The comprehensive ESG Reporting Framework, aligned to six global standards, offers organisations a structured path from fragmented disclosure to credible, investor-ready sustainability reporting.

It consolidates GRI, SASB, TCFD, ISSB/IFRS S1-S2, CDP, and the UN SDGs into one integrated system.

For African businesses navigating rising regulatory pressure and investor scrutiny, this framework arrives at a critical moment, and its quantitative benchmarks set a new bar for what transparent, verified ESG performance looks like.

Unified ESG Disclosure – The Accountability Shift

The age of informal sustainability claims is ending. The ESG Reporting Framework provide organisations a rigorous, globally aligned methodology to measure, manage, and disclose Environmental, Social, and Governance (ESG) performance across six internationally recognised standards.

Spanning GRI 2021, SASB, TCFD, ISSB/IFRS S1-S2, CDP, and the UN SDGs, it consolidates what has long been a fragmented disclosure landscape into one single, auditable system.

For African corporates, development finance institutions, and regulators, the stakes are immediate. Global capital markets are increasingly conditioning investment decisions on the quality and credibility of ESG disclosures, and the EU's Corporate Sustainability Reporting Directive (CSRD) and IFRS S1 and S2 standards are reshaping expectations across supply chains, including those in Africa.

This framework does not simply describe what to report. It shows what measurable ESG leadership looks like, with targets, timelines, assurance pathways, and SDG linkages that transform sustainability from a narrative to a verified fact and from aspiration to bankable credential.

Six Standards. One Framework. Zero Excuses.

The most significant barrier to credible ESG reporting is not ambition; it is architecture. Organisations routinely publish sustainability reports that are selective, inconsistent, and impossible to benchmark.

This framework solves that structural problem by integrating six leading standards, each serving a distinct but complementary function.

GRI 2021 anchors stakeholder inclusiveness and material topics. SASB delivers sector-specific quantitative KPIs. TCFD introduces climate risk scenario analysis. ISSB/IFRS S1-S2 frames sustainability through financial materiality.

CDP captures carbon, water, and forest data. The UN SDGs tie every disclosure to 17 goals and 169 targets.

Together, they eliminate the most persistent excuse in corporate sustainability: "we didn't know what to measure."

The Metrics That Define Credible ESG Performance

The framework's FY2025 performance snapshot sets a clear, evidence-based benchmark. A 42% reduction in Scope 1 and 2 GHG emissions, 94% board independence, 40% women on the board, and zero material ethics violations are reported actuals, not aspirations, that anchor the accountability the framework demands.

On the environmental side, Scope 3 value chain emissions stand at 54,000 tCO2e against a 2025 target of 40,500 tCO2e. Renewable energy share rose from 52% in 2023 to 68% in 2024, tracking toward an 80% target in 2025 and 100% in the long term.

Water recycling rates are targeted to rise from 28% to 45%, while waste diverted from landfill moves from 62% toward 80%.

The social pillar is equally rigorous. Employee satisfaction (eNPS) rose from 42 to 61 between 2023 and 2024. The Total Recordable Injury Rate (TRIR) fell from 1.42 to 0.98 per 200,000 working hours, against a sub-0.75 target.

Community investment reached $1.84 million in 2024, benefiting 12,400 persons directly, against a target of $2.4 million and 18,000 beneficiaries by 2025.

Governance is where the framework directly addresses reform priorities. Board composition reports 73% independent directors, a CEO-to-median-employee pay ratio of 42:1 disclosed annually, and a fully active ESG Committee. Critically, 15% of short-term incentives and 20% of long-term incentives are formally tied to ESG metrics, including GHG reduction, DEI performance, and Net Zero alignment.

From Compliance to Competitive Advantage

The TCFD climate risk assessment reveals precisely what is at stake when ESG risks are left unmanaged.

