists:

- Limited technical expertise in ESG reporting, high compliance costs for SMEs, weak enforcement mechanisms, fragmented data sources across institutions, and low investor awareness of sustainability disclosures.

That combination matters because it shows the challenge is not merely one of corporate willingness. It is structural.

The visual roadmap on page 8 adds another important layer.

- It shows early adoption by PIEs in 2025, expansion to large non-listed corporates in 2026–2027, and full compliance across Nigerian entities by 2028, followed by continuous review of ESG frameworks, assurance and enforcement.

This is ambitious. It also means the window for preparation is short.

What successful adoption could unlock

The upside of getting this right is substantial.

A stronger sustainability disclosure regime could boost investor confidence, especially for Nigerian firms seeking international capital or operating in sectors under growing scrutiny of transition.

It would also create a shared reporting language for regulators, issuers and financial institutions, making markets easier to understand, compare and trust.

There is also a governance dividend. Firms that build IFRS-style reporting systems are likely to make better strategic decisions, with stronger sustainability data informing risk management, capital allocation, supply-chain planning and long-term resilience.

Regulators gain better oversight, while citizens and communities gain clearer visibility into how risks are managed.

Nigeria’s shift could also help define what credible sustainability adoption looks like across African markets.

What needs to be done next

The report is especially valuable because it does not stop at diagnosis. On page 7, it sets out six areas of action:

- Capacity building

- Phased implementation

- Data infrastructure

- Assurance framework

- Advocacy and communication

- Monitoring and enforcement.

That agenda deserves to be read as a sequence, rather than a checklist.

- First, training is essential, not optional. Preparers, auditors and regulators all need stronger technical capability.

- Second, transitional reliefs for SMEs and non-PIEs are necessary if the adoption process is to remain proportionate.

- Third, Nigeria needs a centralised ESG data repository or equivalent infrastructure to reduce fragmentation and improve consistency.

- Fourth, the adoption of ISSA-based assurance standards matters because disclosure without verification will struggle to earn trust.

- Fifth, the report calls for awareness campaigns across industries to raise understanding.

- Finally, it argues for a stronger role for FRC, SEC and NGX in enforcement.

The executive summary on page 9 captures the logic well: Nigeria’s adoption effort will succeed only if data infrastructure, assurance mechanisms, advocacy and monitoring move together.

In other words, disclosure reform is not just about standards. It is about the systems that make standards real.

Path Forward – Build systems before deadlines

Nigeria’s IFRS sustainability push now needs less rhetoric and more operating capacity.

The priority is to build data systems, assurance pathways and regulatory coordination before deadlines begin to bite.

The opportunity is significant: better investor trust, stronger market credibility and more decision-useful sustainability reporting.

However, those gains will depend on whether readiness catches up with the roadmap.