ESG is holding its ground, but the story in 2025 is nuance, not hype. Global adoption has eased from record highs, yet 9 in 10 ESG users are still maintaining or increasing allocations, even as geopolitics and policy uncertainty continue to hit hard.

Energy transition, water and health now anchor conviction, while AI’s soaring energy and water appetite are pushing investors to refine their strategies, favour credible transitioners and reassess where real resilience and alpha will come from.

ESG resilience in a world on edge

ESG is no longer a fringe filter but a default lens. According to the ESG Global Study 2025 published by the Capital Group, 87% of global investors now incorporate ESG, only slightly below the record 90% reached in 2023 - 2024. Adoption remains above 90% in Europe, the Middle East, Africa and Asia-Pacific, even as North America slips to 71% amid politicisation and regulatory pushback.

However, the centre of gravity is shifting from rapid expansion to careful refinement. Over 90% of investors who use ESG either maintained or increased ESG allocations in the past 12 months, and a similar number plan to do so in the years ahead; however, more are holding steady rather than adding aggressively.

ESG holds, politics harden

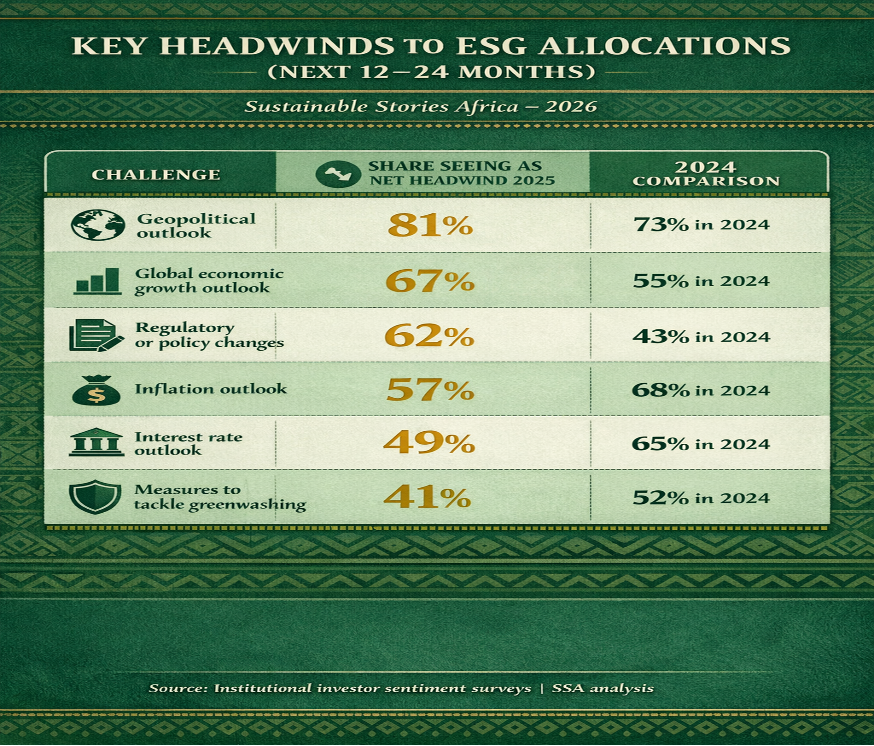

Geopolitics, Growth and Rules Test ESG Convictions. In the fifth edition of the ESG Global Study, geopolitical risk emerges as the single strongest headwind to ESG allocations, cited as a net negative by 81% of respondents. This is a 10.95% increase from 73% recorded in 2024. Concerns about global growth follow at 67%, while worries about inflation and interest rates have eased markedly compared to 2024.

Regulation has deviated from friend to friction. 62% now see policy and regulatory changes as a net headwind, with 80% of North American investors flagging it as a drag as against under 60% in APAC and EMEA. Even as some European fund‑name rules on ESG are seen as confusing, measures to tackle greenwashing have shifted from perceived headwind to net tailwind.

Key headwinds to ESG allocations (next 12–24 months)

