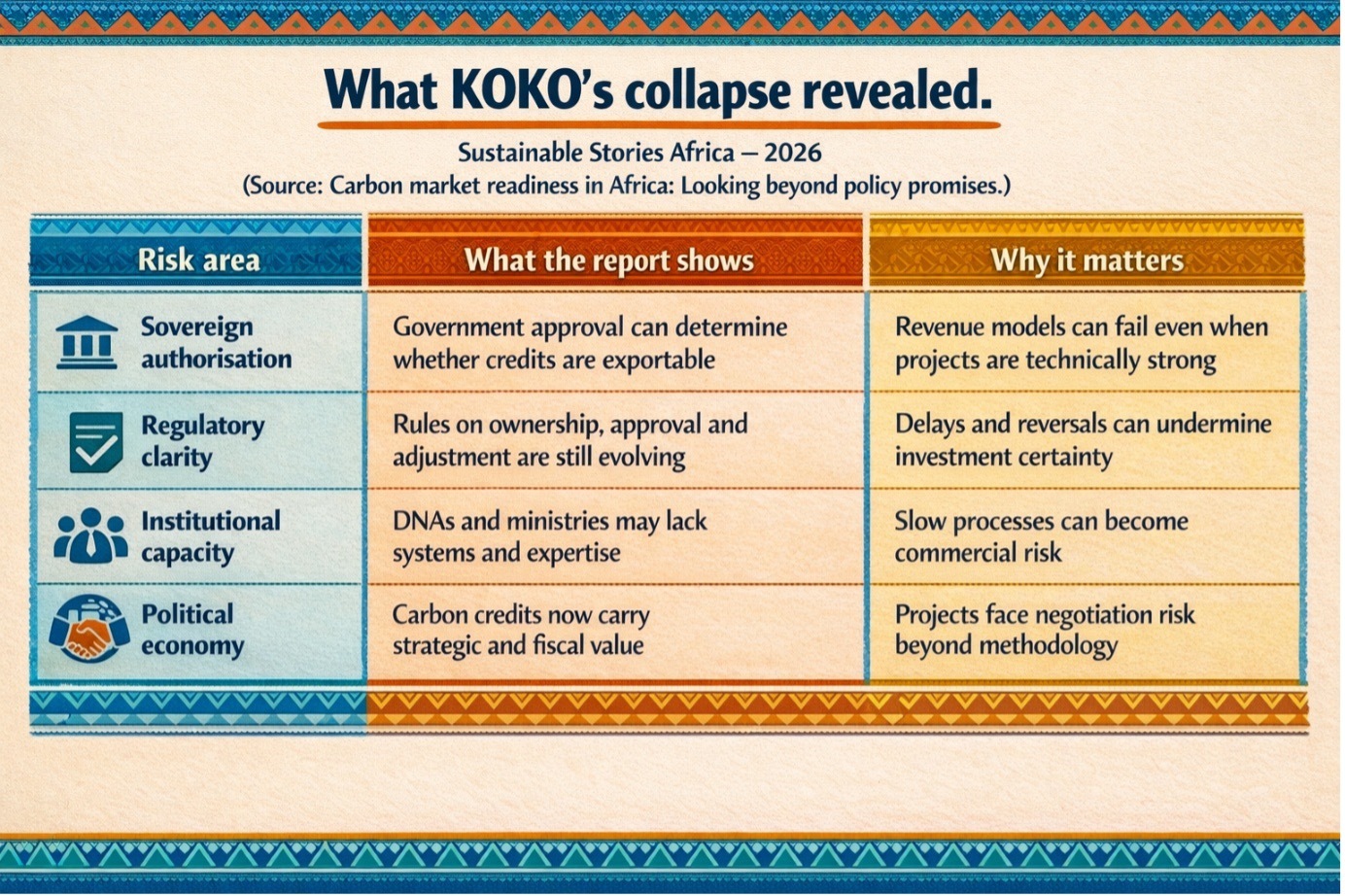

KOKO Networks’ collapse was not just a startup failure. It exposed a deeper shift in African carbon markets, where strong project design no longer guarantees viability if governments control authorisation, exports and value distribution.

That matters far beyond Kenya. As Article 6 matures, developers, investors and African governments are discovering that carbon credits are being treated less as private offsets and more like sovereign assets.

When Carbon Finance Meets Sovereignty

KOKO Networks' failure is more than a corporate cautionary tale; it is a systemic warning for Africa's carbon market ambitions.

