Europe’s sustainability rulebook is being trimmed, not abandoned. The simplified ESRS has sharply reduced reporting volume, but leaves the core logic of double materiality, governance accountability and assurance intact.

For African exporters, banks, subsidiaries and supply-chain businesses tied to European markets, the question is no longer whether ESG rules are easing.

It is whether simplification creates room for better reporting, or reporting it exposes who still lacks systems, data and discipline.

Europe Rewrites ESG Reporting Burden

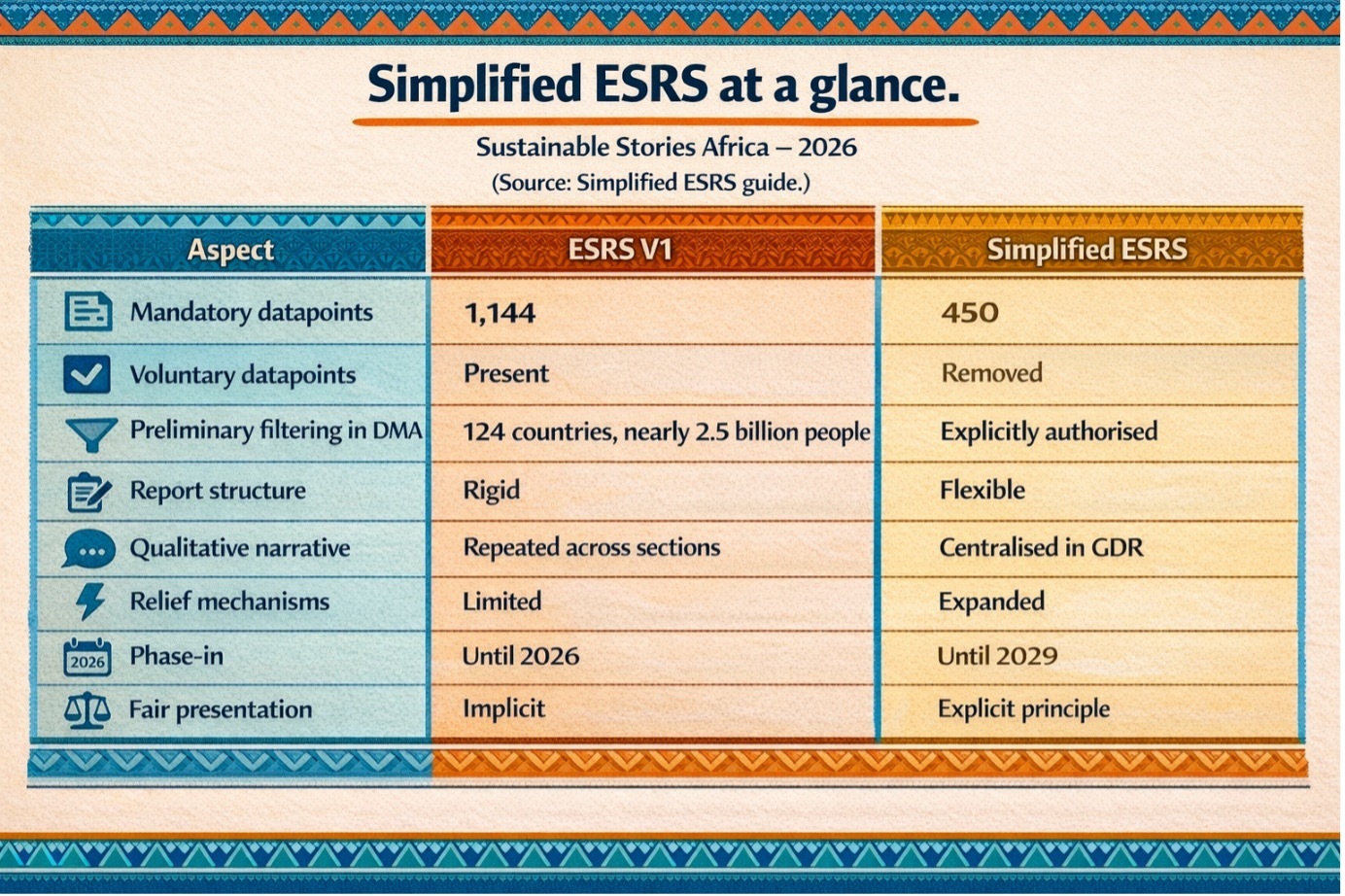

The European sustainability reporting regime is entering a more pragmatic phase. A new guide on the simplified ESRS shows the framework cutting mandatory data points from 1,144 to about 450, removing voluntary data points, formalising a “funnel approach” to double materiality, and expanding relief mechanisms for difficult disclosures.

