Europe’s energy transition is still expensive, but perhaps less economically disruptive than many headline estimates suggest.

An IMF working paper says the EU can meet its climate and energy security goals with moderate macroeconomic effects by combining carbon pricing with targeted green subsidies and labour-tax relief.

The finding matters beyond Europe. For African and other emerging markets, the paper offers a sharper policy lesson: transition costs depend not only on ambition but on policy design, sector sequencing and what governments do with carbon-pricing revenues once they collect them.

Why policy design now matters

The IMF paper, The EU’s Energy Transition: Investment Impact and Role of Carbon Pricing Revenue Recycling, arrives as Europe tries to align climate ambition with industrial resilience and energy security.

The study examines how the EU could meet its existing 2030 target and a plausible 2035 pathway using a model that bridges “bottom-up” engineering-style estimates with “top-down” macroeconomic modelling.

Its central conclusion is that the transition does raise investment needs, but not by as much as some of the largest sector-based estimates imply.

That matters because the investment debate has often swung between two extremes. Detailed sector studies have suggested additional investment needs of approximately 2% and 3% of GDP a year.

Some macro models have implied negligible effects. The IMF argues that both camps have been partly right and partly incomplete: green investment is significant, but some of it replaces brown and other investments, which means the net economy-wide increase is smaller than gross headline numbers suggest.

For African policymakers and investors watching Europe, this is not just a regional modelling exercise. It is a live test of whether carbon pricing, subsidy design and fiscal recycling can be combined in ways that protect competitiveness while still driving decarbonisation.

That inference follows from the paper’s emphasis on policy mix, fiscal space and energy price management.

The investment shock looks smaller

The paper’s central message is that Europe’s transition will demand substantial green capital, but far less net new investment than headline numbers imply.