The company's bioethanol cookstove model, financed through carbon credit sales, collapsed when Kenyan authorities declined to issue the Article 6 Letter of Authorisation required for access to the international compliance market.

The broader lesson is structural. Africa's carbon markets are shifting from a standards-led, largely private model toward a government-led framework where host-country approval, national accounting rules, and sovereign priorities now determine monetisation.

This creates a genuine opportunity for governments to gain greater control over national climate assets and benefit-sharing.

However, it sharpens an uncomfortable question for developers and investors: across a continent rich in mitigation potential, which markets are operationally ready for carbon finance, and which are still running on policy promises alone?

A Startup Failure, A Market Signal

The KOKO Networks case delivers one clear verdict: strong climate narratives are no longer enough. Carbon credits are increasingly treated as sovereign assets rather than private environmental commodities, and Article 6 of the Paris Agreement has formalised that shift.

This is because internationally transferred mitigation outcomes affect a country's own emissions accounting, host governments must now authorise credit exports and apply corresponding adjustments to national inventories, moving from passive observers to active gatekeepers.

For African governments simultaneously navigating climate finance mobilisation, national interest protection, and future target flexibility, approval power has become economically and politically valuable.

Carbon credits are beginning to resemble mineral concessions and spectrum licences, sovereignly allocated, strategically held, and no longer freely tradable without state consent.

Interest: Why The Ground Rules Are Changing

Africa's carbon market problem is not a shortage of political enthusiasm. Governments across the continent reference carbon finance in climate strategies, build project pipelines, and signal support for access to the compliance market. Kenya's 2024 investment framework agreement with KOKO Networks is one recent example.

However, political support and institutional readiness are not the same thing. Approval processes remain opaque in many markets.

Carbon ownership rules are still contested. National registries, MRV systems, and inter-ministerial coordination structures are still maturing.

Many Designated National Authorities understand climate policy but lack the capital markets capability to manage carbon credits as a distinct asset class.

The result is rising transaction risk driven by five compounding dynamics:

- Governments using approval scarcity to renegotiate terms

- Opacity in authorisation decisions

- Information asymmetry creates policy volatility

- Political cycles clashing with private investment timelines

- Carbon credits becoming tools of bilateral economic diplomacy.

A technically sound project can still fail when sovereign priorities, NDC flexibility, or political objectives take precedence over private investment timelines.

The report also revives a long-running debate of value distribution. Critics argue that international developers and buyers often capture too much of the upside, while host countries, communities and local producers see too little.

These concerns, often framed as carbon colonialism, are no longer just ethical critiques. They are influencing regulation through revenue-sharing rules, export limits and stronger sovereign control.