However, the foundations remain intact: double materiality stays central, the 12 E-S-G standards remain, annual reporting is maintained, and external assurance still applies.

That is the real story. This is not deregulation dressed up as efficiency. It is a redesign meant to make compliance usable after first-wave reporters found the original framework too heavy.

The guide says EFRAG published the simplified ESRS in December 2025, with formal European Commission adoption expected in mid-2026, voluntary application for FY2026 reports published in 2027, and mandatory application for FY2027 reports published in 2028.

For African and other emerging-market companies connected to Europe through trade, investment, listings, lending, or group structures, that shift matters.

The rulebook may be lighter, but the demand for disciplined sustainability information is not disappearing. It is becoming more targeted.

Fewer Data Points, Same Stakes

The headline number is striking: a 61% cut in mandatory datapoints. That alone signals how far the original model had drifted from practical reporting capacity.

The guide describes the change as a move toward decision-useful disclosure rather than exhaustive compliance. Expert commentary in the document argues that the new approach lowers friction without changing the strategic direction of reporting.

Companies, it says, will still be expected to explain how sustainability matters are governed, managed and embedded in strategy.

That distinction is crucial. In many African markets, ESG reporting capacity is uneven. Large banks, listed firms and multinationals may have systems in place; mid-sized exporters, manufacturers and suppliers often do not.

Simplification reduces the barrier to entry, but it also narrows excuses. Once the rules are clearer, poor preparation becomes easier to spot.

Three Shifts That Make ESRS More Usable, and More Honest

The guide identifies three big shifts.

- First, the reduction in datapoints.

- Second, a more streamlined double materiality analysis that formally allows preliminary filtering of clearly non-relevant issues before deeper assessment.

- Third, greater structural flexibility and broader relief mechanisms.

That second point may prove the most commercially important. Under the simplified approach:

- Companies can move from broad mapping of business model, value chain and stakeholders to preliminary filtering, then in-depth analysis only on the remaining topics.

- Identifying the material disclosure requirements.

- The guide also introduces a gross-versus-net impact distinction, allowing companies to assess how far policies and actions have already reduced an impact.

The third shift is about usability. Reports can now open with a:

- A three-to-five-page executive summary

- Detailed methodologies, longer historical data and cross-reference tables can move into appendices.

- General Disclosure Requirements are also simplified and centralised, reducing repetitive narrative across standards.

- Crucially, companies must now clearly disclose when they do not have a policy, action plan or target on a material issue.

Companies with fragmented supply chains may omit data points under an "undue cost or effort" principle, provided they document difficulty and improvement plans, and may apply partial-scope reporting where full coverage adds limited analytical value.

Leaner ESRS Is an Opportunity, Not Permission to Stay Vague

For African companies, a streamlined ESRS is not a burden reduction; it is a strategic opening. Global ESG frameworks have long been criticised for favouring firms with mature data systems and deep reporting budgets.

A leaner standard offers a more realistic compliance pathway, particularly for businesses looking to protect access to European customers, capital, and procurement pipelines.

The commercial upside runs deeper. Shorter, more flexible reports with stronger narrative structure and transparent gap disclosures can transform compliance from a documentation exercise into a genuine management tool, one that speaks directly to investors, lenders, customers, and boards.

For emerging markets, the stakes are concrete. A Nigerian agribusiness exporting to Europe, a Kenyan manufacturer inside a European buyer's value chain, or a South African financial institution with cross-border exposure all benefit from clearer, more focused reporting.

But simplification carries a warning: it is not permission to stay vague. Credibility travels through supply chains, and the firms that treat leaner standards as lower standards will eventually pay that price.

