Sustainability due diligence is no longer a niche compliance concept reserved for large European corporates. It is increasingly being framed as the minimum management standard for responsible business conduct across operations and business relationships.

That matters for African and emerging-market companies now more closely tied to global value chains, disclosure regimes and investor screens.

The real question is no longer whether firms talk about ESG, but whether they can document how they identify, prevent, mitigate and account for adverse impacts.

From slogan to system now

The newest shift in sustainability governance is subtle but consequential. Companies are being pushed to move beyond broad ESG promises and toward something more operational: regular impact assessments in their own operations, clear expectations for business relationships, and documentation robust enough to satisfy regulators, investors, customers and affected stakeholders.

That is the core argument in the Global CSR insight note. Do you know? Sustainability Due Diligence.

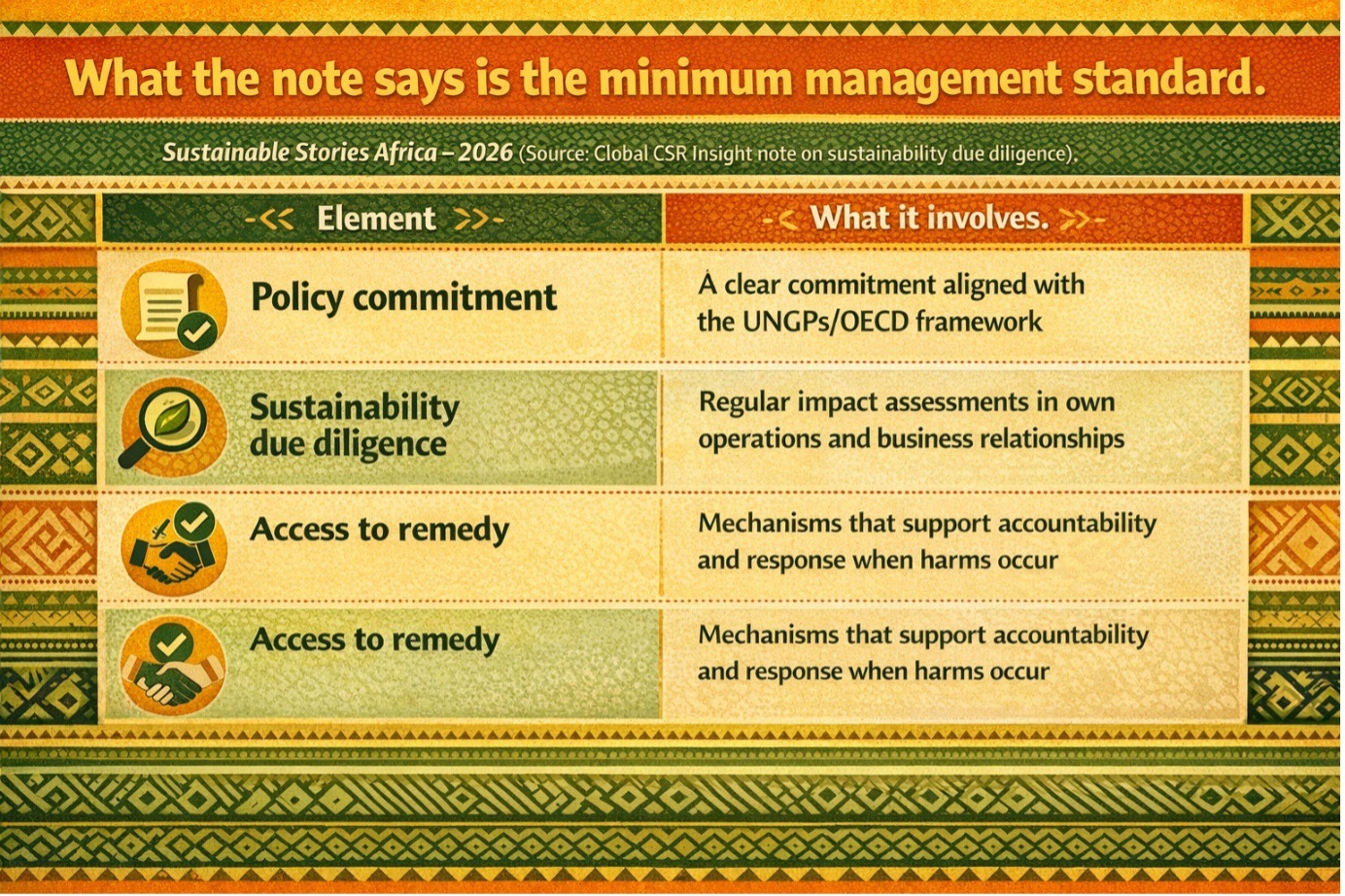

The note presents sustainability due diligence not as a voluntary add-on, but as a management process rooted in the UN Guiding Principles on Business and Human Rights and the OECD Guidelines.

