A lot of companies now say they create impact. Far fewer can show, with evidence, what actually changed for people, communities or markets because of their actions.

That gap is becoming harder to hide. Investors, regulators and stakeholders are asking tougher questions, and the old habit of counting activities instead of measuring outcomes is losing credibility fast.

Why Proof Now Matters Most

The era of broad sustainability claims is giving way to something stricter: proof. A visual guide by Oluwatobi Anjorin argues that companies can no longer rely on glossy ESG language, activity counts or one-off reports if they want to be taken seriously on impact.

The document’s central challenge is blunt: a company may say it creates impact, but unless it can credibly measure change, the claim remains a story rather than evidence.

That message lands at an important moment for African and emerging markets. Across the continent, businesses are under pressure to show that sustainability programmes are not just philanthropic side projects or branding tools, but real interventions with measurable outcomes.

- In capital markets, blended finance, green bonds and ESG-linked funding increasingly depend on evidence.

- In policy, sustainability disclosure expectations are expanding.

- In communities, trust is becoming more conditional: people want to know whether corporate promises improved anything in practice.

The guide reframes the debate neatly.

- Impact assessment, it says, is not a marketing exercise.

- It is a systematic, evidence-based process that asks whether an action created real change and whether that change can be demonstrated with data.

- It focuses on outcomes, not just outputs.

That distinction, while simple, may be one of the most important governance tests now entering African business conversations.

The Metric That Exposes Reality

The difference between outputs and outcomes is where most impact reporting breaks down. Companies routinely declare what they did, such as planting trees, training women, and distributing solar panels, but rarely demonstrate what changed as a result.

The guide draws a sharp distinction: outputs describe activity; outcomes reveal impact.

The gap matters enormously.

- "Planted 10,000 trees" only becomes meaningful when 8,200 survive and reduce local flooding by 35%.

- "Trained 500 women" carries weight when 340 are earning 40% more.

- "Distributed 1,000 solar panels" translates to impact when household energy costs fall 60% across 1,000 families.

For African markets, this discipline is not optional. The continent faces urgent development challenges in which outputs are easy to announce, and outcomes are hard to verify.

Companies that cannot show what improved, for whom and by how much, leave a credibility gap, one that investors increasingly scrutinise, regulators are beginning to enforce, and communities have long recognised.

