Zimbabwe is finally enjoying lower inflation, steadier exchange rates and stronger growth. However, this stability is being bought with crowded‑out social spending, stubborn poverty and a regulatory maze that keeps most firms informal.

Balancing stability, debt and deep poverty

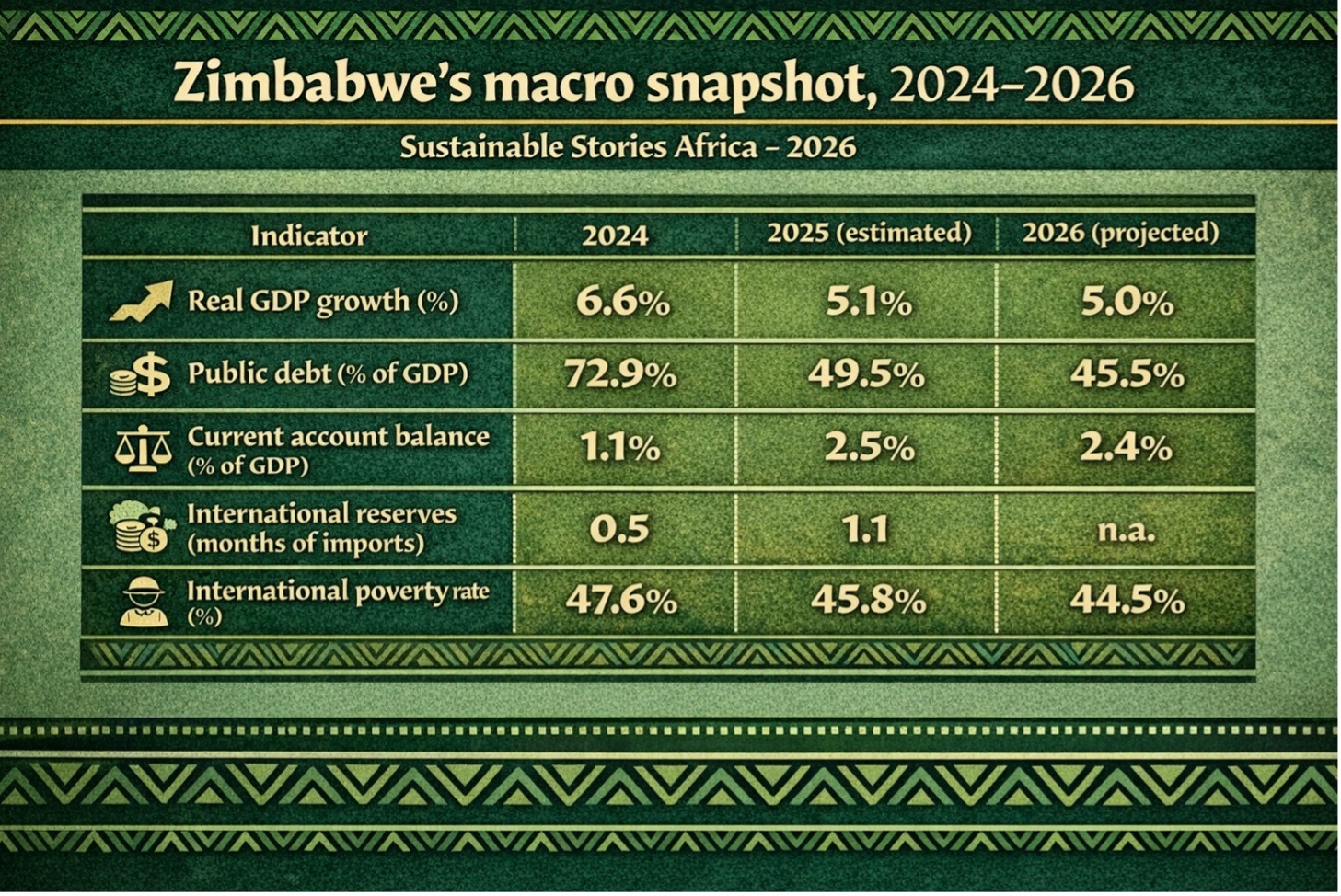

Zimbabwe entered 2025 with a paradoxical economic story: macro indicators are improving, yet households remain trapped close to the edge. This is according to the World Bank Zimbabwe Economic Update Report 2025. Real GDP growth was projected at 5.1% in 2025, supported by rebounds in agriculture, mining and services. This is amidst falling public debt, which has fallen sharply as a share of GDP from 72.9% in 2024 to 49.5% in 2025 after rebasing and exchange‑rate stabilisation.