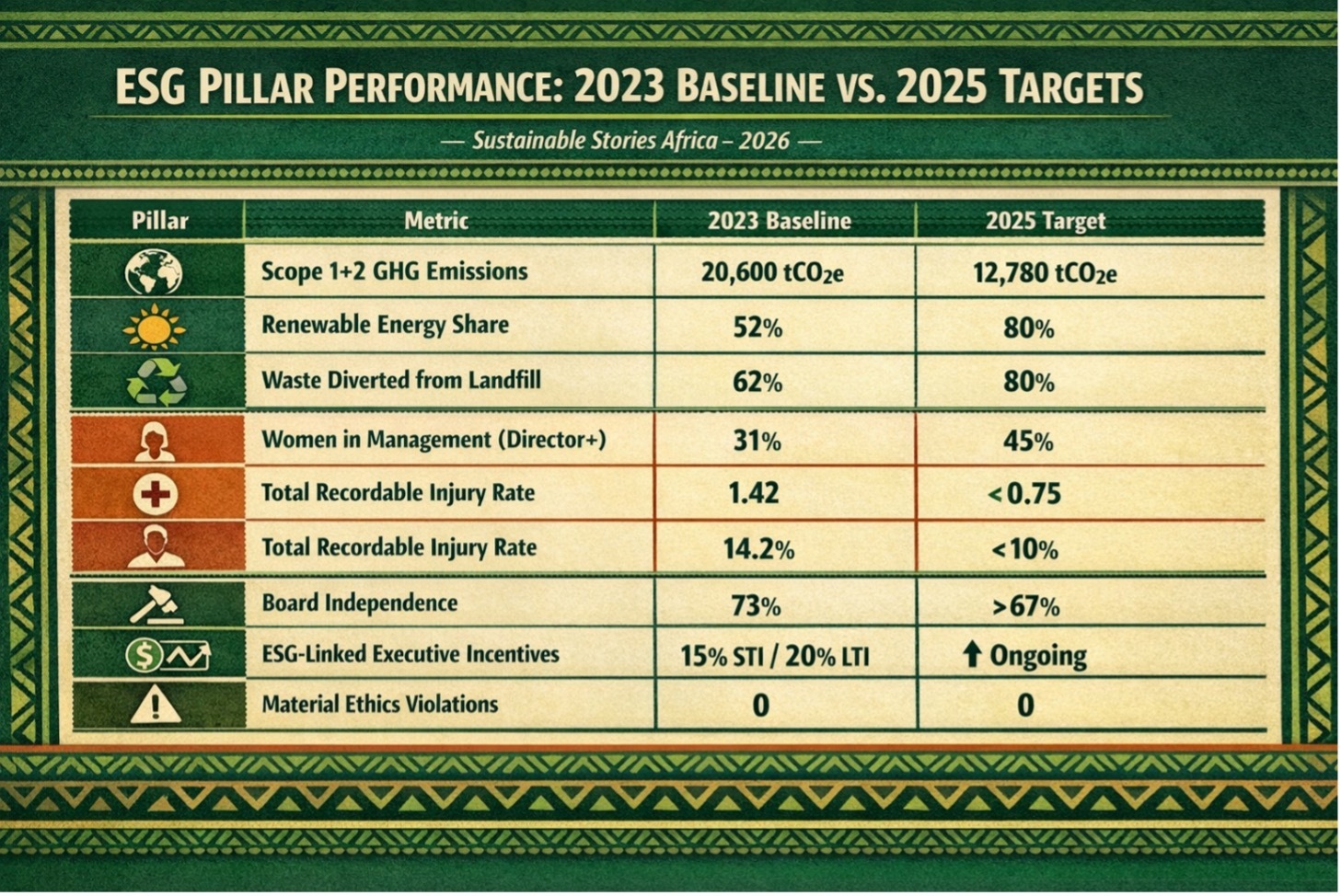

ESG Pillar Performance: 2023 Baseline vs. 2025 Targets

| Pillar | Metric | 2023 Baseline | 2025 Target |

|---|---|---|---|

| Environmental | Scope 1+2 GHG Emissions | 20,600 tCO2e | 12,780 tCO2e |

| Environmental | Renewable Energy Share | 52% | 80% |

| Environmental | Waste Diverted from Landfill | 62% | 80% |

| Social | Women in Management (Director+) | 31% | 45% |

| Social | Total Recordable Injury Rate | 1.42 | <0.75 |

| Social | Employee Turnover Rate | 14.2% | <10% |

| Governance | Board Independence | 73% | >67% |

| Governance | ESG-Linked Executive Incentives | 15% STI / 20% LTI | ↑ Ongoing |

| Governance | Material Ethics Violations | 0 | 0 |

Carbon pricing regulation carries a high-likelihood financial exposure of $2.4 million – $6.0 million. Physical flood damage: $0.8 million – $3.5 million.

Heat stress on operations: $0.5 million – $2.0 million. These are not abstract projections; they are quantified liabilities requiring board-level oversight.

The opportunity framing is equally compelling: green product demand, rated high likelihood, unlocked revenue upside of $8.0 million through R&D investment.

For organisations that proactively manage these risks, the framework converts ESG performance into a measurable financial advantage.

Implement With Rigour, Disclose With Honesty

The implementation roadmap runs across four structured phases with named owners and defined tools.

ESG Assurance Pathway to Full Credibility

| Year | Assurance Level | Scope | Standard | Provider |

|---|---|---|---|---|

| 2023 | Readiness Review | GHG Scope 1 & 2 | ISAE 3000 | Internal Audit |

| 2024 | Limited Assurance | GHG + 10 Social KPIs | ISAE 3000/AA1000 | Big-4 Firm |

| 2025 | Limited Assurance | All material ESG metrics | AA1000AS 2020 | Big-4 Firm |

| 2026 | Reasonable Assurance (target) | Full ESG dataset | ISAE 3000/IAASB | Big-4 Firm |

The Foundation phase, the double materiality assessment, baseline data, and policy review were completed in Q1 2025.

Infrastructure deployment is in progress in Q2 2025. Full business-unit data collection follows in Q3, with external assurance and report publication planned for Q4 2025.

Optimisation, CSRD readiness, and reasonable assurance are planned to commence from 2026

The framework's data quality, demand standards of ≥95% metric completeness, ±5% variance tolerance, 3-year trend data for all KPIs, and data locked within 90 days of fiscal year close.

These are not aspirational; they are the conditions under which any ESG disclosure can credibly claim to be investor-grade.

Path Forward – Disclosure That Delivers

The ESG Reporting Framework Version 1.0 is not a theoretical guide; it is an operational blueprint with timelines, owners, and measurable targets across all three pillars.

The double materiality lens, six-standard alignment, and progressive assurance pathway make it one of the most complete disclosure instruments available to any organisation.

For African businesses, the directive is clear: adopt the architecture, own the data, and verify the outcomes. Credible ESG disclosure is no longer a differentiator; it is the baseline for sustained access to capital, talent, and trust.