African companies are under growing pressure to treat sustainability as a management system, not a reporting appendix.

By September 2025, 17 jurisdictions had adopted ISSB standards, and 19 more were planning to adopt, raising the bar for comparable ESG disclosure across global markets.

This puzzle offers a practical framework for connecting leadership, data, risk, operations and disclosure before trust, competitiveness and capital are lost.

Fund assets using responsible or sustainable investment approaches reached $16.7 trillion in 2024, an increase of approximately 49% from $5.5 trillion in two years.

Why ESG Requires Full Business Integration

The “Sustainability Integration Puzzle” appears simple at first glance: a set of blocks representing functions most companies already recognise, from leadership and governance to disclosure and continuous improvement.

However, the image captures a harder truth for African corporations. ESG performance often fails not because ambition is absent, but because the parts sit in separate departments, are owned by different teams, measured through different systems, and reported too late to shape real business decisions.

That matters more now because sustainability expectations are moving from voluntary signalling into market infrastructure. As ISSB adoption widens, the issue for African and other emerging-market companies is no longer whether ESG belongs in strategy.

The real test is whether climate risk, workforce capability, supplier performance, governance oversight and disclosure quality are tightly connected enough to influence capital allocation, resilience and market credibility.

Capital Now Rewards Integrated ESG Systems

Capital is increasingly rewarding systems that can prove sustainability performance with discipline rather than slogans. Global sustainable investment-linked assets reached $16.7 trillion in 2024, while clean energy accounted for 64% of total energy investment that year.

That shift is not abstract for African corporations. As standards converge, companies seeking bank finance, development finance, export access, insurance confidence, and institutional capital will increasingly be asked not only what their ESG policy says but also how the business governs climate risk, measures outcomes and discloses material information.

This is where the puzzle becomes useful. Leadership sets direction. Governance defines roles. Strategy integration aligns sustainability with commercial priorities. Risk management identifies threats to value.

Data and metrics convert intent into evidence. Operations, innovation, supply chain, culture, stakeholder engagement, disclosure and continuous improvement are what turn policy into everyday business behaviour.

Every Puzzle Piece Must Connect

Each element of the infographic addresses a distinct management question; however, none can stand on its own.

Leadership defines accountability. Governance clarifies oversight.

- Strategy identifies what drives growth.

- Risk tests what could erode value.

- Data establishes what can be measured.

- Operations and supply chains reveal where impacts occur.

- Disclosure determines what can be defended publicly.

- Continuous improvement shows whether the business is learning quickly enough.

That interdependence mirrors the direction of global reporting rules. IFRS S1 focuses on sustainability-related risks and opportunities, while IFRS S2 narrows in on climate disclosures, including emissions, physical and transition risks, and scenario analysis.

For African businesses, the message is clear: ESG credibility is built operationally first. If procurement, credit, oversight, finance, legal, risk and sustainability teams are misaligned, the sustainability narrative will not hold.

