African companies are increasingly being asked to decarbonise operations, strengthen climate resilience and reduce pressure on nature, often from the same balance sheet.

However, green finance, climate finance and biodiversity finance are not the same.

For companies seeking capital, the distinction now affects eligibility, disclosure expectations, pricing, investor fit and project design.

Finance Labels Now Shape Capital Access

Across African boardrooms, the ESG conversation has moved beyond reputation and into capital allocation.

Projects are no longer assessed simply on whether they appear sustainable, but on the specific environmental problem they address, how outcomes will be measured, and which financing pool they can credibly access.

That distinction matters. Green finance is the broadest category. Climate finance targets low-carbon and climate-resilient outcomes. Biodiversity finance is aimed at protecting, restoring and sustainably managing nature.

When companies blur those categories, they risk presenting the wrong transaction to the wrong investors, or missing lower-cost, better-aligned capital altogether.

The urgency is rising. Climate finance to Africa increased by 48%, from $29.5 billion in 2019/20 to $43.7 billion in 2021/22; however, that still meets only 23% of the continent’s estimated climate-finance needs through 2030.

At the same time, the global biodiversity finance gap remains approximately $700 billion a year. This underlines how undercapitalised nature-positive investment still is, even as ecosystem risk becomes more material to business performance.

Capital Is Available, But Highly Selective

Africa’s annual climate investment passed the $50 billion mark for the first time in 2022, but the structure of that capital remains uneven. International sources still accounted for 87% of tracked climate finance, while private finance contributed just 18%.

The implication is straightforward: capital is available, but it is increasingly selective and tied to clear definitions, taxonomies and measurable impact.

For African corporations, this makes terminology a strategic issue.

Under the IFC’s Green Bond Framework, green finance has a broad umbrella, while climate finance and biodiversity finance are among the more specific categories with different investor expectations.

An energy-efficiency upgrade may qualify as green and climate finance, but it only counts as biodiversity finance when it directly protects or restores nature. For finance teams, this is no longer semantics; it is capital matching.

Different Labels Open Different Capital Pools

The most practical way to distinguish these financing categories is to look at the problem each is meant to solve.

- Green finance covers broad environmental outcomes, from renewable energy and energy efficiency to green buildings, cleaner industry, biodiversity protection, and water stewardship.

- Climate finance is more targeted, focusing on decarbonisation and resilience.

- Biodiversity finance is narrower still, centred on protecting, restoring and sustainably managing ecosystems.

That distinction is becoming more material as capital pools grow at different speeds.

Governments have now adopted a global biodiversity finance strategy aimed at mobilising $200 billion annually by 2030, while private finance for nature has expanded sharply.

For African corporations, the message is clear: Access to capital is increasingly shaped by the language of finance.

