Sodium-ion batteries, long overshadowed by lithium-ion batteries' dominance, are moving from laboratory promise to early commercial reality. New analysis from IRENA suggests they could reshape how the world thinks about battery supply chains, cost volatility, and energy security.

With production capacity accelerating and performance metrics improving, sodium-ion technology is emerging not as a silver bullet, but as a strategic complement, particularly for grid storage, two-wheelers, and cost-sensitive emerging markets.

A Second Battery Path Emerges

For more than a decade, lithium-ion batteries have been the undisputed backbone of the energy transition. They power electric vehicles, stabilise grids, and anchor renewable energy systems.

Their rapid cost declines and improving performance made them indispensable. However, the success has also created new vulnerabilities: concentrated supply chains, volatility of raw-material prices, and growing geopolitical risk.

A new technology brief from the International Renewable Energy Agency (IRENA) places sodium-ion batteries back into the spotlight. Once sidelined by lithium-ion's superior energy density, sodium-ion technology is now benefiting from advances in materials science, scale-up in manufacturing, and renewed concern about the sustainability of lithium-dependent systems.

For policymakers and investors, especially in emerging markets, the question is no longer whether sodium-ion batteries can work, but where they can be applied.

IRENA's analysis suggests they could play a meaningful role in diversifying battery supply chains, lowering costs in specific applications, and strengthening energy security without displacing lithium-ion outright.

Lithium's Success Is Becoming a Risk

The global battery boom is accelerating fast. Under IRENA's 1.5°C pathway, battery storage capacity must be expanded from 17 GW in 2020 to around 360 GW by 2030, and more than 4,100 GW by 2050.

Electric vehicles are expected to dominate road transport by mid-century, pushing annual battery demand into the thousands of gigawatt-hours.

However, lithium-ion's dominance comes with structural exposure. Lithium carbonate prices surged dramatically in 2022–2023, briefly exceeding $80,000 per tonne before retreating.

While prices have since moderated, the episode highlighted how quickly cost assumptions can unravel. At the same time, lithium supply chains remain geographically concentrated, amplifying geopolitical and logistical risk.

IRENA argues that this combination of surging demand, volatile prices, and concentrated supply has reopened the case for alternative battery chemistries. Sodium-ion batteries, built on far more abundant raw materials, are emerging as one of the most credible contenders.

What Makes Sodium-Ion Different

Sodium-ion batteries share a comparable cell architecture with lithium-ion systems, which reduces retooling requirements and eases integration into existing manufacturing lines.

The key difference lies in the materials and their availability: sodium is 2,000 times more abundant than lithium in the Earth's crust and roughly 60,000 times more abundant in seawater, with global soda ash resources estimated at 47 billion tonnes.

