Not all gas is the same. The distinction between Compressed Natural Gas, Liquefied Petroleum Gas, Piped Natural Gas, and Liquefied Natural Gas determines which communities gain access to energy, which industries can scale, which transport systems can decarbonise, and which nations can attract investment.

Africa, with 331 billion cubic metres of annual natural gas production and a continent-wide energy deficit, urgently needs this conversation.

The right gas, delivered through the right infrastructure, to the right end-use; that is the energy transition Africa cannot afford to get wrong.

Not All Gas Is Equal

Walk into any market in Lagos, Nairobi, Accra, or Kinshasa, and you will find LPG cylinders stacked: the continent's most familiar face of gas access.

Drive through Abuja, Dar es Salaam, or Cape Town and CNG-powered buses and tuk-tuks are increasingly visible, steadily displacing diesel vehicles. Travel to the industrial corridors of Egypt, Algeria, or South Africa and piped natural gas is powering factories, utilities, and fertiliser plants.

Off the coast of Mozambique, Mauritania, and Nigeria, billion-dollar LNG tankers are transforming long-stranded gas reserves into global export commodities.

Each of these represents a different form of gas: compressed, liquefied, piped, and cryogenic, each with its own physical properties, use cases, infrastructure requirements, and economic implications.

Together, they constitute Africa's most important near-term energy toolkit: a suite of transition fuels that, deployed strategically, can reduce energy poverty, power industrial growth, and lower emissions simultaneously.

Africa's natural gas demand is set to more than double by 2050, with its share of the continent's total energy mix rising to approximately one-fifth.

That trajectory makes gas literacy not an academic exercise, but a practical imperative for every policymaker, infrastructure investor, corporate energy manager, and citizen trying to understand the energy future being built around them.

The Deficit That Makes Gas Choice Matter

Africa remains the epicentre of the world’s energy access crisis, with about 600 million people still lacking reliable electricity.

Per capita power consumption has stagnated or even declined, even as populations and economies expand, exposing infrastructure failures.

In this context, understanding what each gas type does in a technical debate is not merely; it is central to development, competitiveness, and dignity.

The continent produced 331 billion cubic metres of natural gas in 2025, led by Algeria, Nigeria, and Egypt; however, it still imports fuels, leans on diesel, and depends heavily on biomass. Distinguishing CNG, LPG, PNG, and LNG matters.

Four Fuels, Four Distinct Realities

The four gas types differ fundamentally in how they are stored, transported, and used. These differences determine their fitness for different markets, geographies, and industries.

