Africa holds the renewable resources to anchor a global green hydrogen economy. However, only three projects, totalling just 23.5 MW, are operational across the entire continent.

A landmark 2025 report by GIZ and the Africa Green Hydrogen Alliance documents the full scope of this gap.

The potential is real. The pipeline is vast. But the distance between ambition and delivery is widening. What must change, and who must act, is now in plain sight.

Potential Vast, Delivery Still Distant

Africa stands at a defining energy crossroads. The African Green Hydrogen Report 2025, published by Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) in partnership with the Africa Green Hydrogen Alliance, presents one of the continent's most comprehensive assessments of green hydrogen readiness to date.

The findings signal both exceptional promises and sobering structural constraints that demand immediate action from governments, financiers, and regional institutions.

Released against the backdrop of South Africa's G20 Presidency and the African Union's formal endorsement of its African Green Hydrogen Strategy at the 38th AU Summit in February 2025, the report calls for coordinated action across policy, finance, infrastructure, and capacity-building.

These are not distant goals; they are the preconditions for a competitive and inclusive continental GH₂ economy.

With global pressure to decarbonise hard-to-abate sectors accelerating, the question for Africa is no longer whether it has the resources.

It demonstrably does. The question is whether its institutions, regulatory systems, and financial structures can mobilise fast enough to convert potential into production.

A 23.5 MW Reality vs. a 40,000 MW Pipeline

Just three projects, totalling a mere 23.5 MW of installed electrolyser capacity, are operational across Africa's entire green hydrogen sector.

Contrast that with over 40,000 MW at the feasibility stage and 61 further initiatives at the concept phase, and the gap between Africa's ambition and its current delivery becomes stark.

Global electrolyser capacity surged from 200 MW in 2019 to an estimated 5,200 MW by the end of 2024. Africa's contribution: 15 MW in Egypt, 5 MW in Namibia, and 3.5 MW in South Africa.

Five additional projects combining over 75 MW are under construction. Only 8 of more than 110 announced projects across Africa have moved beyond Final Investment Decision (FID), compared to a global FID rate of just 4%.

Africa's renewable energy endowment is not in question. The speed, structure, and substance of its transition from announcement to action is.

The Numbers That Define the Opportunity

The economic stakes embedded in Africa's green hydrogen future are transformative. Domestic hydrogen demand in South Africa, Egypt, and Morocco already exceeds 2 million tons annually, projected to rise to between 3 and 4 million tons across the continent by 2030, and between 6 and 10 million tons by 2050.

Five nations, including Tunisia, Namibia, Morocco, Egypt, and South Africa, are targeting GH₂ exports of more than 20 million tons annually by 2050, primarily to European and Asian markets.