Inflation

Inflation, once the defining symbol of Zimbabwe's crisis, moderated, with monthly ZiG and USD inflation staying in single digits through 2025, and year‑on‑year weighted inflation was expected to settle around 13% by December, backed by tight monetary policy and a stable ZiG‑USD exchange rate.

However, these gains sat alongside an extreme poverty rate still around 42% in 2023 and an international poverty rate only edging down from 47.6% in 2024 and projected to drop to 45.8% in 2025, underscoring how fragile welfare was expected to remain after years of shocks and drought.

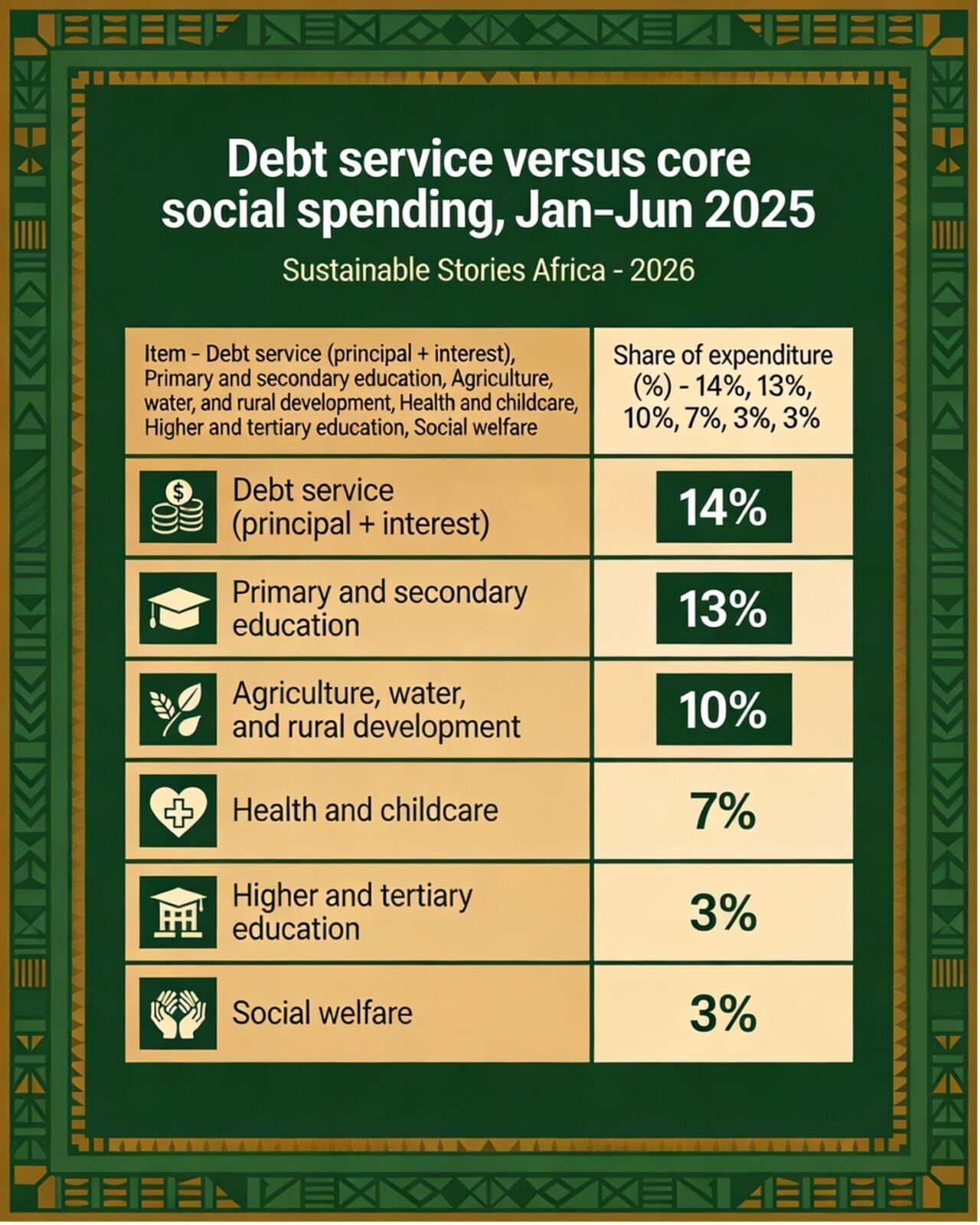

Behind the macro headlines, the state was paying heavily for past decisions. Debt service in the first half of 2025 reached $524 million, with 14% spent on expenditure, which was more than primary and secondary education, agriculture or health care, even as legacy debts, external arrears and domestic arrears keep Zimbabwe in public‑debt distress, which locked it out of affordable international finance.

Growth returns, but buffers are thin

Growth rebounds, but cushions remain perilously thin.

For the first time in several years, the macroeconomic narrative is no longer dominated by runaway inflation or exchange-rate collapse.

Real GDP growth has averaged above 5% in recent years and is projected at 5% in 2026, supported by a rebound in agriculture, following the El Niño-induced drought, expanding gold and lithium output, and new iron and steel capacity coming on stream.

The external position has also improved. The current account has shifted into a modest surplus, from 1.1% of GDP in 2024 to a projected 2.5% in 2025, driven by higher mineral exports, easing fuel and food imports, and rising remittances, which grew from $1.2 billion in 2020 to $2.7 billion in 2025. However, reserves remain critically low, and stand at 1.1 months of import cover, making the economy vulnerable and exposed to external and climate shocks.

