Green finance is not being held back only by a shortage of money. It is being slowed by weak pipelines, policy friction and projects that still sit outside acceptable risk-return thresholds.

The latest evidence suggests the transition will be won not just by setting targets, but by building the market conditions that allow private capital to move from interest to deployment.

Capital needs conditions, not slogans alone

The latest edition of Green Finance Quarterly makes a blunt point: capital does not deploy based on targets or frameworks alone.

In its March 2026 issue, the Green Finance Institute argues that institutional investors are willing to engage; however, money flows only when risks are understood, returns are credible, and policy, finance and delivery are aligned to create investable opportunities.

That distinction matters for African markets. Across the continent, governments are setting energy-transition, adaptation and industrial decarbonisation goals while also trying to crowd in private finance.

However, many of the barriers look familiar: early-stage projects remain too risky, business models are uncertain, public support is fragmented, and market architecture is often still incomplete.

The result is a stubborn gap between ambition and execution. The report’s core insight is that mobilising green finance is less about announcing more capital pools and more about doing the practical, earlier-stage work required to make sectors, technologies and projects financeable.

Capital Alone Will Not Deliver Deployment

More capital does not automatically translate into more deployment. That is the report’s central warning.

In the foreword, Green Finance Institute chief executive Rhian-Mari Thomas argues that the transition challenge is no longer only about ambition or available capital, but about doing the hard, practical work needed to make projects financeable at scale.

Capital still stays on the sidelines when sectors and technologies fall outside private investors’ risk-return thresholds.