What A Better Market Could Look Like

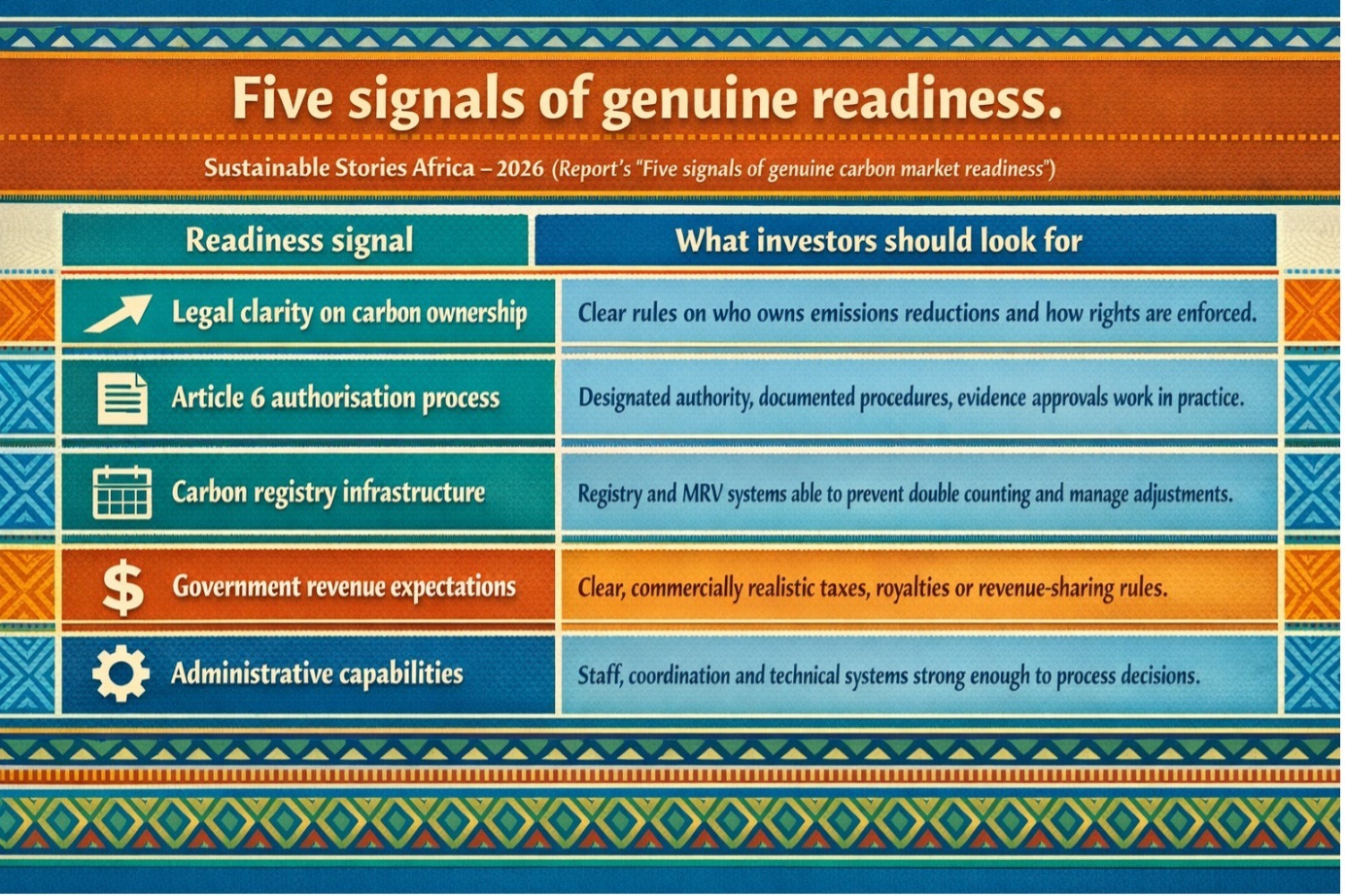

There is a positive reading of this shift. If done well, stronger sovereign oversight could produce more credible African carbon markets, not weaker ones.

- Governments that clarify ownership, formalise authorisation pathways, build registries and define benefit-sharing clearly can create markets that are more investable because they are more transparent.

- That would matter across the climate-finance chain. Developers would be able to price regulatory risk more accurately.

- Investors could distinguish first-mover opportunity from preventable political uncertainty.

- Communities could gain clearer rights and more visible participation in value distribution. Governments could protect national climate accounting while still attracting private capital.

The report identifies five signals of genuine carbon market readiness: legal clarity on carbon ownership; an operational Article 6 authorisation process

- Functioning carbon registry infrastructure

- Transparent government revenue expectations

- Real administrative capability inside institutions managing the market.

Those five signals amount to a practical readiness test for Africa’s next generation of carbon projects.

What Developers, Investors, and Governments Must Do

For developers and investors, political economy analysis can no longer be excluded from carbon project design. Technical expertise remains essential; however, understanding how governments allocate carbon credits is becoming as important as understanding how projects generate them.

Practical due diligence must now screen for authorisation risk, testing whether approval rules exist in practice, not only on paper; whether ministries coordinate; whether revenue demands are stable; and whether timelines are genuinely workable.

For governments, institutional credibility is the priority. Attracting durable carbon finance requires public approval processes, staffed institutions, functioning registries, clear ownership rules, and predictable benefit-sharing structures — not speeches and memoranda.

The KOKO Networks case delivers a direct message to African policymakers: stronger sovereign control over national carbon assets is legitimate and necessary; however, opacity, discretion, and political volatility carry a measurable cost.

Markets will price that uncertainty, and climate-finance flows will stall if governance clarity does not keep pace with commercial ambition.

Path Forward – Governance Will Decide Market Depth

The future of African carbon markets will depend less on project rhetoric and more on state capability.

Markets that clarify ownership, operationalise Article 6, and manage approvals transparently will be better placed to attract serious long-term capital.

KOKO’s collapse should not push investors away from Africa. It should push them toward deeper due diligence, better stakeholder engagement and a clearer reading of how governments govern carbon as a strategic asset.