Challenge | Share, seeing as net headwind 2025 | 2024 comparison |

|---|---|---|

Geopolitical outlook | 81% | 73% in 2024 |

Global economic growth outlook | 67% | 55% in 2024 |

Regulatory or policy changes | 62% | 43% in 2024 |

Inflation outlook | 57% | 68% in 2024 |

Interest rate outlook | 49% | 65% in 2024 |

Measures to tackle greenwashing | 41% | 52% in 2024 |

Portfolios pivot to themes, transition

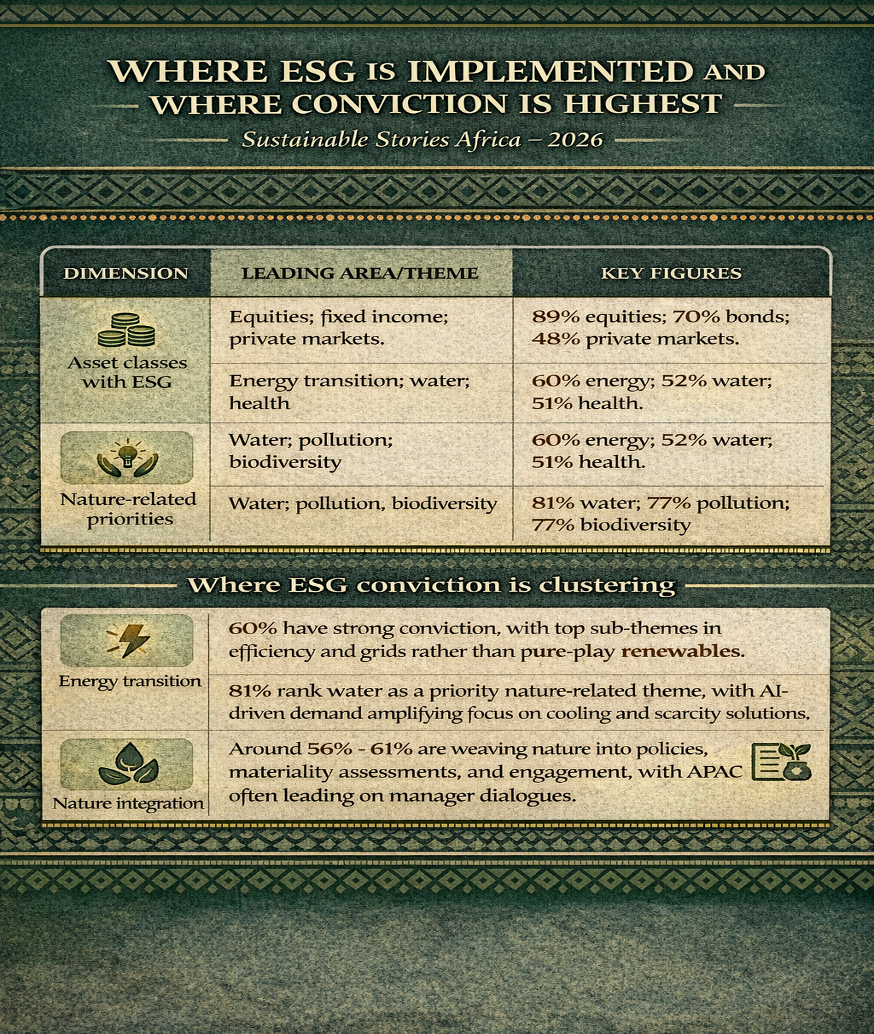

Refined ESG Playbooks, From Bonds To Nature. The architecture of ESG portfolios is changing. ESG is still most embedded in equities, but implementation in fixed income has climbed to a record 70% of respondents, up 9.385 from 64% in 2024, with corporate bonds as the leading sub‑asset class. ESG use in private markets has also reached its highest level, with 48% now applying ESG approaches despite data and transparency gaps.

Thematic investing is where conviction is coalescing. 60% of investors report strong conviction in energy-transition opportunities, while 52% say the same for clean water and sanitation and 51% for health and well‑being, with EMEA and APAC especially bullish on energy transition and North America favouring water.

Multi‑thematic ESG strategies are gaining favour for diversification, adaptability and efficient exposure across themes, with more investors planning to increase allocations to multi‑thematic than single‑thematic approaches.

Where ESG is implemented and where conviction is highest

Dimension | Leading area/theme | Key figures |

|---|---|---|

Asset classes with ESG | Equities; fixed income; private markets | 89% equities; 70% bonds; 48% private markets. |

Top conviction themes | Energy transition; water; health | 60% energy; 52% water; 51% health. |

Nature-related priorities | Water; pollution; biodiversity | 81% water; 77% pollution; 77% biodiversity. |

Investors are also gravitating toward transitioning organisations; these are firms shifting to more sustainable models. 56% say transitioning organisations are an increasingly important focus, and 58% believe that backing organisations with credible transition plans can be a source of long‑term outperformance, provided rigorous fundamental research underpins those calls.

Energy, water and AI rewire ESG

Conviction Concentrates In Transition, Health, And Nature. Within the energy transition theme, investors now rank energy efficiency (63%) and grid‑modernisation infrastructure (61%) ahead of renewable power generation (55%), reflecting concerns that a “wall of capital” has compressed returns in wind and solar. Electric mobility and nuclear attract niche but rising interest, while carbon capture and storage remain a minority conviction at 30%.

Water is expanding rapidly from background risk to headline theme. 81% of respondents rank water among their top three nature‑related investment opportunities, ahead of pollution, biodiversity and circular economy, with North American investors particularly focused on water as AI data‑centre build‑outs magnify concerns over cooling and scarcity.

