A stronger global framework for financing sustainable development has arrived at a difficult time.

Debt burdens are heavier, aid is falling, project finance is weakening, and many poorer countries remain priced out of affordable capital.

The question is no longer whether the world recognises the problem. It is whether the Sevilla Commitment can overturn reform, risk sharing and country-led execution into measurable financing relief.

The squeeze is now systemic

The 2026 Financing for Sustainable Development Report comes with a blunt diagnosis. Financing the Sustainable Development Goals is becoming harder, not easier, for many developing countries, as high borrowing costs, weaker aid flows, trade tensions, and fragmented capital markets tighten the space for investment.

The report was prepared by the Inter-agency Task Force on Financing for Development following the fourth International Conference on Financing for Development in Sevilla in mid-2025.

Its political counterweight is the Sevilla Commitment, described as a renewed global framework for financing sustainable development.

The agreement contains 280 actions across the financing architecture and is backed by 130 voluntary initiatives under the Sevilla Platform for Action, aimed at getting implementation started quickly.

For African and other emerging markets, the stakes are immediate. Financing conditions are worsening at the same time that countries need more investment in infrastructure, health, education, climate resilience, industrial capability and data systems.

The lived reality is that development ambition now runs into the hard math of debt service, capital costs and falling concessional support.

Rising Debt Costs Deepen Development Squeeze

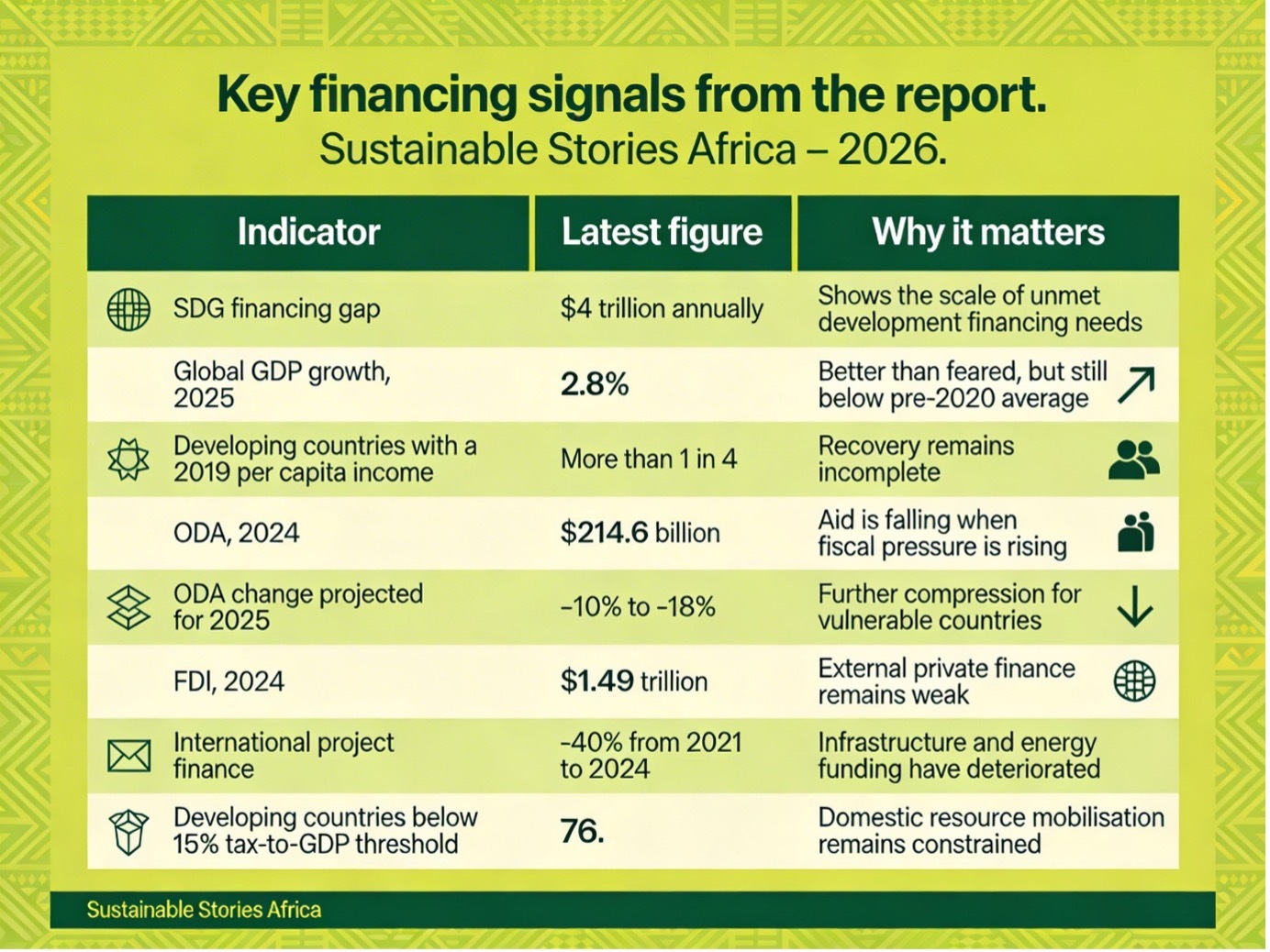

The sharpest number in the report is not the $4 trillion annual SDG financing gap, large as that is. It is the way that pressure is now converging on poorer countries from multiple directions at once.