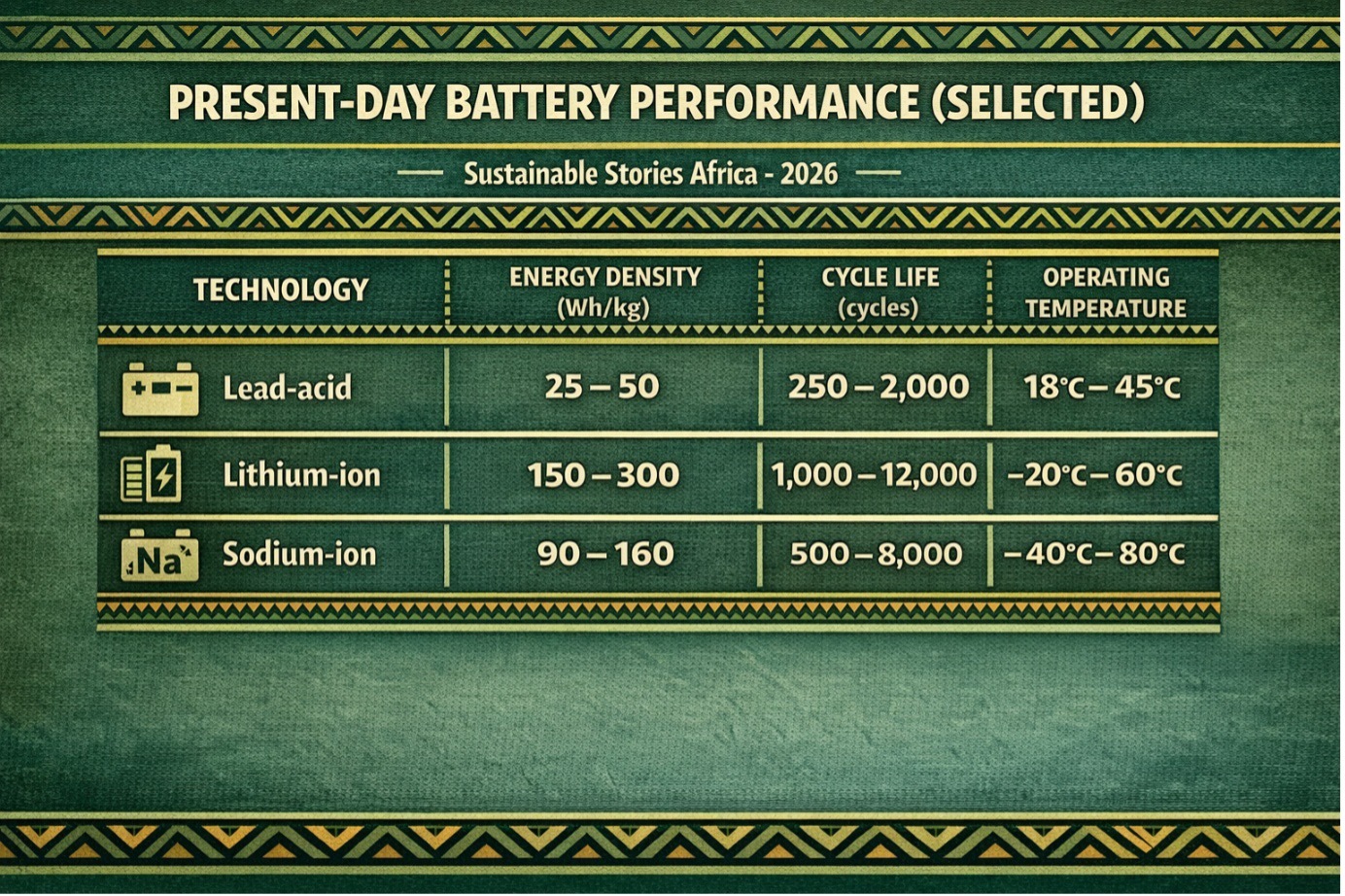

The performance of sodium-ion technology has clearly moved beyond the prototype phase. Commercial cells now reach 90 – 160 Wh/kg, with leading designs at 175 Wh/kg and roadmaps targeting 190 – 200 Wh/kg.

However, it is still trailing high-end lithium-ion chemistries; these energy densities already surpass lead-acid and most nickel-based batteries, converging with lower-tier lithium-ion systems.

Importantly, sodium-ion batteries operate reliably between -40°C and 80°C, retain capacity at low temperatures, and support fast charging, positioning them as strong candidates for stationary storage and e-mobility in demanding climate conditions.

Present-Day Battery Performance (Selected)

| Technology | Energy Density (Wh/kg) | Cycle Life (cycles) | Operating Temperature |

|---|---|---|---|

| Lead-acid | 25 – 50 | 250 – 2,000 | 18°C – 45°C |

| Lithium-ion | 150 – 300 | 1,000 – 12,000 | -20°C – 60°C |

| Sodium-ion | 90 – 160 | 500 – 8,000 | -40°C – 80°C |

Why Markets Are Paying Attention

Sodium-ion batteries are attractive not only for their chemistry but also for their economics. Pack prices of between $90 – $125 per kWh in 2022 were comparable to lithium-ion, and scaling effects could push cell costs toward $40 per kWh.

Supply-chain resilience is another advantage. Sodium-ion chemistries draw on manganese, iron, aluminium, and hard carbon, avoiding or minimising cobalt and nickel and reducing exposure to concentrated, high-risk mineral supply.

These properties align well with stationary storage, where cost, safety, and lifetime outweigh volumetric constraints, and with short-range EVs, two- and three-wheelers, and industrial fleets prevalent across emerging markets.