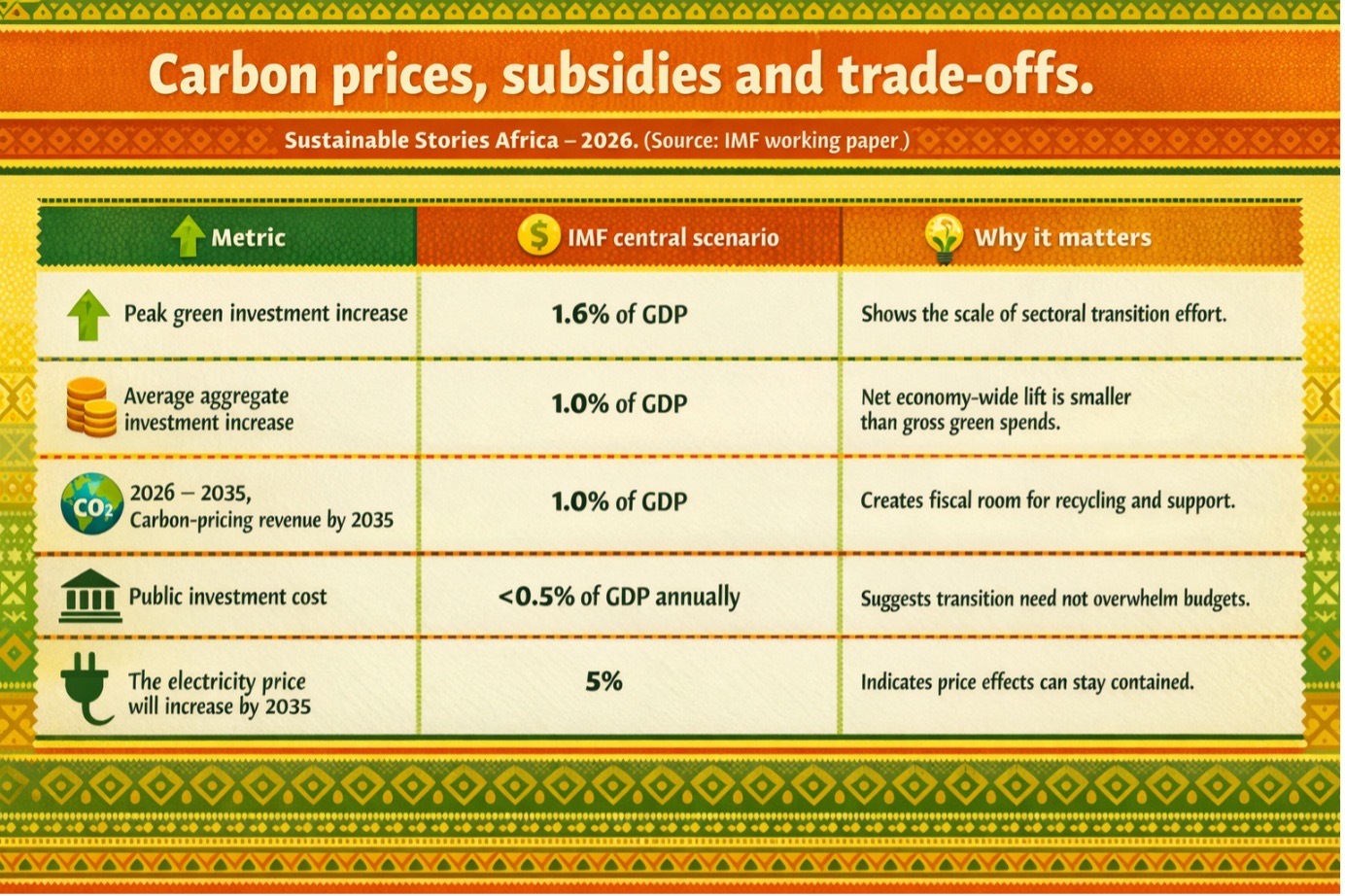

In the IMF’s baseline, green investment rises by 1.6 percentage points of GDP at its peak and averages 1.3 points during 2026 – 2035, equal to roughly €2.2 trillion cumulatively.

However, because greener spending displaces brown and other investments, aggregate investment rises by only 1.2 percentage points at peak and 1 point on average.

That places the IMF between bottom-up studies showing annual needs of about 2% to 3.5% of GDP and macro models suggesting near-zero or even negative overall effects.

Its estimate matters because it distinguishes gross green spending from net economy-wide investment. Some low-carbon capital replaces fossil-fuel extraction, gas heating and other carbon-intensive assets rather than simply adding to them.

The result is a transition that remains capital-intensive but more manageable than gross investment figures alone suggest.

Carbon prices, subsidies and trade-offs

The paper’s argument is not that the EU can drift into decarbonisation, but that policy design determines both cost and political durability.

In its central scenario, the transition is driven by tighter carbon pricing under ETS1 and ETS2, with two-thirds of carbon-pricing revenues recycled into green subsidies and one-third into labour-tax cuts.

Within the subsidy pool, two-thirds support renewable energy capital, while the balance is distributed among electric vehicles, building insulation and heat pumps.

That mix matters because it reallocates capital rather than simply adding cost, helping restrain electricity prices while accelerating investment in cleaner technologies.

The sectoral shift is clear. Renewable power investment rises strongly, building insulation more than doubles, and energy-efficient capital expands in energy-intensive tradable sectors, while EV adoption accelerates.

Brown investment falls sharply: gas heating declines, oil and gas extraction is phased out, and fossil assets lose ground.

Despite sharper carbon prices and revenues nearing 1% of GDP by 2035, the macroeconomic effects remain modest. Electricity prices rise by only about 5% by 2035, or roughly 0.5% annually, while inflation, consumption and interest rates stay contained.

A smoother transition is possible

The IMF paper’s most useful insight is that carbon pricing need not function only as a penalty; it can also finance a smoother transition.

In the central scenario, annual public investment costs remain below 0.5% of GDP, while revenues from ETS1 and ETS2 rise to about 1% of GDP. That suggests decarbonisation, if built around carbon pricing, can create fiscal space rather than deepen budget strain.

For emerging markets, the lesson is not to copy Europe line for line, but to design climate policy with a fiscal strategy from the outset.

Carbon revenues can fund targeted investment, cushion households, or reduce other distortionary taxes, with clear consequences for output, prices and investment.

The paper also shows that recycling choices matter. When revenues go only to labour-tax cuts or lump-sum transfers, green investment and overall macroeconomic outcomes weaken. Smart recycling reduces pressure for steeper carbon prices later on, too.

What policymakers should do next?

The paper’s practical recommendations are more important than the model itself.

- First, policymakers should stop arguing about carbon pricing and subsidies as if they are mutually exclusive. The IMF’s central finding is that they are complementary. Carbon pricing creates the signal and the fiscal space; green subsidies lower energy prices, support investment and reduce inflationary pressure.

- Second, governments need to think as carefully about revenue recycling as they do about carbon-price levels. Revenue can be used for labour-tax reductions, targeted household support, green deployment incentives, or public investment in systems such as grids and interconnectors. The paper argues that these choices are trade-offs across growth, energy prices, fiscal goals, energy security and distribution.

- Third, Europe still needs complementary reforms beyond carbon markets. The IMF points to the value of reducing policy uncertainty, clarifying regulatory standards, accelerating permitting, supporting energy-related public goods, and easing labour frictions and capital reallocation.

These are the less glamorous, but highly consequential, parts of transition execution.

Path Forward – Revenue use will decide

Europe’s transition debate is no longer only about how much it costs. It is increasingly about how intelligently those costs are distributed, financed and timed. The IMF answers that carbon pricing works best when paired with targeted support and credible follow-through.

For African markets, the underlying lesson is clear: climate ambition without revenue strategy can become politically brittle, but carbon pricing tied to visible investment, household protection and competitiveness can start as a development tool rather than a compliance burden.