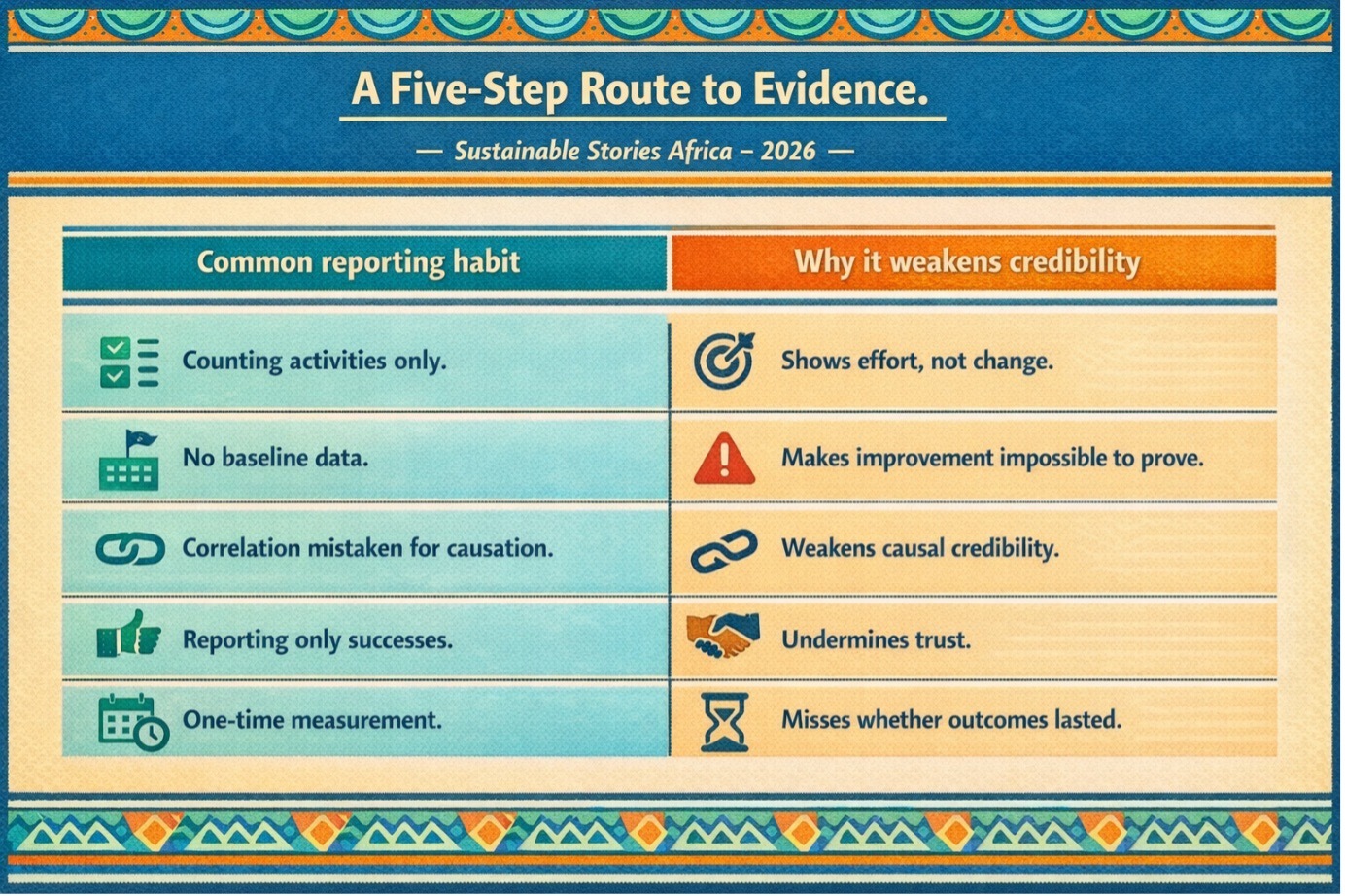

A Five-Step Route to Evidence

A practical five-step framework:

- Define

- Measure

- Attribute

- Value

- Report

It gives companies a structured path from sustainability ambition to measurable proof. The logic is deliberate: each step builds on the last.

- Companies must first define the specific change they want to create and for whom. Not broad language about helping communities, but concrete, time-bound targets, such as increasing household income by 20% for 500 farming families within 24 months.

- They must then measure change using indicators anchored to pre-intervention baselines, attribute credible outcomes, assign economic or social value to results, and report findings transparently, including what did not work.

- Attribution is the most demanding and the most revealing step.

- If incomes rose, was it the programme, better rainfall, broader economic recovery or another funder's intervention? If emissions fell, did the company drive the result, or did production slow?

Without honest attribution and clear measurements, correlation masquerades as impact.

In African markets, where external shocks, policy volatility and informal dynamics routinely shape outcomes, attribution is difficult; however, it is not optional.

- In the area of reporting, the guide also identifies five credibility failures that explain why many ESG reports feel polished yet unconvincing: vanity metrics, absent baselines, confusing correlation with causation, cherry-picking successes and one-time measurement.

These are not minor oversights; they are the difference between showing motion and providing proof.

