Green Central Banking has explained how Scope 1, 2 and 3 emissions help organisations measure climate impact and financial risk.

The framework matters now as regulators, investors and lenders demand clearer climate disclosures.

For African businesses, the question is no longer whether emissions count, but who measures them, who pays, and who is left exposed.

Carbon Counting Moves Into Mainstream Finance

Carbon emissions reporting is moving from sustainability departments into boardrooms, bank risk teams and investment committees, as Green Central Banking’s April 2026 explainer argues that Scope 1, 2 and 3 emissions provide a practical framework for measuring climate-related risk.

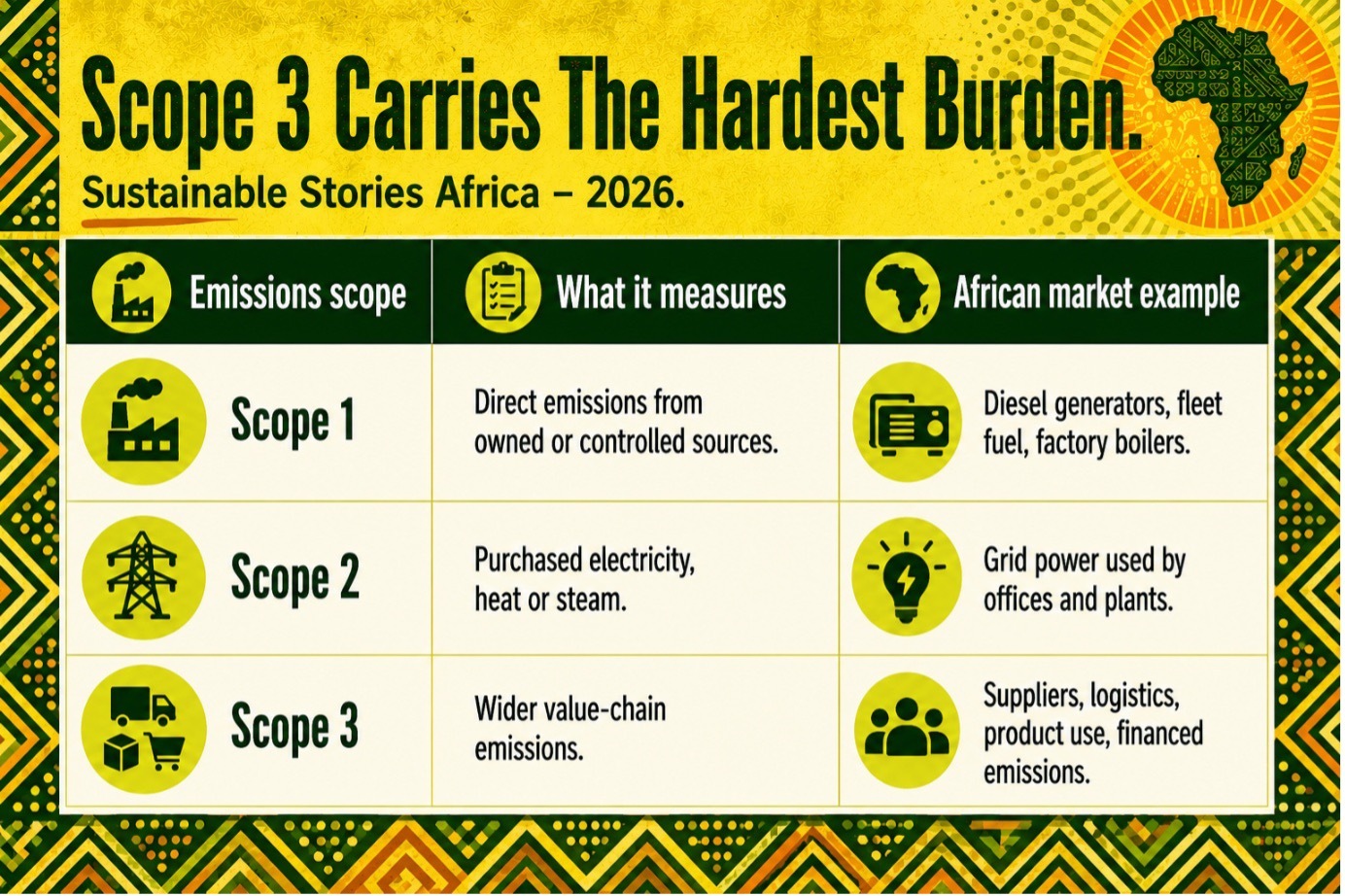

The framework divides emissions into three categories: Scope 1 covers direct emissions from sources owned or controlled by an organisation; Scope 2 covers indirect emissions from purchased electricity, heat or steam; and Scope 3 covers wider value-chain emissions, including suppliers, transport, product use and financed activities.

The Network for Greening the Financial System uses the same baseline definitions in its climate disclosure guidance for central banks.

For African businesses, this changes the commercial conversation.

- A factory in Aba

- A bank in Nairobi

- Acocoa exporter in Accra

- A logistics company in Durban

May now be judged not only by profit, but by the carbon trail behind its power, suppliers, transport and financing.

Scope 3 Carries The Hardest Burden

The first two scopes are easier to understand. Scope 1 is what a company burns or releases directly: diesel generators, company vehicles, boilers or industrial processes. Scope 2 is the electricity it buys, which matters deeply in markets where grids are still fossil-heavy or unreliable.

Scope 3 is the difficult one. It looks beyond the company gate.

- For a bank, it can include emissions linked to loans and investments.

- For a retailer, it can include suppliers, packaging, transport and how customers use products.

- For an exporter, it can reach into farms, warehouses, shipping and final markets.

That is why Scope 3 has become the real test of climate credibility. UNEP Finance Initiative guidance says banks’ climate targets should include clients’ Scope 1, 2 and 3 emissions where significant and where data allows, with coverage expected to rise as data quality improves.

Better Data Can Unlock Finance

The prize is not just compliance. Better carbon accounting can help African companies access cheaper capital, protect export markets and strengthen credibility with global buyers.

As climate disclosure rules tighten, companies that understand their emissions profile can identify where savings are possible. A manufacturer may cut fuel costs by improving energy efficiency.

A bank may reduce portfolio risk by helping clients transition. An agribusiness may defend market access by tracing emissions across farms and transport routes.

The danger is that companies without data may be treated as higher-risk counterparties, even when their actual emissions are modest.

This matters for small and medium-sized enterprises that supply larger companies but lack carbon-accounting tools.

Without support, Scope 3 reporting could become another barrier between African producers and global value chains.

Disclosure Needs Capacity, Not Just Rules

The next step is practical implementation. Regulators, banks, development finance institutions and business groups should help firms build emissions data systems before disclosure becomes punitive.

That means templates, sector benchmarks, affordable measurement tools, supplier training and clearer rules on financed emissions.

It also means recognising African realities: many firms operate with unstable electricity, fragmented logistics and limited access to climate finance.

Carbon accounting should not become a paperwork exercise. It should guide investment into cleaner power, efficient transport, better buildings, climate-smart agriculture and more resilient supply chains.

Path Forward – Turn Carbon Data Into Climate Investment

The path forward is to make emissions measurement useful, comparable and fair. African markets need carbon data that supports finance, not exclusion.

Governments, banks and companies should align reporting rules with capacity-building, especially for SMEs.

Well done, Scope 1, 2 and 3 accounting can move Africa from climate-risk exposure toward credible transition planning, stronger ESG performance and better access to sustainable capital.

Culled From: Measuring carbon emissions – scope 1, 2 and 3 explained - Green Central Banking