A 500-question ESG interview bank for 2026 reads like a hiring tool. It is also a market signal.

The document shows how sustainability work has moved far beyond glossy reporting into regulation, assurance, data controls, Scope 3, board governance, biodiversity, finance and litigation risk.

For African public companies, the real issue is capability: who within the firm can credibly answer these questions?

Why the talent question matters

African public companies are entering a phase of ESG maturity in which the biggest risk may no longer be whether they publish a sustainability report, but whether they have the internal capability to produce one that can survive investor scrutiny, lender due diligence, customer questionnaires, assurance review and board oversight.

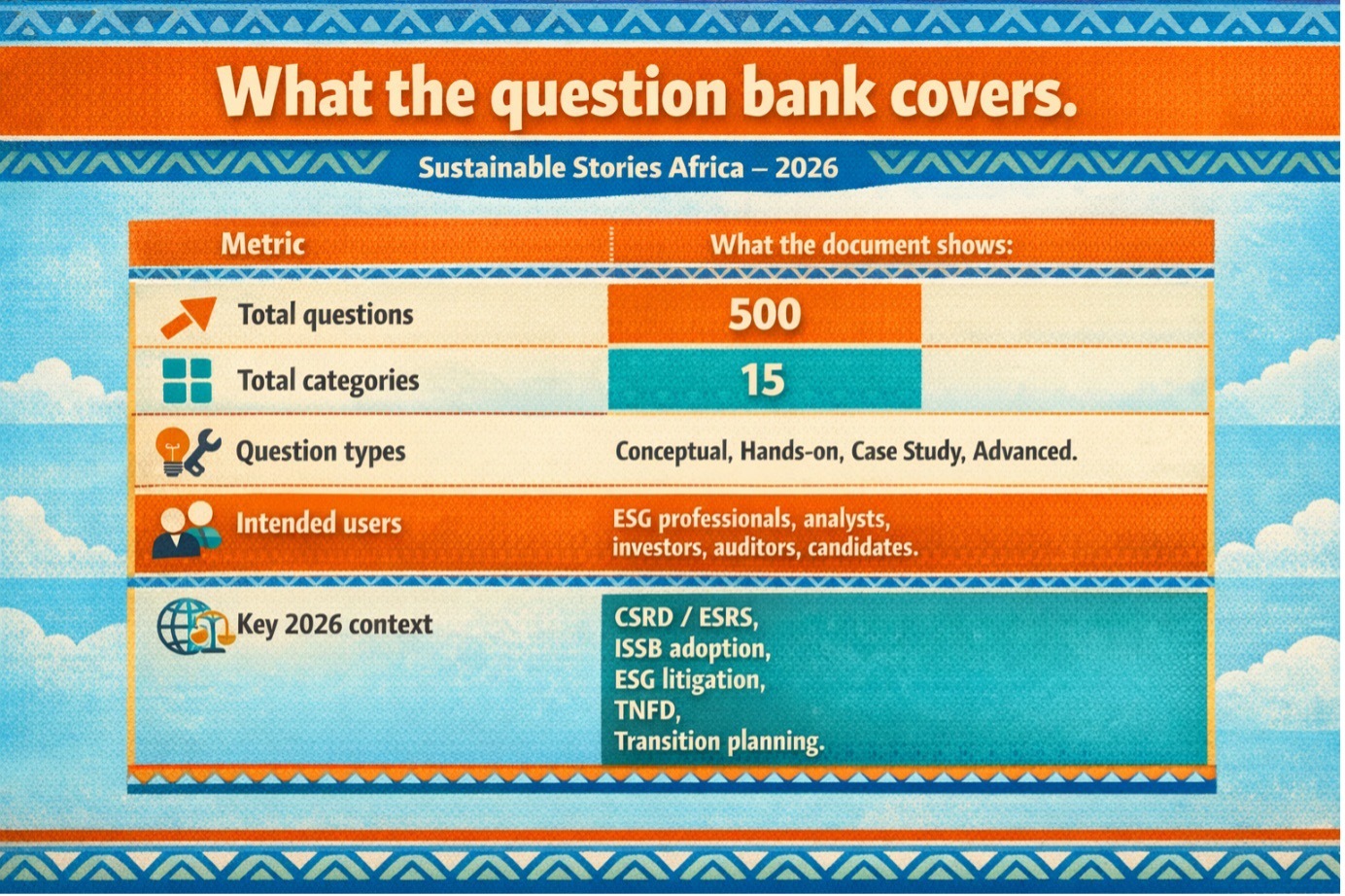

A new ESG & Sustainability Interview Question Bank 2026 makes that shift unusually visible. It compiles 500 likely interview questions across 15 categories, ranging from ESG fundamentals to reporting frameworks, regulations, data systems, assurance, GHG accounting, social metrics, biodiversity, governance, sustainable finance, supply chain due diligence, materiality and transition planning.

That breadth matters because it captures what the market now expects an ESG function to know.