In its framing, the minimum standard for responsible business conduct rests on three linked elements:

- Policy commitment

- Sustainability due diligence

- Access to remedy.

For African businesses selling into Europe, raising capital from sustainability-focused investors, or serving multinational customers, this matters because the compliance burden is already cascading through contracts and reporting expectations.

The largest firms may sit at the formal regulatory centre, but the operational pressure increasingly travels outward across value chains.

The compliance threshold is widening

The document makes clear that sustainability due diligence is no longer tied to a single EU rule. The CSDDD, SFDR, EU Taxonomy Regulation, and CSRD with ESRS are converging around one expectation: companies must apply the UNGPs and OECD Guidelines in practice, not just cite them in policy statements.

The issue is therefore not only legal overlap, but operational credibility. Without minimum due diligence standards, sustainability reporting weakens, especially where firms must disclose governance systems and material impacts with evidence.

That pushes due diligence beyond the largest companies directly exposed to fines or liability. It now reaches value chains, affecting suppliers, service providers and smaller firms expected to show governance discipline.

For African exporters, agribusinesses, manufacturers, fintechs and service firms, rising requests from European buyers, lenders and auditors are not random; they reflect a structured compliance chain in which due diligence is becoming a minimum threshold for market access and disclosure.

Interest: What due diligence actually requires

Sustainability due diligence, the document argues, is understood not as abstract ESG language but as an operational system organised around two tracks: a company’s own operations and its business relationships.

That distinction matters because it turns principle into process. Within operations, companies are expected to assess social, environmental and economic risks regularly, using a human rights baseline grounded in the International Bill of Human Rights.

The guide stresses that risk is not limited to large firms or sectors; any company, in any market, can affect multiple rights and sustainability outcomes.

It also rejects narrow compliance shortcuts. A supplier code, sourcing policy or limited labour-rights framework does not meet the minimum threshold if the broader UNGPs and OECD-based approach are missing.

It is also not enough to identify salient issues without addressing risks before they become severe. The document’s message is that credible due diligence must be documented, transparent and auditable, rather than merely declared.

The note draws a crucial line: investor-led ESG due diligence is not the same as company-led sustainability due diligence.

In African boardrooms, questionnaires do not replace systems required to identify, manage and document material impacts.

Why stronger due diligence can help

Read narrowly, this is a compliance story. Read more strategically; it is a capacity story. A company that builds a credible due diligence system becomes better able to identify operational risks early, engage stakeholders more, respond to customer scrutiny quicker, and reduce the chance that reporting becomes disconnected from reality.

The note goes even further by linking due diligence to double materiality. It says that adding material financial risks and opportunities to regular assessments can generate:

- The results needed for a double materiality assessment.

- Support ESRS 2 reporting and prevent irrelevant reporting or cumbersome parallel processes.

That is especially relevant for African firms trying to avoid duplicative sustainability exercises across lenders, buyers and reporting templates.

There is also a commercial upside.

- As sustainability clauses spread through procurement, financing and partnership agreements, companies that can demonstrate documented due diligence may find it easier to stay in preferred supplier pools, defend their governance quality and negotiate from a position of credibility rather than pressure.

That is an inference grounded in the note’s repeated emphasis on accountability to business relationships.

What companies should do next?

The practical response is not to build an oversized ESG bureaucracy. In fact, the note repeatedly says to keep it simple and keep the work lean.

However, lean does not mean superficial. It means structuring the process clearly:

- Assess own operations regularly

- Require business relationships to do the same

- Document the results

- Record efforts to prevent or mitigate impacts

- Use leverage where the company is linked to actual impacts in the value chain.

That also means avoiding false shortcuts. Companies should not confuse a supplier code with a real due diligence system, nor assume that reviewing only a few labour issues is enough.

They need broader sustainability coverage, stronger policy alignment, and regular assessments that are operational rather than purely legalistic.

For African regulators, business associations and corporate leaders, the next move may be to treat sustainability due diligence as a market-readiness issue.

Training, common templates, sector guidance and shared interpretation frameworks could help smaller firms meet rising buyer and investor expectations without being overwhelmed.

Path Forward – From promises to proof

The direction is becoming harder to ignore. Sustainability language alone will not satisfy regulators, investors or value-chain partners for long.

The operating test is whether a company can show a documented process for identifying, preventing, mitigating and accounting for adverse impacts.

For African markets, the smartest response is early preparation:

- Simpler systems

- Better records

- Stronger policy alignment

- Practical supplier engagement.

The firms that build this discipline now may find that due diligence becomes less a compliance cost than a passport to tougher markets.