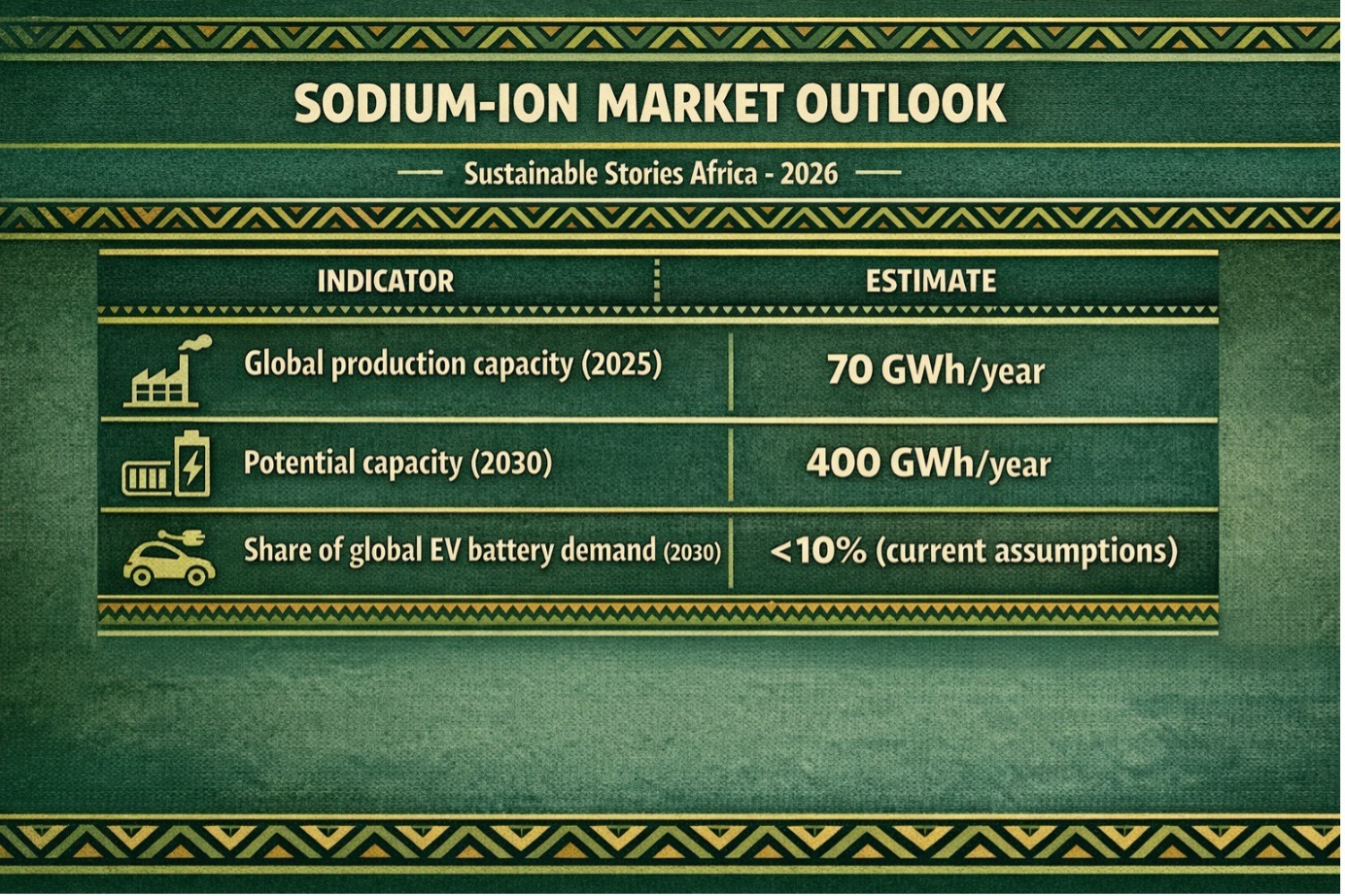

Sodium-Ion Market Outlook

| Indicator | Estimate |

|---|---|

| Global production capacity (2025) | 70 GWh/year |

| Potential capacity (2030) | 400 GWh/year |

| Share of global EV battery demand (2030) | <10% (current assumptions) |

From Curiosity to Strategic Choice

IRENA is careful to temper expectations. Sodium-ion batteries will not displace lithium-ion across all use cases, as energy density still limits their suitability for long-range vehicles and supply chains, particularly for hard carbon anodes, which must expand side by side with cell manufacturing.

Instead, the agency positions sodium-ion as a strategic complement. Emerging hybrid systems that pair lithium and sodium cells allow manufacturers to trade off energy density against cost, safety, and resilience.

For policymakers, the signal is clear: technology neutrality is important, but diversification is essential. Governments and utilities can begin mainstreaming sodium-ion through procurement, pilots, and grid-scale projects in cost- and climate-constrained settings.

PATH FORWARD – Diversifying Storage for a Fragile Transition

Sodium-ion batteries will not dethrone lithium-ion, but they may stabilise the energy transition by easing material risks and cost volatility.

The near-term priorities will be for scaling manufacturing, securing anode supply chains, and proving reliability at the grid scale.

If successful, sodium-ion technology could become a quiet workhorse of the transition, less visible than EV flagships, but critical to resilience, affordability, and energy security.