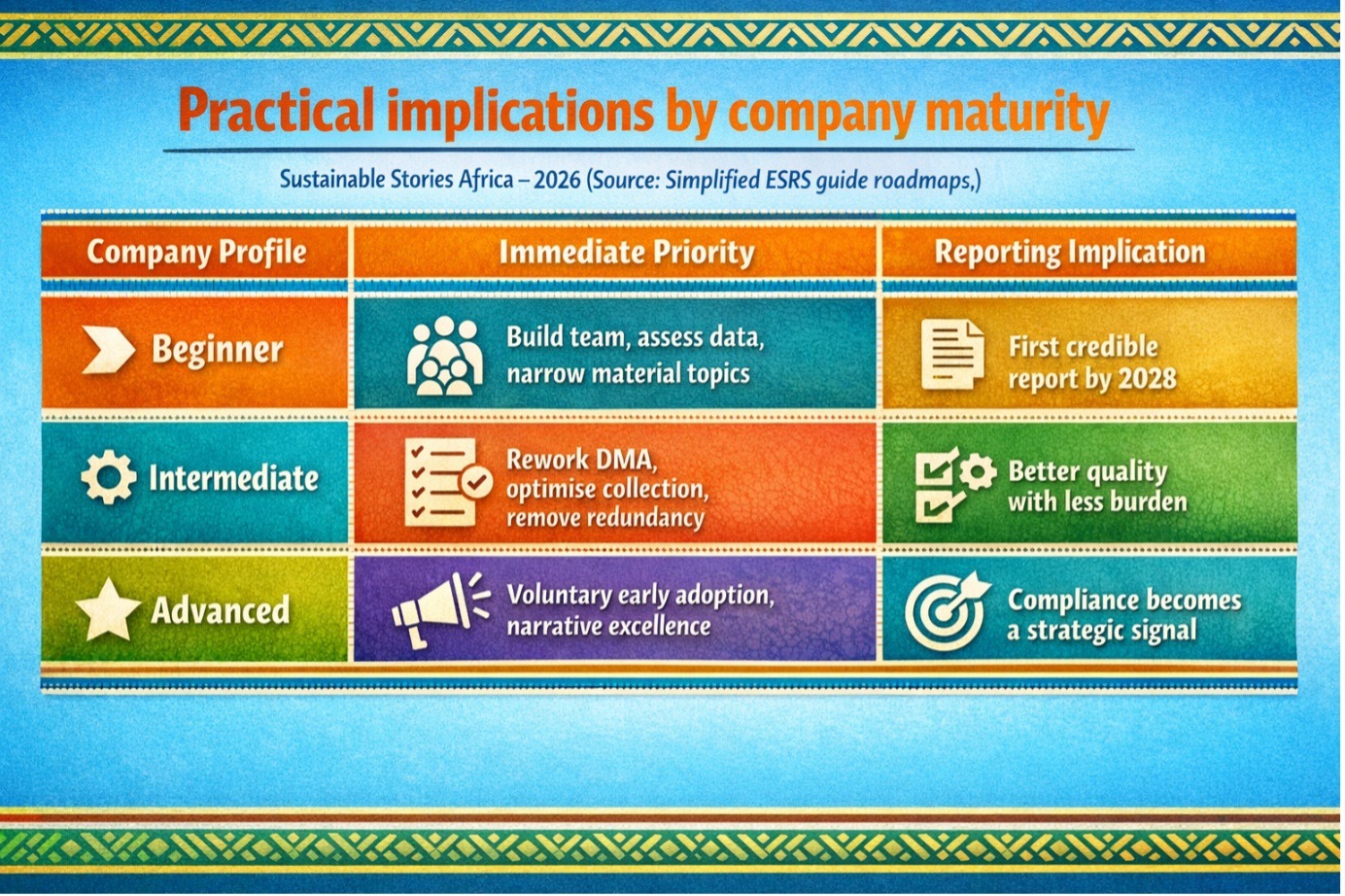

Three Profiles, One Clear Directive – Start Earlier Than You Think

The guide structures implementation across three profiles.

- Beginners with first reports due in 2028 should start in early 2027, building cross-functional teams, conducting maturity assessments, running disciplined materiality analyses, and applying relief mechanisms early, within a 13-to-18-month reporting window targeting spring 2028 publication.

- Intermediate companies should revisit materiality assessments, exclude a justified additional 20% – 30% of topics, automate data collection, and improve readability through executive summaries and appendices.

- Advanced reporters are encouraged to adopt the simplified model voluntarily from FY2026, publish earlier, and reframe compliance as leadership communication, turning regulatory obligation into competitive differentiation.

Materiality quality, documented relief justifications, fair presentation, and consistency with financial reporting are now the critical pressure points; weakly documented exclusions fail under audit, and balanced reporting outperforms polished reports that obscure difficulties.

Path Forward – Lighter Framework, Harder Questions

Simplified ESRS gives companies a narrower, clearer route to compliance, not a softer standard.

The task now is to focus on what is genuinely material, explain what is missing honestly, and build systems that improve year by year.

For African markets, the opportunity lies in moving from reactive disclosure to strategic readiness. The companies that win will be those that use simplification to sharpen governance, strengthen data, and prove integrity under pressure.