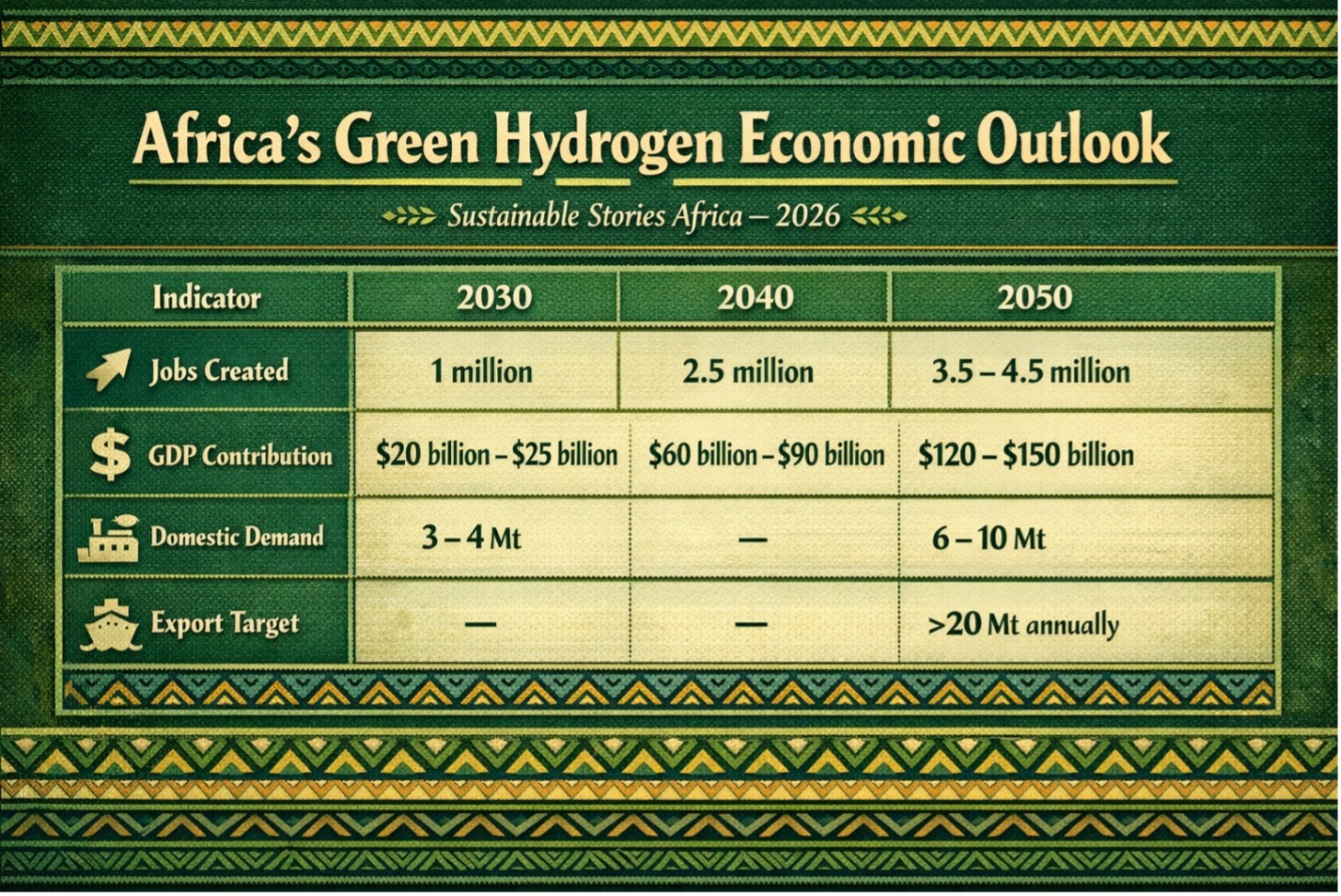

Africa's Green Hydrogen Economic Outlook

| Indicator | 2030 | 2040 | 2050 |

|---|---|---|---|

| Jobs Created | 1 million | 2.5 million | 3.5 – 4.5 million |

| GDP Contribution | $20 billion – $25 billion | $60 billion – 90 billion | $120 – $150 billion |

| Domestic Demand | 3 – 4 Mt | — | 6 – 10 Mt |

| Export Target | — | — | >20 Mt annually |

Priority domestic sectors include fertiliser production, green steel and cement, heavy transport, mining, maritime fuel, and grid balancing, industries central to African industrialisation and food security.

Africa's reserves of platinum group metals, copper, and nickel in South Africa, Mozambique, Zambia, the DRC, and Zimbabwe further position the continent as a critical node in the global GH₂ supply chain.

The financing picture, however, reveals acute bottlenecks. Almost 80% of public funding for African GH₂ projects has come from Europe, with Germany accounting for 13%.

Over 90% of those committed funds remain undisbursed as of 2024. Africa holds just 20 registered hydrogen patents, and Namibia alone faces a projected skills gap of 130,000 workers by 2040.

What a Functioning Green Hydrogen Economy Looks Like

The pieces are beginning to fall into place. Namibia's HyIron Oshivela project, the world's first green iron produced from green hydrogen, delivered its first output in March 2025. The project benefited from a €13.7 million German federal grant covering 40% of Phase 1 costs, and support from the SDG Namibia One Fund.

It is proof that coordinated policy commitment and blended finance can move African projects to commercial scale.