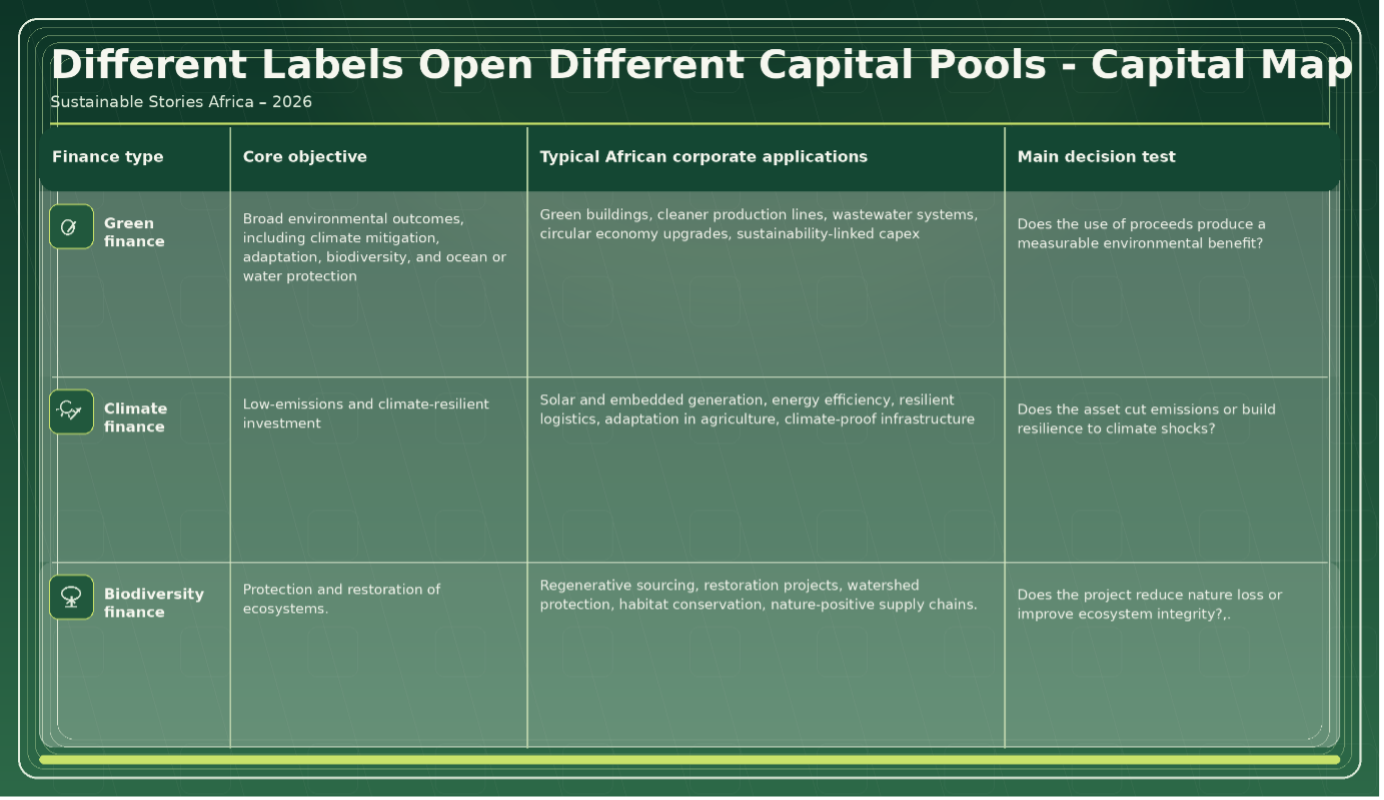

Capital map

Finance type | Core objective | Typical African corporate applications | Main decision test |

|---|---|---|---|

Green finance | Broad environmental outcomes, including climate mitigation, adaptation, biodiversity, and ocean or water protection | Green buildings, cleaner production lines, wastewater systems, circular economy upgrades, sustainability-linked capex | Does the use of proceeds produce a measurable environmental benefit? |

Climate finance | Low-emissions and climate-resilient investment | Solar and embedded generation, energy efficiency, resilient logistics, adaptation in agriculture, climate-proof infrastructure | Does the asset cut emissions or build resilience to climate shocks? |

Biodiversity finance | Protection and restoration of ecosystems | Regenerative sourcing, restoration projects, watershed protection, habitat conservation, nature-positive supply chains | Does the project reduce nature loss or improve ecosystem integrity? |

For African companies, overlap across financing categories is common, but the funding story still requires precision.

An agribusiness restoring land, improving water stewardship and cutting diesel use may combine green, climate and biodiversity elements; however, each component may fit a different capital window.

That distinction matters because climate finance in Africa remains highly concentrated. With a small group of countries absorbing most flows, companies that classify projects clearly and report outcomes credibly stand a better chance of attracting capital than those that package every environmental effort as a broad ESG claim.

Precision Brings Resilience, Credibility and Capital

Getting the label right delivers more than compliance.It expands access to capital, lowers the risk of failed fundraising, and helps companies build assets that are better prepared for regulation, climate shocks, supply-chain disruption and changing buyer expectations.

Markets increasingly reward clear use-of-proceeds structures, credible reporting and measurable environmental outcomes, rather than broad sustainability claims.

Biodiversity finance also presents a strategic opening that many African corporates still undervalue.

Nature loss is becoming an operational, regulatory and supply-chain risk for sectors ranging from banking and insurance to food, mining and real estate.

Companies that move early can strengthen competitiveness, protect productive assets and position themselves for the next wave of blended and sustainability-linked finance.

Boards Must Match Projects to Capital

African corporations need to treat environmental finance as a portfolio discipline, not a branding exercise.

Boards and finance teams should classify projects clearly before approaching investors, distinguishing between broad environmental improvement, climate mitigation or adaptation, and measurable nature protection or restoration.

They also need stronger evidence. Each project should be backed by baselines and target metrics that can be measured, monitored and reported.

Financing instruments should then be matched to project type, whether through green bonds, climate-finance windows, biodiversity finance or blended capital. Just as importantly, governance must improve.

Stronger controls over the use of proceeds, internal assurance and board oversight are becoming essential as investor scrutiny grows more rigorous.

Path Forward – One Strategy, Three Financing Languages Ahead

African corporations do not need three separate sustainability stories. They need one disciplined capital strategy that classifies projects correctly, measures outcomes rigorously and speaks the language each pool of finance requires.

The companies most likely to attract investment will be those that climate-proof assets, nature-proof supply chains, and turn ESG ambition into investable, reportable pipelines before markets price the transition more aggressively.