The document is designed for ESG professionals, analysts, investors, auditors and candidates for roles in sustainability reporting, ESG advisory, climate finance and corporate governance.

Its premise is straightforward: in 2026, credible ESG work is cross-functional, technical and increasingly regulated.

From an African public company perspective, this is not merely a recruitment issue. It is a governance issue, a disclosure issue and a competitiveness issue.

Questions now define the market

The most striking feature of the question bank is not the number 500. It is the pattern those questions reveal. They are tagged across four types:

- Conceptual

- Hands-on

- Case Study

- Advanced

This means the market is no longer looking only for theoretical ESG fluency. It wants people who can build reporting systems, defend materiality judgments, respond to crises, prepare assurance-ready data, map regulations across jurisdictions and explain trade-offs to boards and CFOs.

The 15 sections cover the full architecture of modern ESG work. They include

- ESG Fundamentals & Strategy

- ESG Reporting Frameworks

- ESG Regulations & Policy

- ESG Reporting Process & Data Management

- ESG Assurance & Audit

- GHG Accounting & Climate Reporting

- Social & Human Capital, Environmental Reporting (Beyond GHG)

- ESG Governance & Ethics

- ESG in Finance & Sustainable Investing

- Supply Chain ESG & Scope 3 Due Diligence

- Materiality Assessment, Net Zero

- Transition Plans & Target Setting

- ESG Ratings, Rankings & Indices

- Emerging Topics & Advanced Case Studies.

That list reads less like a niche sustainability curriculum and more like a map of how listed company oversight is being rebuilt.

The new ESG job is operational

The document explicitly says the 2026 landscape is defined by mandatory CSRD/ESRS reporting in Europe, emerging ISSB adoption globally, growing ESG litigation risk, mainstreaming of TNFD, and the integration of transition planning into regulatory requirements.

It advises candidates to cite specific frameworks and regulatory texts, use structured answers for case studies, and stay current with EFRAG, ISSB and IOSCO updates.

That matters for African public companies because many are still staffing ESG as if it were mostly communications, stakeholder relations or annual-report production. The question bank suggests the opposite.

Modern ESG roles increasingly demand comfort with inline XBRL, limited assurance, ISAE 3000, Scope 3 methodologies, EU Taxonomy, CSDDD-style supply-chain due diligence, board committee design, proxy advisor expectations, ESG ratings engagement, and AI-related governance.

In other words, the centre of gravity is shifting from storytelling to systems.

That shift aligns with broader governance trends already visible in Europe. A previous paper in this conversation argued that ESG oversight is moving into the corporate control framework itself, making boards and management responsible for controls, data accuracy and accountability in the same way financial reporting already does.