Zimbabwe's macro snapshot, 2024–2026

| Indicator | 2024 | 2025 (estimated) | 2026 (projected) |

|---|---|---|---|

| Real GDP growth (%) | 6.6% | 5.1% | 5.0% |

| Public debt (% of GDP) | 72.9% | 49.5% | 45.5% |

| Current account balance (% of GDP) | 1.1% | 2.5% | 2.4% |

| International reserves (months of imports) | 0.5 | 1.1 | n.a. |

| International poverty rate (%) | 47.6% | 45.8% | 44.5% |

ZiG stability, dollarisation and the debt squeeze

ZiG steadies markets, debt squeezes classrooms.

The April 2024 launch of the ZiG, followed by decisive monetary tightening after a brief surge in reserves, has helped stabilise the official exchange rate and cooled monthly inflation. A one-off devaluation pushed the year-on-year ZiG inflation above 90% in August 2025, but a sharp deceleration is expected.

The central bank has the Monetary Policy Rate (MPR) at 35%, curtailed money-supply growth, ended quasi-fiscal operations, and aligned the official rate more closely with market demand through the Willing-Buyer – Willing-Seller framework.

However, dollarisation remains deeply entrenched. Foreign-currency accounts remain high, making up 82.5% of broad money, as little has changed since the introduction of ZiG. Households and firms continue to hedge against future currency transitions. A headline 20% parallel-market premium narrowed to roughly 7 – 9% once bank margins and transaction taxes are included, suggesting reduced misalignment but persistently low trust in domestic money.

Fiscal dynamics are similarly double-edged. Revenues have strengthened, increasing marginally by about 6.3% from 14.3% of GDP in 2024 to 15.2% in 2025, thus delivering a modest deficit of 0.3% of GDP.

However, constrained access to concessional finance has increased the reliance on treasury bills and arrears, while debt service now absorbs 14% of spending, crowding out investment in people and resilience.