The report says debt service on external debt reached 20-year highs in 2024 in developing countries and small island developing States, exceeding 20% of government revenue in 14 developing countries.

At the same time, average coupon rates on hard-currency bonds for least developed and other low-income countries rose to 8.4% in 2025 from 6.1% in 2024.

That means sustainable development is increasingly being financed in an environment where the cost of money itself is punitive.

Add in falling official development assistance, weak investment flows and renewed trade strain, and the report’s core message becomes clear: the financing problem is no longer one issue. It is a system-wide constraint.

Financing Strain Deepens Across Developing Economies

The report describes a global economy that performed slightly better than expected in 2025, with growth estimated at 2.8%. However, that remains below the 3.2% average recorded between 2010 and 2019, and more than one in four developing countries still have per capita incomes below 2019 levels.

That leaves a fragile starting point for financing recovery, let alone the deeper structural transformation many economies still need.

Aid is no longer providing the cushion it once did. Official development assistance fell 6% in 2024 to $214.6 billion and was projected to decline by a further 10% to 18% in 2025.

Least developed countries face the sharpest exposure, with bilateral ODA to LDCs expected to drop by another 13% to 25% after already declining 3% in 2024.

Bilateral ODA accounts for approximately 15% of government revenue in LDCs on average; these reductions carry direct consequences for state capacity and development delivery.

Private finance is also failing to close the gap. Foreign direct investment, excluding conduit flows, fell 11% to $1.49 trillion in 2024, marking a second consecutive annual decline.

International project finance, a major source of infrastructure and energy funding, fell 40% between 2021 and 2024 and weakened further in the first half of 2025.

Domestic resource mobilisation remains limited, with developing-country tax revenue rising only from 12% to 14% of GDP between 2000 and 2022, leaving 76 countries below the 15% Sevilla threshold.

The Sevilla Commitment is presented as the institutional response.

It includes 280 actions aimed at improving the quality of financing, strengthening national enabling environments, expanding transparency, supporting science and technology, and building technical capacity.

Its broader message is that development finance now depends on aligning domestic and international, public and private capital around impact, resilience, cooperation and workable multilateralism.

Development Finance Must Deliver Better Impact Top of Form

What is encouraging in the report is that it does not reduce the solution to more leverage alone.

The report argues for a shift in the quality and quantity of financing.

Blended finance grew from $32 billion in 2015 to $75 billion in 2024, but the gains have been uneven.

Mobilised volumes were four times higher in middle-income countries than in LDCs, LLDCs and SIDS combined.

More than three-quarters of mobilised private finance flowed to commercially attractive sectors.

The report therefore argues that success should be judged not only by leverage ratios, but also by sustainable development impact per public dollar.

That matters for African markets. The report suggests that financing should be assessed based on whether it reaches productive sectors, resilient infrastructure, local financial systems, value addition, digital readiness and climate adaptation.

It also backs stronger local banking systems, national development banks, cooperative finance, pass-through lending and local-currency funding.

The report’s emphasis on resilience is another strong signal. Instruments, including pause clauses, climate-resilient debt clauses and stronger safety nets, point to a development-finance model built not just to mobilise capital, but to protect impact when shocks hit.

Sevilla Pushes Finance Reform Beyond Leverage

The article’s policy agenda is demanding but clear.

- Governments need to strengthen tax systems, improve the quality of public finance, and align fiscal and private-sector policy with sustainable development priorities.

- International institutions need to lower borrowing costs, improve debt treatment, expand risk-sharing, and do more to support domestic resource mobilisation.

- Development actors also need to move beyond leverage as the main measure of success and focus more directly on development impact, especially in vulnerable countries.

The report also stresses the importance of data systems, linking stronger impact, accountability, and interoperability to better national statistical capacity.

The Sevilla Platform for Action offers an early implementation channel. It launched 130 initiatives involving more than 240 lead entities, and early updates suggest momentum.

The real test, however, is whether that progress delivers cheaper capital, more resilient financing, and stronger country-led execution.

Path Forward – Sevilla’s Next Test Is Practical Delivery

Sevilla has provided a framework, but not yet relief. The next phase depends on whether reforms can reduce borrowing costs, protect fiscal space, direct more finance toward impact and rebuild trust in multilateral cooperation.

For African and other developing economies, the priority is practical: cheaper capital, stronger domestic systems, more resilient instruments and implementation that follows national priorities rather than donor fashion.

That is where financing for sustainable development becomes real.