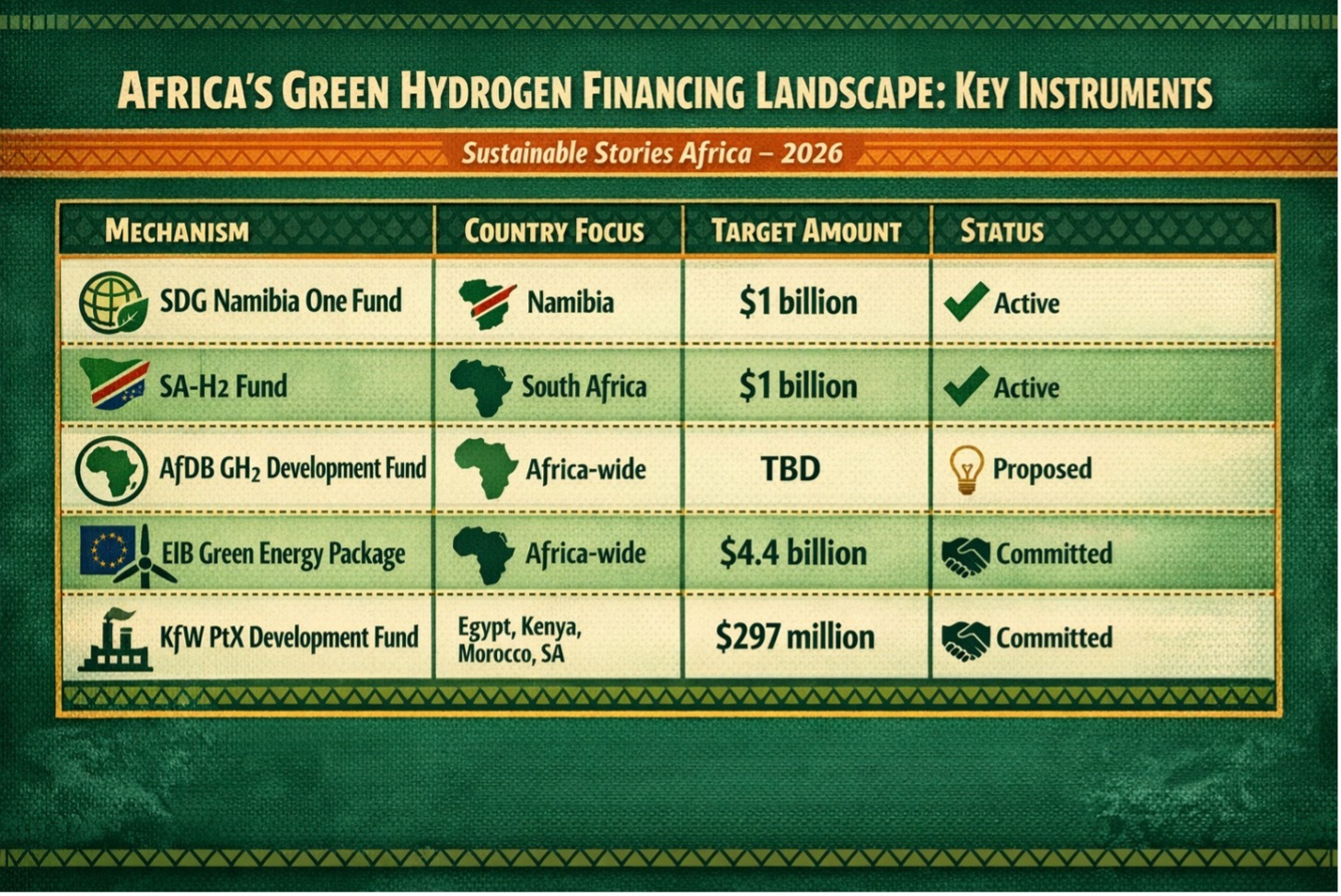

Africa's Green Hydrogen Financing Landscape: Key Instruments

| Mechanism | Country Focus | Target Amount | Status |

|---|---|---|---|

| SDG Namibia One Fund | Namibia | $1 billion | Active |

| SA-H2 Fund | South Africa | $1 billion | Active |

| AfDB GH₂ Development Fund | Africa-wide | TBD | Proposed |

| EIB Green Energy Package | Africa-wide | $4.4 billion | Committed |

| KfW PtX Development Fund | Egypt, Kenya, Morocco, SA | $297 million | Committed |

Eight countries, including Algeria, Egypt, Kenya, Mauritania, Morocco, Namibia, South Africa, and Tunisia, now have hydrogen strategies or roadmaps in place, following the AU's endorsement of its continental Green Hydrogen Strategy in February 2025.

ECOWAS has set binding production targets of 0.5 Mt by 2030 and 10 Mt by 2050 under its regional GH₂ Policy and Strategy Framework.

Political will is crystallising. The window for coordinated first-mover action is open.

Governments, Investors, and Institutions Must Move Now

The report's ten strategic recommendations present a clear, actionable blueprint.

- Establishing regional GH₂ corridors, connecting RE-rich zones to industrial hubs and export ports, is the foundational step, beginning with joint feasibility studies across Regional Economic Communities (RECs).

- A continental infrastructure master plan must follow, preventing duplication and aligning investments with long-term demand.

- Regulatory harmonisation across regional blocs is non-negotiable. The current patchwork of individually negotiated project agreements creates investor uncertainty, raising the cost of capital, a dynamic already shown to push Africa's Levelised Cost of Green Hydrogen above Southern Europe's despite better renewable resources.

- South Africa's Gas Act Amendment Bill, Kenya's certification gaps, and Tunisia's regulatory lag are each urgent national priorities.

- Financiers must close the disbursement gap. Over 90% of committed public funding remains on paper.

- Unlocking requires policy de-risking alongside financial de-risking, credible regulatory environments, transparent procurement, and binding offtake agreements.

- The African Development Bank-anchored GH₂ Development Fund, offering blended loans, grants, and equity, should be fast-tracked as a continent-wide capital mobilisation vehicle.

Path Forward – From Strategy to Delivery

Africa’s green hydrogen opportunity hinges on execution. Turning its solar, wind, mineral and geographic advantages into bankable value chains will require regulation, coordinated infrastructure and blended finance that moves from promise to disbursement. These must advance together.

Regional alignment, skills development and enforceable ESG safeguards will determine whether GH₂ growth is inclusive. Africa has the base; it now needs delivery.