Debt service versus core social spending, Jan–Jun 2025

| Item | Share of expenditure (%) |

|---|---|

| Debt service (principal + interest) | 14% |

| Primary and secondary education | 13% |

| Agriculture, water, and rural development | 10% |

| Health and childcare | 7% |

| Higher and tertiary education | 3% |

| Social welfare | 3% |

Total public debt has climbed by a 127.9% from $10.4 billion in 2019 to about $23.7 billion by mid‑2025, including over $8.4 billion in external arrears and more than $1 billion in domestic arrears, even as the debt‑to‑GDP ratio fell on the back of rebasing and growth.

Legacy obligations – blocked funds ($3.73 billion), compensation to former farm owners ($3.5 billion) and $2.16 billion in absorbed RBZ liabilities continue to weigh on the balance sheet and on politics.

Turning reforms into inclusive resilience

From fragile stability to shared, shock‑proof growth.

Economic recovery has yet to translate into broad-based welfare gains. Extreme food poverty peaked at 49% in 2020 and remained at about 42% in 2023, while structural transformation has stalled: rural populations and agricultural employment shares rose through the 2010s rather than declining.

A predominantly rain-fed smallholder sector leaves livelihoods highly exposed to drought, and a fragmented, low-coverage, weakly targeted social protection system struggles to absorb shocks.

At the same time, the private sector is being asked to lead growth while navigating a dense regulatory thicket. Roughly 76% of firms remain informal, facing high compliance costs across dozens of permits, fees, and licences imposed by some 25 regulators and nine ministries.

This para-fiscal model effectively taxes formalisation and investment, with licensing cited as a binding constraint by formal firms and a deterrent by informal entrepreneurs.

This is where reform moves beyond technocratic checklists. The 2025 Presidential Ease of Doing Business initiative and a new regulatory transparency drive signal a shift toward regulation as a competitiveness tool. In parallel, the national social registry (ZISO) offers a pathway to cushion households during fiscal consolidation, if scaled and properly funded.

Debt deals, discipline and cutting red tape

Hard reforms now, to anchor tomorrow's gains

The economic update is explicit about the next steps. On the macro front, Zimbabwe is anchoring its path on the Structured Dialogue Platform for arrears clearance and debt resolution, while seeking an IMF Staff-Monitored Program from early 2026.

The six-point Economic Reform Matrix provides a roadmap, maintaining tight monetary policy and a transparent FX regime, clearing RBZ liabilities, strengthening revenue and expenditure management, and protecting the most vulnerable.

Politically, the path is narrow. A credible SMP would likely entail spending restraint and new domestic revenue measures at a time when debt service already competes with classrooms and clinics, and arrears to domestic suppliers persist.

The report argues for pro-poor fiscal consolidation, rationalising tax expenditures, increasing health-damaging excises, improving mining revenues, trimming redundant public employment, and digitising procurement, to protect stability while creating space for social protection and priority infrastructure.

At the micro level, the business-regulation chapter offers an unusually concrete playbook. In the near term, it calls for a comprehensive regulatory review across 12 priority sectors, elimination of redundant licences, pilot joint inspections, and reduced reliance on para-fiscal charges.

Over time, it envisages a public registry of regulations, a unified digital licensing portal, risk-based fees, regulator consolidation, and legally anchored Regulatory Impact Assessments overseen from the centre of government.

These are not marginal tweaks. They will determine whether recovery remains confined to a narrow formal enclave or expands to draw in the 76% of firms still operating in the informal economy.

Path Forward – Locked‑in reforms, locally grounded resilience

Locking reforms, widening ownership, protecting the vulnerable

The report concludes on a sober warning. Even with growth above 5% and stabilising prices, downside risks remain acute, from renewed inflation and exchange-rate pressures to climate-driven droughts and social tensions around adjustment. A successful SMP and arrears-clearance process could unlock concessional finance and restore multilateral engagement; however, costs will fall hardest on low-income households already living near the poverty line.

The path forward rests on three commitments: sustaining hard-won macro discipline, accelerating business-environment reforms to generate quality jobs, and scaling integrated social protection through ZISO and poverty data.