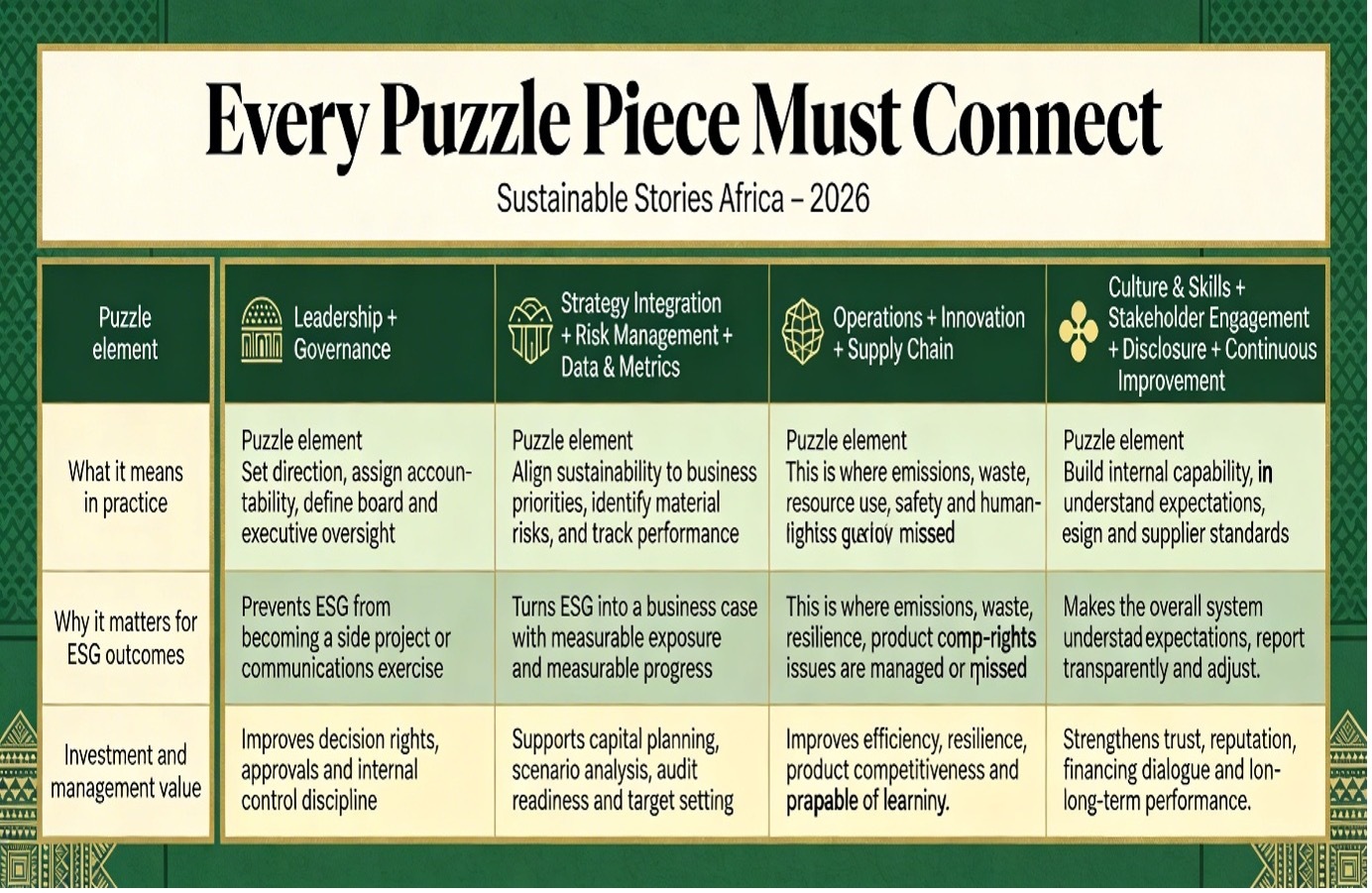

Puzzle element | What it means in practice | Why it matters for ESG outcomes | Investment and management value |

|---|---|---|---|

Leadership + Governance | Set direction, assign accountability, define board and executive oversight | Prevents ESG from becoming a side project or communications exercise | Improves decision rights, approvals and internal control discipline |

Strategy Integration + Risk Management + Data & Metrics | Align sustainability to business priorities, identify material risks, and track performance | Turns ESG into a business case with measurable exposure and measurable progress | Supports capital planning, scenario analysis, audit readiness and target setting |

Operations + Innovation + Supply Chain | Embed sustainability in processes, product design and supplier standards | This is where emissions, waste, resource use, safety and human-rights issues are managed or missed | Improves efficiency, resilience, product competitiveness and procurement quality |

Culture & Skills + Stakeholder Engagement + Disclosure + Continuous Improvement | Build internal capability, understand expectations, report transparently and adjust | Makes the overall system credible, responsive and capable of learning | Strengthens trust, reputation, financing dialogue and long-term performance |

Integration Turns ESG Into Value

When the puzzle comes together, sustainability stops operating as a compliance cost and functions as a quarterly value-creation system. That is why integration matters more than symbolism.

Better governance, cleaner data, stronger supplier visibility and more credible disclosure can strengthen investor confidence, improve lender engagement, sharpen regulatory readiness and reinforce strategic positioning.

For African corporations, the opportunity is especially important as sectors are being repriced in real time.

Power shortages, water stress, logistics gaps and carbon-heavy production create pressure; however, they also reward smarter investment, stronger risk management systems, better supplier capabilities and more focused, decision-useful ESG disclosure.