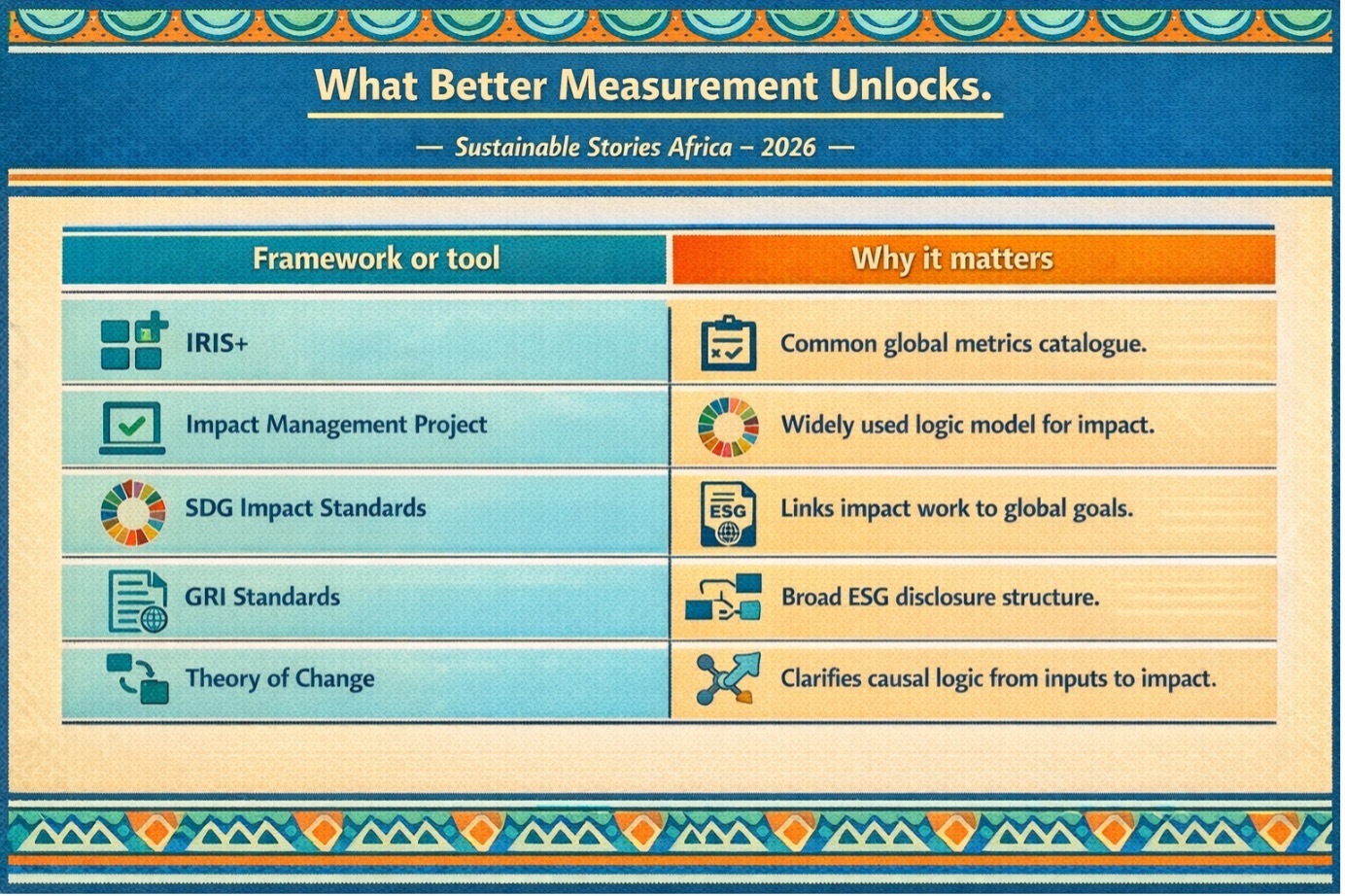

What Better Measurement Unlocks

If businesses take this seriously, the benefits extend far beyond compliance. Better impact measurement can sharpen management decisions, strengthen capital access, improve stakeholder trust and make sustainability spending more effective.

A company that knows which programmes genuinely raise incomes, reduce emissions, improve health or lower household costs can allocate resources more intelligently.

It also changes the quality of corporate conversation. Instead of defending reputation with anecdotes, firms can show evidence. Instead of competing on slogans, they can compete on outcomes.

For development-focused sectors in Africa, such as agriculture, energy, financial inclusion, health and manufacturing, this could be powerful. It would help businesses demonstrate not only intent, but contribution.

The guide’s recommended tools are useful here. It points companies toward established frameworks rather than asking them to invent a methodology from scratch.

These include

- IRIS+, used by more than 30,000 organisations worldwide

- The Impact Management Project, SDG Impact Standards, GRI Standards, and Theory of Change models.

The practical implication is reassuring: rigorous impact measurement is demanding, but the architecture already exists.

Move From Narrative to Proof

The broader lesson for African companies is clear. ESG and sustainability teams need to work more closely with finance, operations, monitoring and evaluation, and community-facing units.

Baselines must be built before programmes launch. Indicators must reflect real-world outcomes. Reports must include both progress and failure. Boards should begin treating impact evidence as a strategic asset, not a communications accessory.

There is also a role for policymakers, exchanges, investors and industry bodies. They can reduce confusion by encouraging greater standardisation, clearer disclosure expectations and stronger verification culture.

If capital increasingly rewards evidence, then the firms that build measurement discipline early will be better placed to attract funding and defend legitimacy.

The guide’s closing line deserves attention because it captures the shift in one sentence: impact without measurement is just a story; measurement turns it into evidence.

That is not merely a reporting lesson. It is a governance lesson, a market lesson and, increasingly, a leadership lesson.

Path Forward – Requires Honest Evidence

What is being advocated is straightforward but demanding: define change clearly, measure from the start, prove contribution, assign value and report honestly.

That is how impact claims move from branding to credibility.

For African markets, the next frontier in ESG may not be louder ambition but better evidence. The companies that measure what matters will be the ones most likely to earn trust, attract capital and create outcomes that endure.