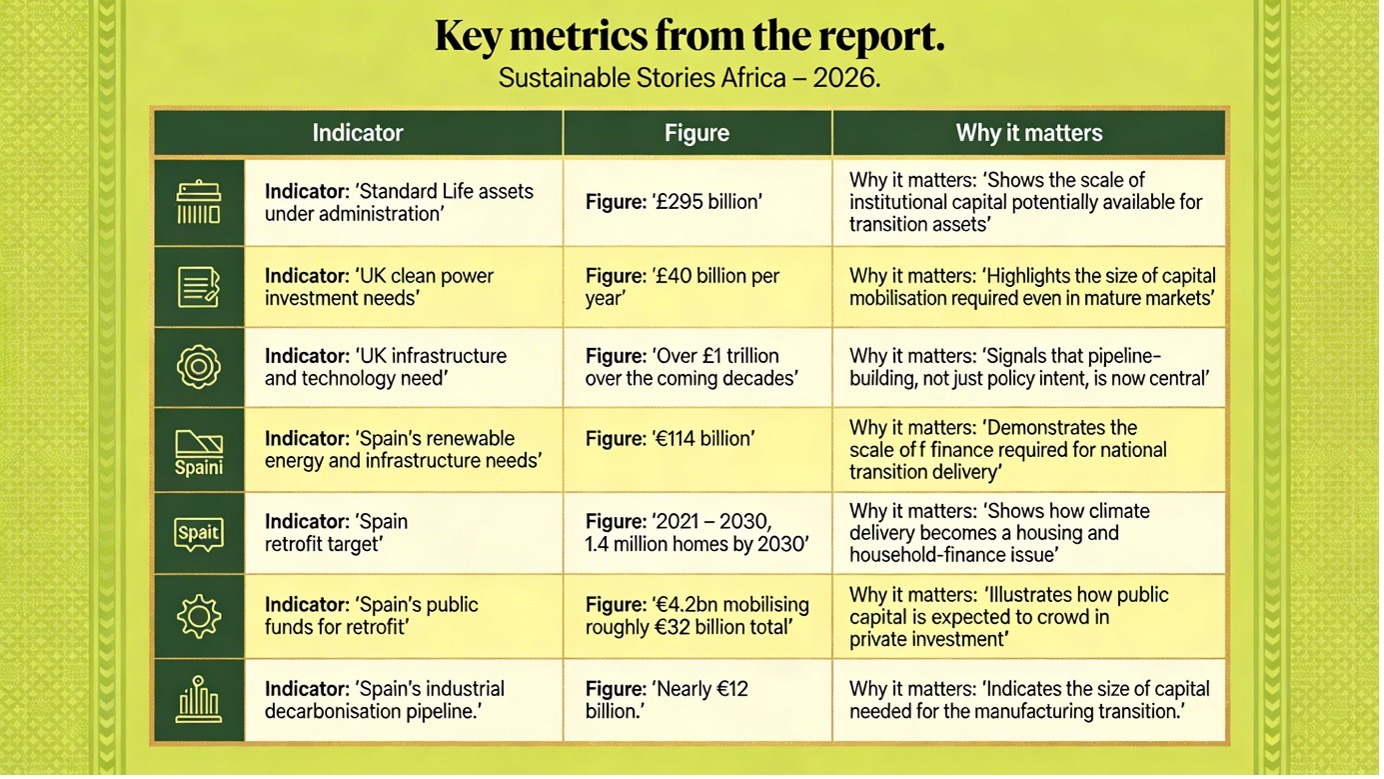

The report’s interviews and case studies reinforce that point. Standard Life, with £295 billion in assets under administration, says pension funds are willing to back the transition, but only where the risk-return balance is credible.

For African economies seeking finance for solar, grids, resilient infrastructure, industrial upgrades and nature-based solutions, the implication is clear: investor appetite can coexist with serious deployment bottlenecks.

Making Capital Move Requires Market Architecture

The report offers three useful lenses for understanding how capital moves.

- The first is institutional investors. It argues that long-term pension capital is well suited to infrastructure-style assets with stable cash flows, but only where policy clarity and long-term regulatory certainty exist.

Public finance institutions are also presented as critical catalysts, helping to derisk projects, structure transactions, and match opportunities with investors.

Tools such as guarantees, first-loss capital and blended finance are highlighted as especially important when assets are not yet investment-grade.

- The second lens is Spain’s system-level approach. Its climate and energy plan estimates that €114 billion will be needed for renewable energy and related infrastructure between 2021 and 2030.

It also targets 1.4 million home retrofits by 2030, with €4.2 billion in public funds expected to mobilise about €32 billion in total investment, while industrial decarbonisation could attract nearly €12 billion.

The key lesson is that barriers are less about capital scarcity than market organisation, demand stimulation and execution capacity.

- The third lens is execution. The report says many projects fail to move from ambition to investment-ready reality because early-stage and first-of-a-kind opportunities are often too risky, too small or too bespoke for mainstream investors.

Grants and subsidies remain useful, but on their own, they rarely deliver scale, durable debt markets or replicable models that can attract long-term institutional capital.

Better Market Design Can Unlock Transition

The positive case is not hard to see.

If governments and public finance institutions can improve policy certainty, structure pipelines and deploy catalytic instruments earlier, the transition becomes easier to finance and scale.

Pension funds get access to long-duration assets that fit their liabilities. Governments make better use of scarce public capital.

Businesses gain clearer routes to finance. Households can benefit from more affordable retrofit and efficiency programmes. And markets move from isolated pilot projects to repeatable structures.

For African economies, that could be transformative. Better market design could unlock financing not only for renewables, but also for transmission, mini-grids, industrial retrofits, clean transport, climate adaptation and resilient agriculture.

It could also help ensure that public climate spending is used less as a permanent substitute for private finance and more as a lever that brings it in.

Pragmatic Market Reform Can Unlock Capital

The report suggests a pragmatic agenda.

- Governments need to focus on market architecture: stable policy, streamlined approvals, stronger project aggregation, and clear long-term roadmaps.

- Public finance institutions need to place greater weight on catalytic impact, not just narrow portfolio returns, and use instruments such as guarantees, concessional capital, first-loss tranches and blended structures more strategically.

- Investors need to engage earlier in shaping investable pipelines rather than waiting for perfect assets to appear.

- Market institutions need better data, dashboards and reporting tools to track whether sustainable finance is actually reaching priority sectors.

For African policymakers, the core takeaway is simple: private capital does not arrive because a transition strategy exists.

It arrives when the strategy is translated into structures that make projects bankable.

Path Forward – Africa Needs Investable Pathways, Not Promises

Green finance mobilisation will depend less on announcing fresh ambition and more on building investable pathways.

That means stronger policy certainty, better project pipelines, smarter public de-risking and earlier coordination between governments, financiers and developers.

For African markets, the prize is larger than capital alone. It is the chance to turn climate and development priorities into durable financial ecosystems that can support the transition and the delivery at scale.