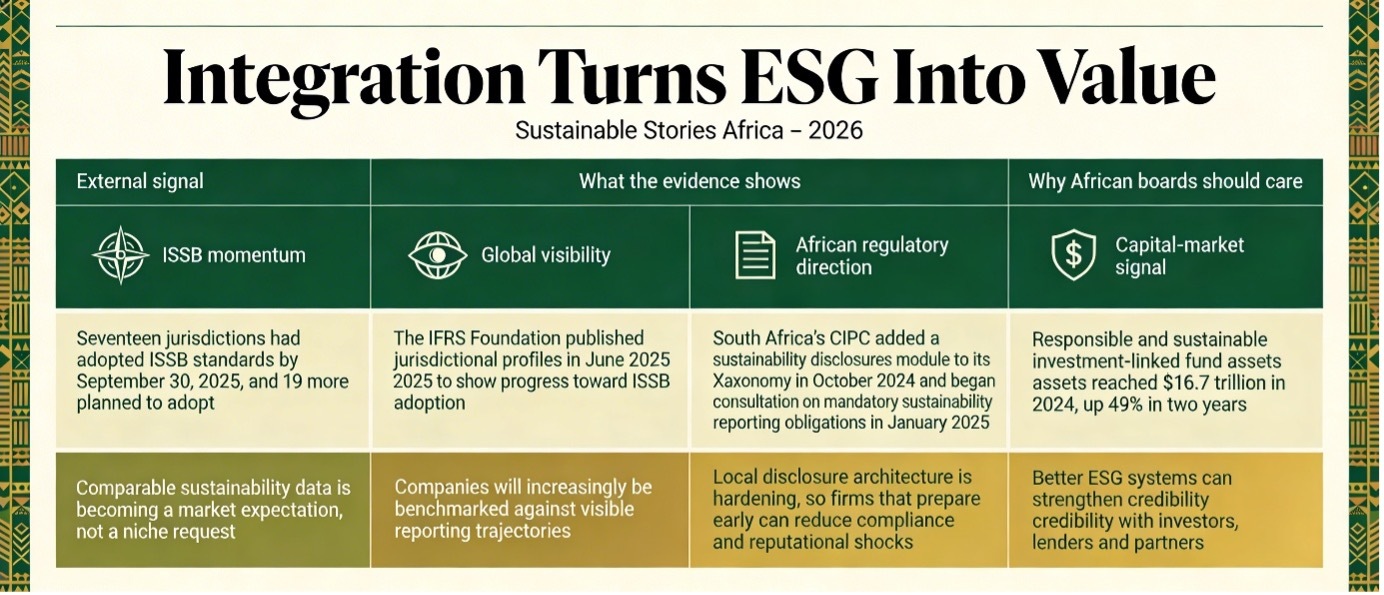

External signal | What the evidence shows | Why African boards should care |

|---|---|---|

ISSB momentum | Seventeen jurisdictions had adopted ISSB standards by September 30, 2025, and 19 more planned to adopt | Comparable sustainability data is becoming a market expectation, not a niche request |

Global visibility | The IFRS Foundation published jurisdictional profiles in June 2025 to show progress toward ISSB adoption | Companies will increasingly be benchmarked against visible reporting trajectories |

African regulatory direction | South Africa’s CIPC added a sustainability disclosures module to its XBRL taxonomy in October 2024 and began consultation on mandatory sustainability reporting obligations in January 2025 | Local disclosure architecture is hardening, so firms that prepare early can reduce compliance and reputational shocks |

Capital-market signal | Responsible and sustainable investment-linked fund assets reached $16.7 trillion in 2024, up 49% in two years | Better ESG systems can strengthen credibility with investors, lenders and partners |

Build One Coherent Management Loop

African corporations do not need to chase every sustainability framework at once.

The smarter approach is to build an integration sequence that links accountability, materiality, measurement and disclosure within a single management loop.

That need is becoming more urgent as regulators and standard setters shift from broad ambition to more structured disclosure rules.

Five practical steps stand out.

- Boards should assign clear responsibility for climate, workforce, supply-chain and disclosure issues.

- Companies should create a single materiality map tied to revenue, costs, assets, liabilities and community impact.

- They need decision-grade data systems, earlier supplier integration through standards and training, and disclosure treated as the output of management quality, not a substitute for it.

- Governments, regulators, financiers and employees also matter.

- Clearer rules, aligned timelines, and stronger incentives can help shift ESG from communications rhetoric to a tool for resilience, efficiency, inclusion and long-term competitiveness.

Path Forward – Connect Systems, Protect Enterprise Value

African corporations do not need a bigger ESG vocabulary. They need tighter links between leadership, governance, strategy, risk, data, operations, suppliers and disclosure.

The companies that move early will be better placed to meet rising ISSB-aligned expectations, defend enterprise value and turn sustainability spending into measurable investment rather than symbolic compliance.