Companies are being asked to disclose more on climate, workers, communities and boardroom conduct.

The more difficult question is no longer whether to report, but what data is material, credible and decision-useful.

For African markets, that challenge is becoming strategic. Better ESG data can improve trust, sharpen risk management and strengthen access to capital, but weak data can turn reporting into noise rather than accountability.

Why reporting now depends on data

ESG reporting is increasingly moving beyond glossy statements and broad commitments. The more practical issue for companies is whether they can collect, organise and explain the environmental, social and governance data that regulators, investors, lenders, customers and communities now expect to see. In that sense, the core message of ESG Reporting: What Data Do Companies Need? is straightforward: sustainability reporting begins with data architecture, not public relations.

The document breaks the task into three familiar pillars, Environment, Social and Governance, but its deeper value lies in its simplicity.

It shows that meaningful ESG reporting is built from a defined set of measurable indicators: emissions, energy use, water and waste, workforce metrics, labour practices, board structure, ethics controls and reporting alignment.

For African and emerging markets, that matters now because reporting expectations are rising even where internal systems remain uneven.

Businesses are being pushed to show not just ambition, but evidence. Evidence depends on what data they track, how consistently they track it, and whether leadership uses it to manage risk, performance and credibility.

The reporting gap is operational

The document’s sharpest line comes on page five: “ESG reporting isn’t just numbers.” Instead, it frames disclosure as a commitment to People, Planet and Prosperity.

That matters because it expands reporting beyond templates and checklists, asking companies to show how they affect the systems around them and how seriously they manage those impacts.

However, that commitment must be anchored in data. The environmental section identifies five essentials:

- Carbon footprint

- Energy use

- Water usage and waste management

- Biodiversity impact

- Climate risk disclosures.

The value of that clarity is simple: credible sustainability reporting begins with measurable operational information, not broad language or brand positioning.

The real gap, then, is not vocabulary but data discipline. Where Scope 1, 2 and 3 emissions are not tracked, water use is unmeasured, or climate risk is detached from operations, reporting becomes fragmented.

That materially weakens comparability for investors and regulators, and weakens strategy for companies themselves.

What companies actually need

The document’s strongest contribution is its treatment of ESG as a practical reporting checklist.

- On the environmental side, it puts carbon footprint first, covering Scope 1, 2 and 3 emissions, alongside energy use split between renewable and non-renewable sources.

- It also includes water, waste, biodiversity and climate risk, making clear that environmental disclosure extends beyond carbon.

- The social pillar is equally operational. It tracks diversity through gender, age and ethnicity; well-being through safety incidents, training hours and turnover; labour practices through fair wages and supply-chain ethics; community engagement through philanthropy and local development; and customer responsibility through product safety and data privacy. In African markets, that breadth speaks directly to licence to operate.

- Governance brings the framework into the boardroom. The document points to board composition, executive pay, anti-corruption and ethics, risk management, and transparency through standards such as GRI and TCFD.

- The implication is straightforward: governance data shows whether ESG oversight shapes decisions or remains a peripheral communications exercise.

Read this way, the document works as a maturity ladder. Early-stage reporters may start with internal metrics, but stronger companies connect those metrics to risk systems, incentives and disclosure frameworks.

Its visual layout separates ESG into categories, yet the message is that weak governance can unravel environmental and social claims.

What better data can unlock

Stronger ESG data systems do more than improve disclosure. They sharpen management decisions, expose operational risks earlier, and help companies identify where costs, inefficiencies and reputational vulnerabilities sit.

A firm that can track emissions, energy mix, safety incidents or board oversight accurately is also better equipped to improve performance.

There is a market benefit too. Better ESG data can strengthen confidence among investors, lenders, customers and partners seeking evidence of risk management and integrity.

In African markets, consistent, credible reporting can become a marker of stronger governance and future readiness.

The social value is important. Measuring well-being, labour practices, community engagement and product responsibility makes ESG tangible, showing how business decisions affect workers, supply chains, public trust and real outcomes.