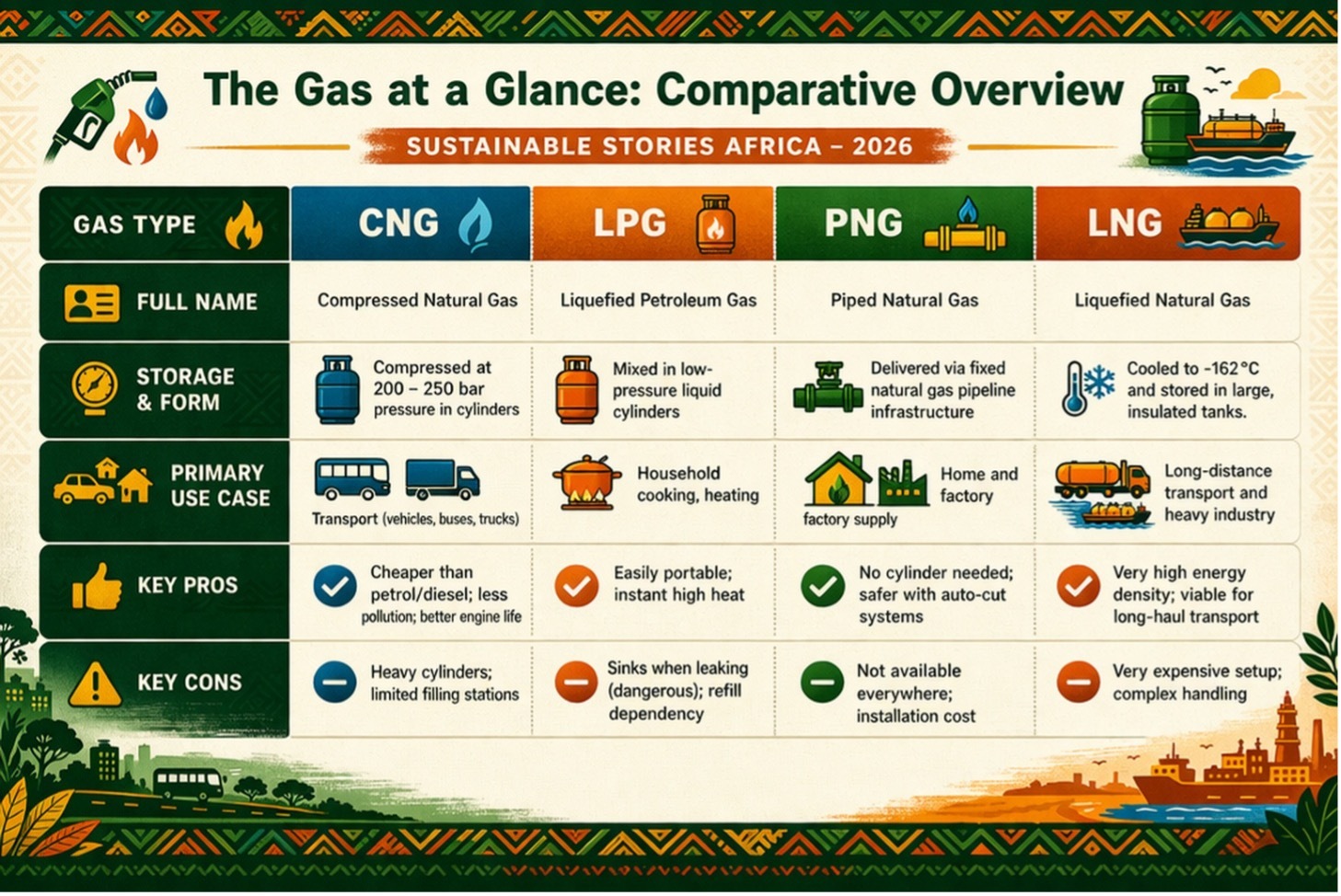

The Gas at a Glance: Comparative Overview

| Gas Type | Full Name | Storage & Form | Primary Use Case | Key Pros | Key Cons |

|---|---|---|---|---|---|

| CNG | Compressed Natural Gas | Compressed at 200 – 250 bar pressure in cylinders | Transport (vehicles, buses, trucks) | Cheaper than petrol/diesel; less pollution; better engine life | Heavy cylinders; limited filling stations |

| LPG | Liquefied Petroleum Gas | Mixed in low-pressure liquid cylinders | Household cooking, heating | Easily portable; instant high heat | Sinks when leaking (dangerous); refill dependency |

| PNG | Piped Natural Gas | Delivered via fixed natural gas pipeline infrastructure | Home and factory supply | No cylinder needed; safer with auto-cut systems | Not available everywhere; installation cost |

| LNG | Liquefied Natural Gas | Cooled to -162°C and stored in large, insulated tanks | Long-distance transport and heavy industry | Very high energy density; viable for long-haul transport | Very expensive setup; complex handling |

- CNG: Transport's Cleanest Affordable Fuel – CNG is gaining ground in Africa as a cheaper, lower-emission alternative to petrol and diesel, especially in transport and light industry. Nigeria and Tanzania are expanding retail infrastructure, but the model depends on scale. Its promise will remain limited until African cities build denser networks of compression and refuelling stations.

- LPG: The Household Energy Solution – LPG remains Africa’s most widely used gas because it is portable, energy-dense and can quickly displace biomass in homes and small businesses. However, safety risks from leaks, high upfront cylinder costs, and dependence on refill still limit adoption. Consumption remains far below global levels, leaving millions in harm from biomass-related challenges.

- PNG: The Industrial Backbone – PNG remains the benchmark for gas access, offering continuous, convenient and potentially safer supply when properly installed. However, Africa’s constraint is cost: pipelines require heavy capital investment. North Africa shows the upside, with Egypt and Algeria using PNG to support industry and power generation. For sub-Saharan Africa, expansion is transformative.

- LNG: The Export Engine and Heavy Industry Solution – LNG demands the highest infrastructure spending, but its returns can be substantial. Projects across Mozambique, Nigeria, Senegal, Mauritania and Angola are turning stranded gas into export revenue, jobs and local business opportunities. Beyond trade, LNG also supports cleaner long-haul transport, offering a lower-emission alternative to diesel in trucks and shipping.

The Scenario Where Gas Gets It Right

If African governments, regulators and investors align gas use with the right economic purpose, the gains could be far-reaching.

CNG can clean up urban transport and cut transit costs. LPG can reduce indoor air pollution, deforestation and the estimated 600,000 premature deaths linked to biomass cooking each year.

PNG can anchor industrial parks, lower operating costs and support job creation, while LNG export earnings can help finance the infrastructure needed to sustain wider energy access.

The African Energy Chamber’s 2026 Outlook Report points to this integrated pathway, with countries advancing gas-to-power plans, regional pipelines and LNG exports in parallel.

If that segmentation fails, Africa risks deeper energy poverty, weaker industrial competitiveness and the continued stranding of gas reserves that should serve domestic development first.

Who Needs to Move and How

Governments need to move faster on CNG refuelling networks while advancing public transport electrification, treating CNG buses and trucks as an immediate, deployable solution.

They must also strengthen LPG safety rules and subsidy systems so clean cooking becomes affordable, especially for households still locked out by cylinder and regulator costs.

Regulators and utilities should extend PNG networks into industrial zones, free trade areas and manufacturing corridors, where a reliable gas supply can lower costs and unlock investment.

Development finance institutions must widen support for domestic gas infrastructure. While LNG exports attract private capital, LPG and PNG networks need concessional finance, guarantees and patient funding.

Path Forward – Aligning Africa’s Gas Future With Purpose

Africa’s gas opportunity is large, real and time sensitive. Production is rising, demand is accelerating, and infrastructure gaps are narrowing, but only where policy and capital align. The priority is clear: match each gas type to its most valuable and sustainable use, then build the systems to deliver it at scale.

Each CNG bus, LPG cylinder, PNG line and LNG cargo represents a practical step toward the energy future Africa needs. The policy coordination and investment to connect them must move now.