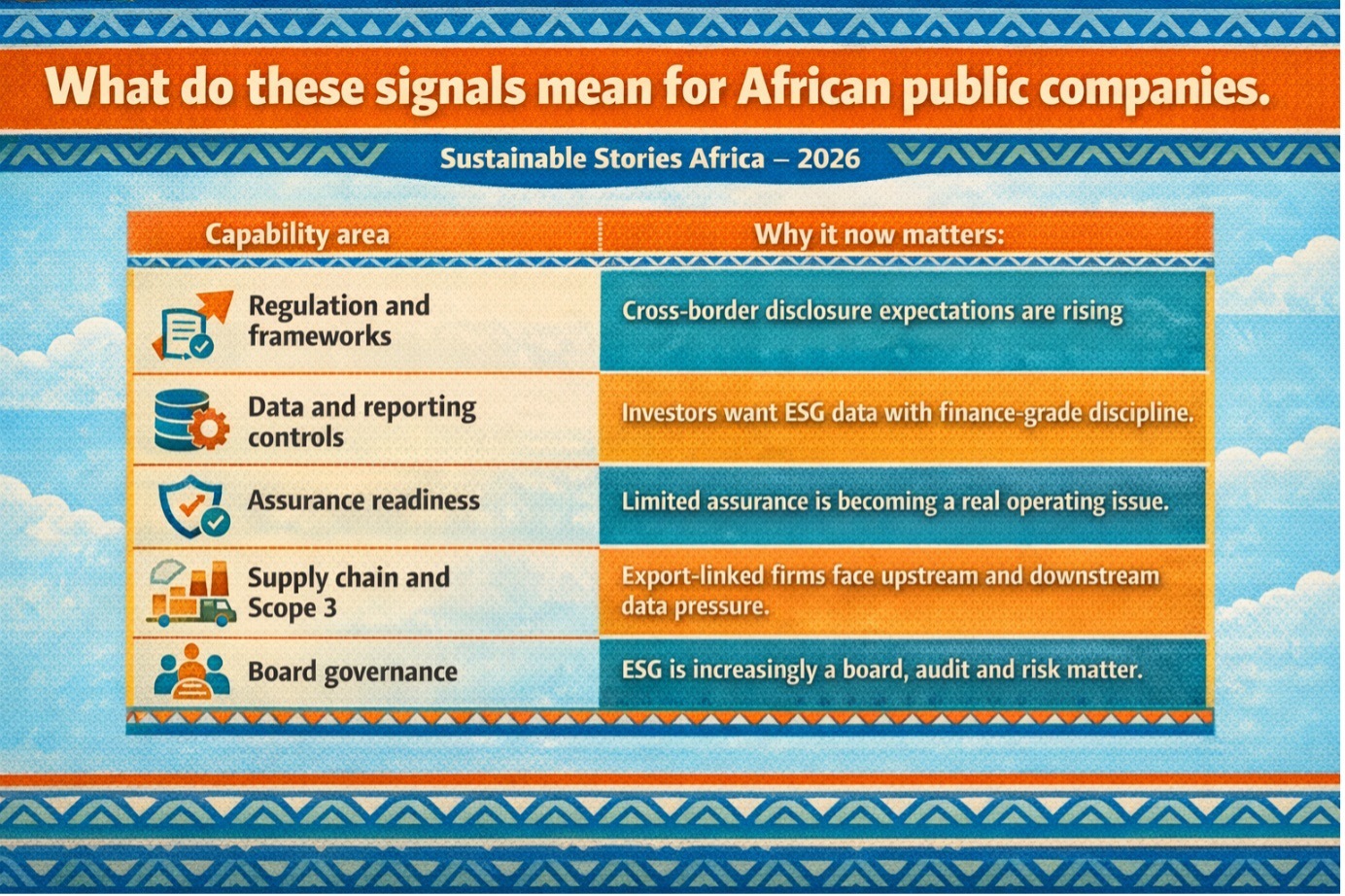

Why African issuers should pay attention

For African public companies, three implications stand out.

- First, ESG capability now affects access to capital. The question bank includes sections on sustainable finance, green bonds, sustainability-linked instruments, climate stress testing, financed emissions and ESG factor investing, showing that markets increasingly treat ESG knowledge as part of core capital-market competence.

- Second, value-chain pressure is hardening. The document devotes 30 questions to Supply Chain ESG & Scope 3 Due Diligence and another block to data collection, supplier questionnaires, third-party data risk, and ESG response processes for investors, customers and banks. That is particularly relevant for African exporters and suppliers integrated into European and global chains.

- Third, boards need better internal challenge. Questions on board oversight, ESG-linked remuneration, anti-bribery, tax transparency, whistleblower mechanisms, lobbying, proxy advisors and governance committees show that ESG governance is no longer separable from company governance.

A better ESG team creates value

There is a constructive side to this. A stronger ESG talent bench can help African issuers move beyond reactive compliance into strategic advantage.

The question bank repeatedly links ESG to the CFO, cost of capital, credit ratings, integrated reporting, M&A due diligence, transition planning and resilience.

It also pushes candidates to explain the ROI of ESG investments, set dashboards, build content libraries, run internal audit programs for ESG data and benchmark maturity against peers.

For companies operating in energy, banking, telecoms, consumer goods, mining, industrials or agriculture, that matters because good ESG capability can reduce duplication, improve lender dialogue, strengthen board decision-making and cut the risk of inconsistent claims across reports, questionnaires and investor engagements.

It can also help firms manage the shift from carbon-only thinking toward water, biodiversity, labour rights, digital ethics, and nature-related risks.

The point is not that every African-listed company must build a huge sustainability department. It is that the people it hires and the questions it asks them now determine how credible the company’s ESG story will be later.

What boards and management should do

The document is designed as a preparation tool for interviews, but management teams could use it as a diagnostic tool.

If a public company’s ESG lead, finance team, internal audit, procurement head and board committee chairs cannot answer a large share of these questions, that is not just a talent gap. It is a readiness gap.

From an African public company perspective, the next steps are practical.

Boards should review whether ESG oversight sits clearly with the full board, audit committee or a dedicated committee. Management should assess whether the ESG function has real technical depth on reporting frameworks, controls, data governance and assurance.

HR teams should revise job descriptions away from generic sustainability language toward framework-specific, systems-oriented competence. And CFOs should bring ESG closer to finance, because the questions increasingly assume that financial and sustainability reporting are converging operationally, even where they remain separate formally.

This is especially urgent given how quickly European reporting expectations have evolved. Even though the EU has recently narrowed mandatory CSRD scope, the broader market expectation for usable sustainability data remains high, especially from value chains, financing relationships and investor pressure.

Path forward – ESG Interviews Signal Africa’s Corporate Future

African public companies should treat the 2026 ESG interview market as an early warning system.

The skills now being tested, regulation, assurance, data controls, Scope 3, board oversight and nature-related risk, are the capabilities markets increasingly expect companies to have, whether or not law demands them immediately.

The smartest move now is to hire and train for substance: people who can build systems, defend disclosures, challenge weak claims and connect ESG to finance and governance.

In the next phase of public-company ESG, the quality of questions may matter as much as the quality of answers.