This sits alongside surging interest in nature funds and policies: 61% already invest in, or are looking to invest in, nature‑focused mandates, and 56% now include nature in active ownership and engagement.

Managing defence, data and deployment

Investors Reassess Defence, Disclosure, And Deployment Pace. As wars reshape security debates, nearly 80% of investors running ESG or sustainable strategies still apply some form of defence exclusion, yet the ground is moving.

About 25% of respondents have shifted from excluding defence to allowing some exposure, and another 24% are actively reviewing their policies, with North America far more comfortable including all defence names than APAC or EMEA.

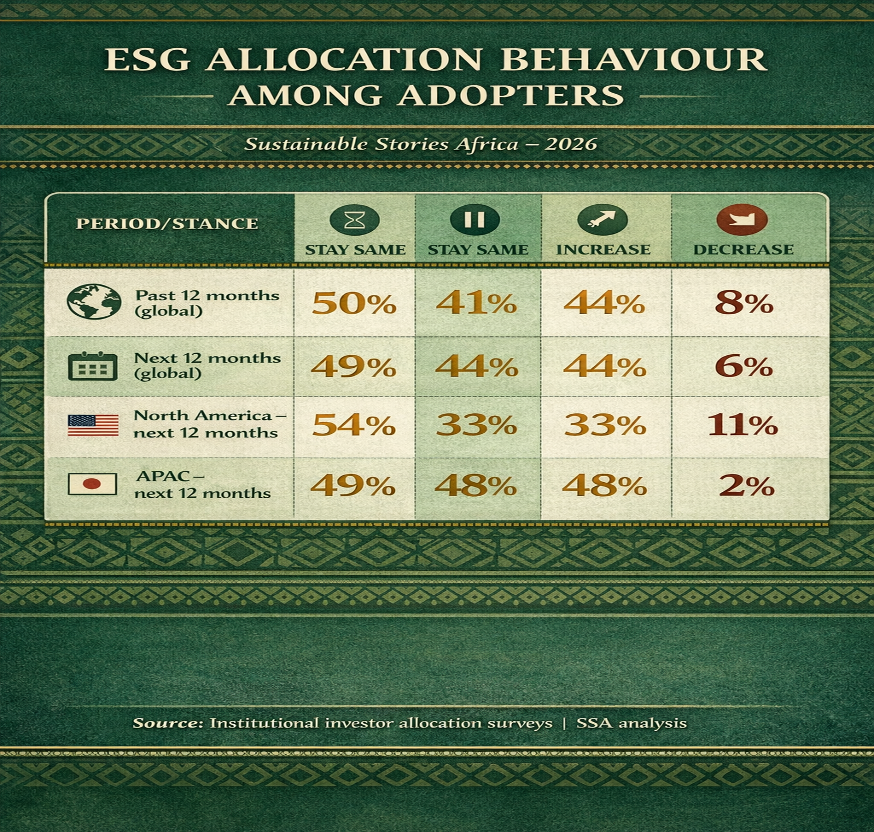

For implementation, investors are tightening how ESG is used rather than abandoning it. Over the past year, 41% of ESG adopters increased allocations, while 50% held steady, and only 8% reduced ESG exposure.

Looking ahead at 12 months, 44% expect to add more to ESG strategies and 49% to maintain, underlining a bias toward persistence and gradual refining of their strategies, rather than outright retreat.

ESG allocation behaviour among adopters

Period/stance | Stay same | Increase | Decrease |

|---|---|---|---|

Past 12 months (global) | 50% | 41% | 8% |

Next 12 months (global) | 49% | 44% | 6% |

North America – next 12 months | 54% | 33% | 11% |

APAC – next 12 months | 49% | 48% | 2% |

Path Forward – Navigating AI, nature and nuance

Balancing AI’s Promise With Planetary Boundaries. AI crystallises the new ESG paradox: 73% of investors predict AI’s energy use and greenhouse gas emissions as among the most material ESG risks over the next two to three years, and 43% point to rising water consumption as a key concern.

However, 56% also believe AI can ultimately accelerate innovations in decarbonisation, and 45% expect it to improve grid efficiency enough to offset part of its energy footprint.

Over the next cycle, the battle for credible ESG will be fought on three fronts:

- Sharpening transition frameworks for high‑emitting sectors

- Integrating nature and water into mainstream risk models

- Demanding far more granular AI‑related environmental disclosures from tech leaders.

For allocators, the opportunity lies in using ESG less as a label and more as a decision‑critical discipline, such as for pricing geopolitical and regulatory risk, backing genuine transitioning organisations, and aligning portfolios with energy, water and digital infrastructure that can deliver both resilience and returns.