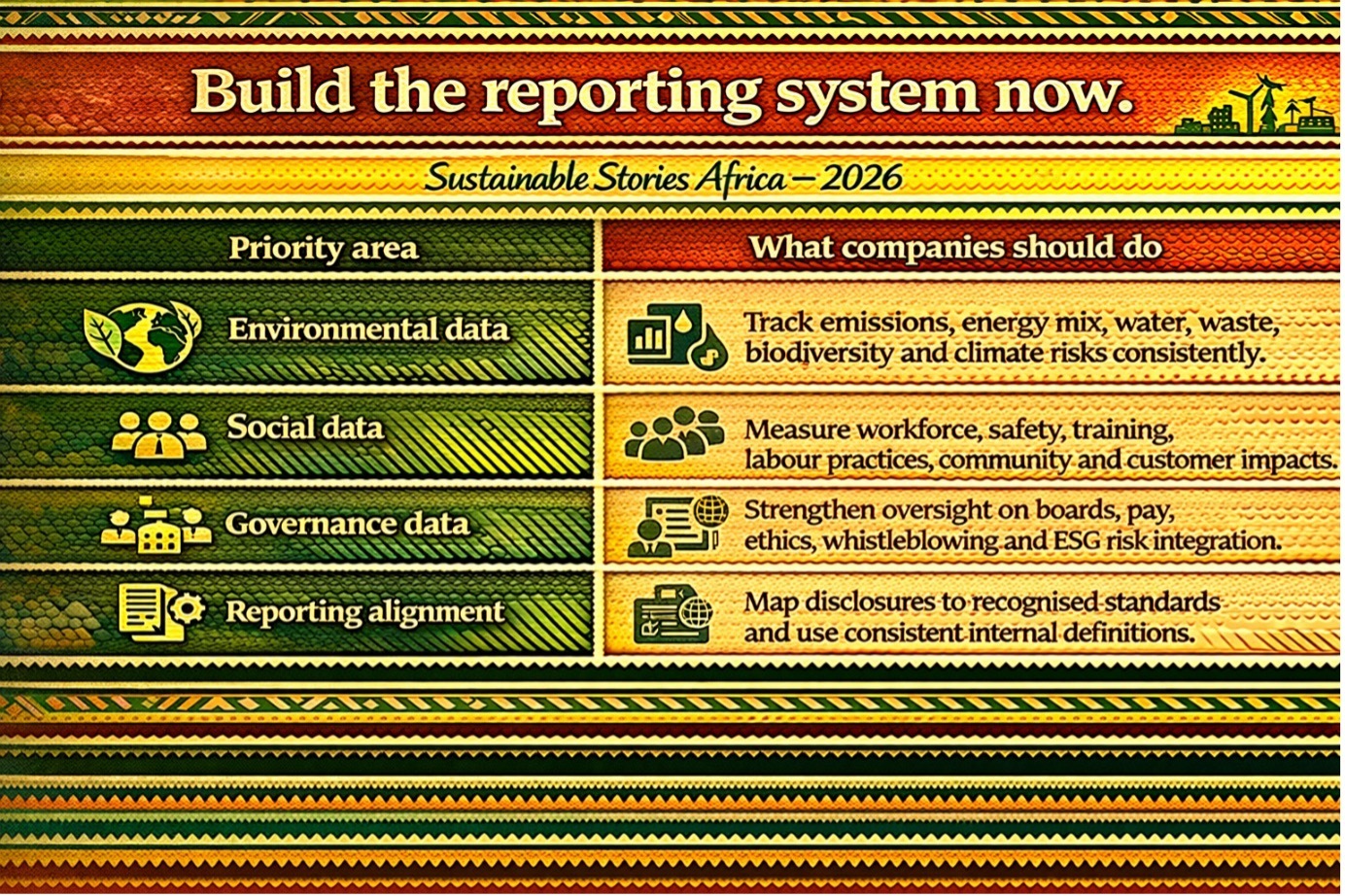

Build the reporting system now

ESG reporting should no longer be treated as a once-a-year writing task.

- Companies first need to map data across operations, finance, HR, risk, procurement and legal teams, then standardise definitions, assign ownership and align disclosures with frameworks such as GRI and TCFD.

- For boards and executives, governance data must be treated with the same rigour as financial data. That means tighter oversight of anti-corruption controls, whistleblower systems, executive incentives and ESG risk.

- For operating teams, reporting should stay grounded in site realities, from emissions and energy sources to water, safety, training and customer responsibility.

For African policymakers, exchanges and regulators, the message is practical: clearer guidance, phased requirements and stronger reporting literacy can help firms produce more credible, comparable disclosures.

Path Forward – Better data, better trust

The essential shift is from ESG storytelling to ESG evidence. Companies that know which data matters, who owns it and how it connects to strategy will be better placed to report credibly and act earlier on risk.

For African markets, the next step is disciplined simplification: start with material metrics, strengthen governance over data, and build reporting systems that serve people, planet and prosperity rather than just disclosure deadlines.